January 9, 2026

at

1:00 am

EST

MIN READ

TRON Stablecoin Ecosystem Report

.png)

Executive Summary

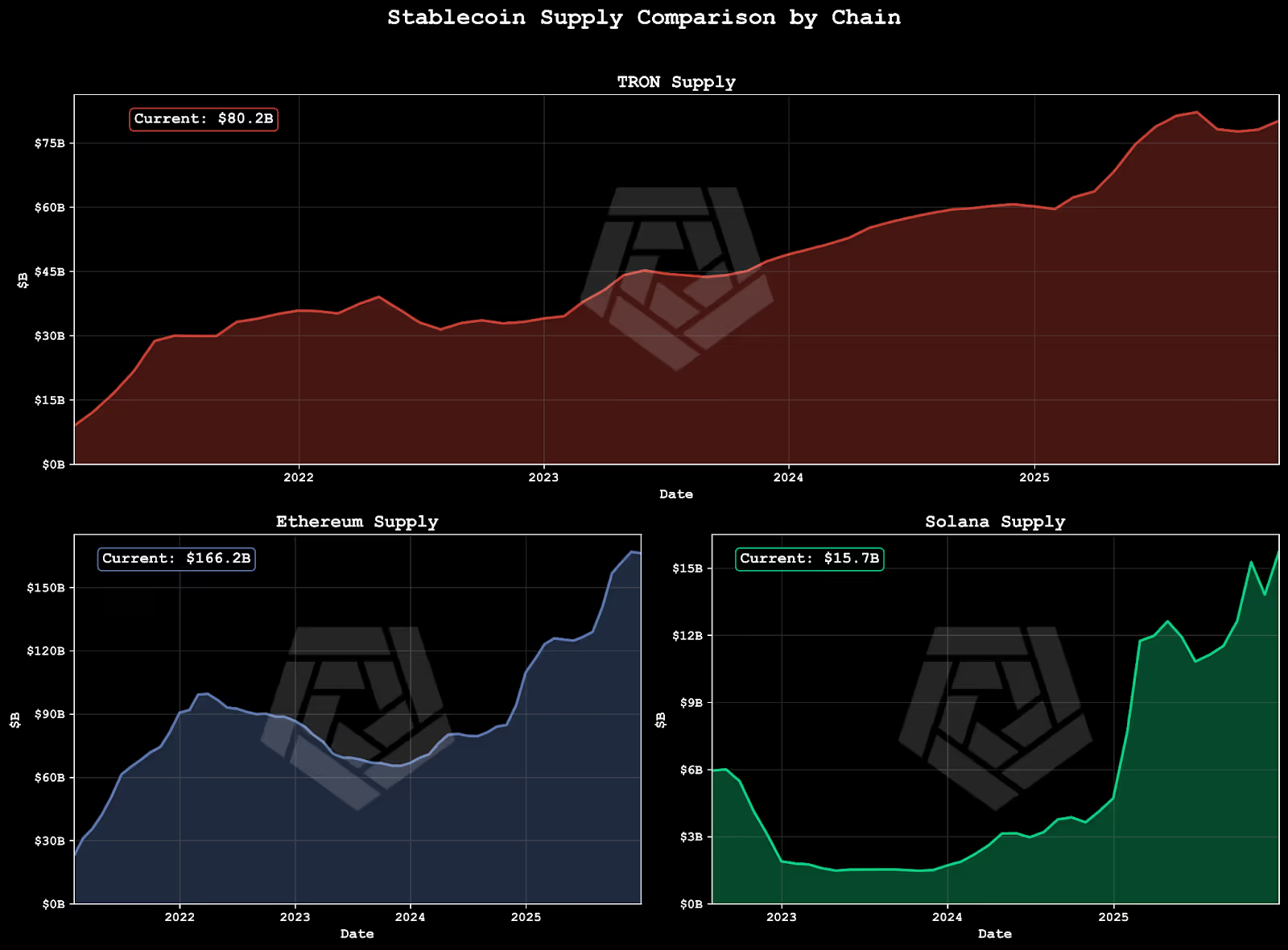

TRON has established itself as one of the largest blockchains by stablecoin supply, hosting over $80 billion in assets and processing more than $20 billion in daily volume across 2 million transactions. This positions the network as the second-largest stablecoin chain, trailing only Ethereum. The network's growth has been driven by a straightforward value proposition: near-zero fees, fast confirmations, and an EVM-compatible environment that lowers integration barriers.

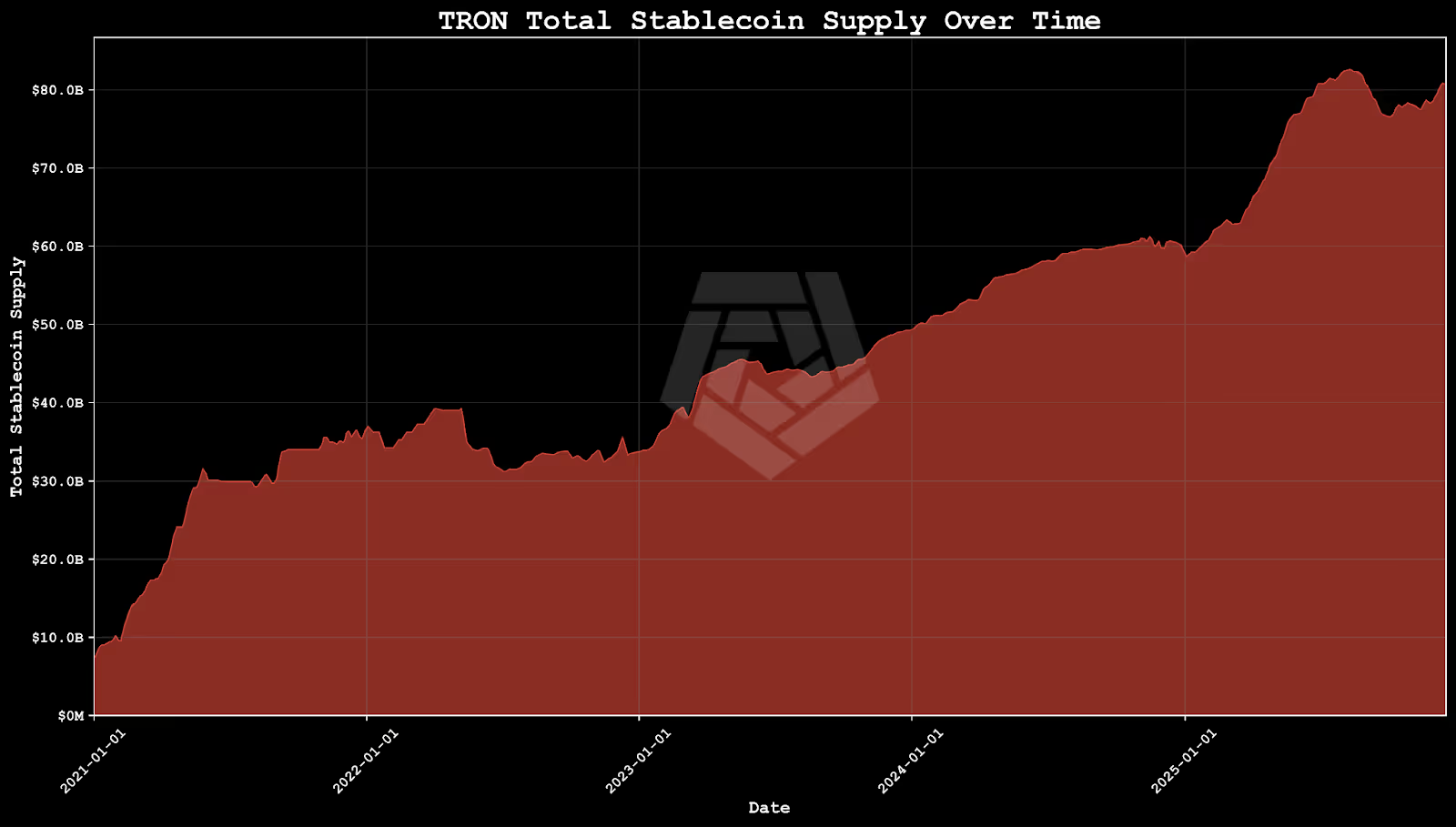

Stablecoin supply has grown nearly tenfold since 2021, through both bull and bear market conditions. During the 2022-2023 bear market, TRON's supply remained resilient and continued expanding while Ethereum's contracted. The largest USD stablecoin on TRON is Tether's USDT, which accounts for the vast majority of circulating supply and makes TRON the most active settlement layer for Tether's flagship token.

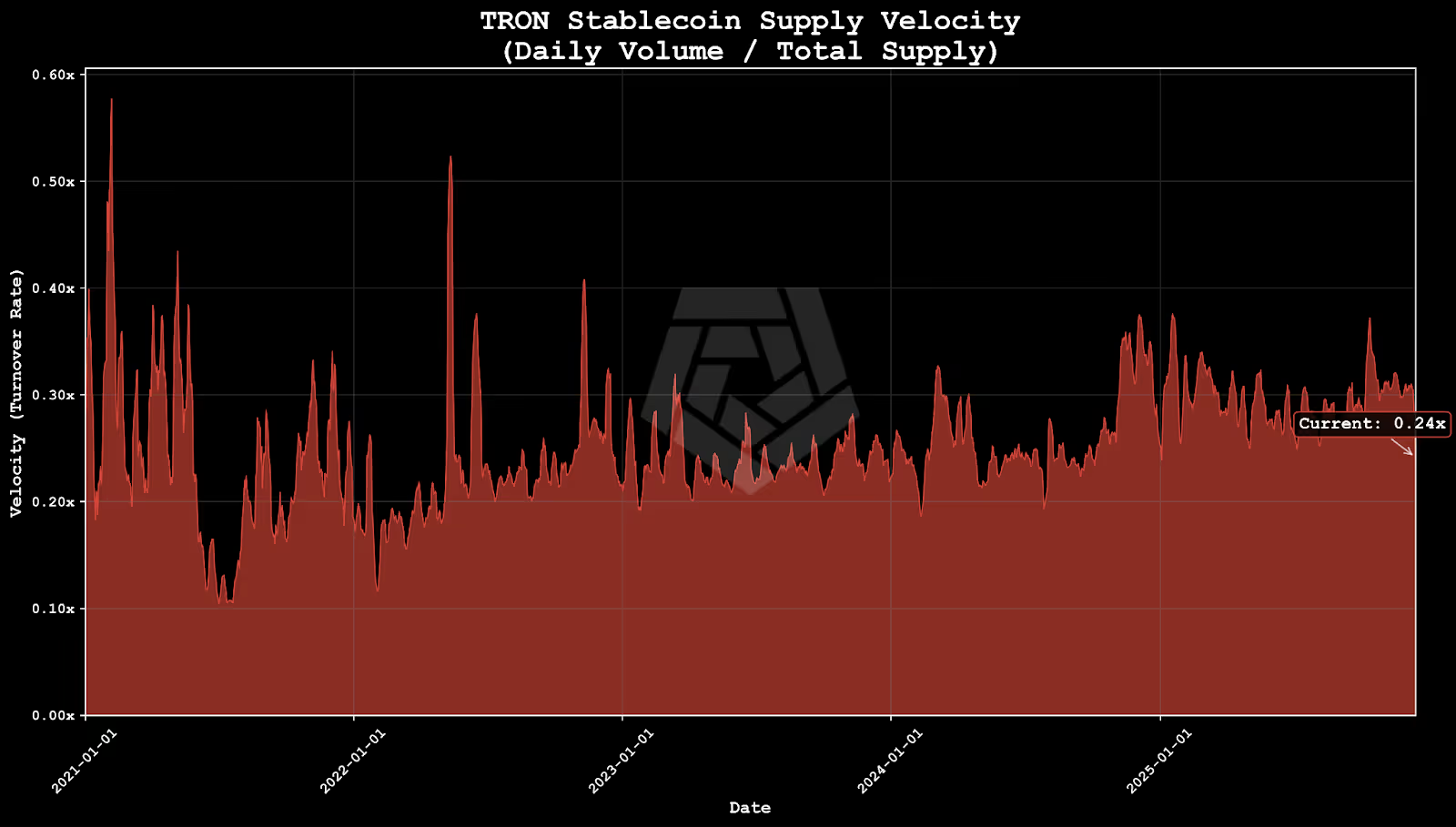

On-chain data suggests TRON’s stablecoin usage emphasizes settlement and transfer activity, while its broader DeFi ecosystem continues to evolve. Centralized exchanges account for a majority of labeled stablecoin inflows. This exchange-centric pattern, combined with daily supply velocity of 0.2-0.3x, indicates users treat TRON-based stablecoins as a utility for moving value between platforms and jurisdictions. The velocity remains consistent regardless of market conditions, suggesting TRON's core use case is insulated from speculative cycles.

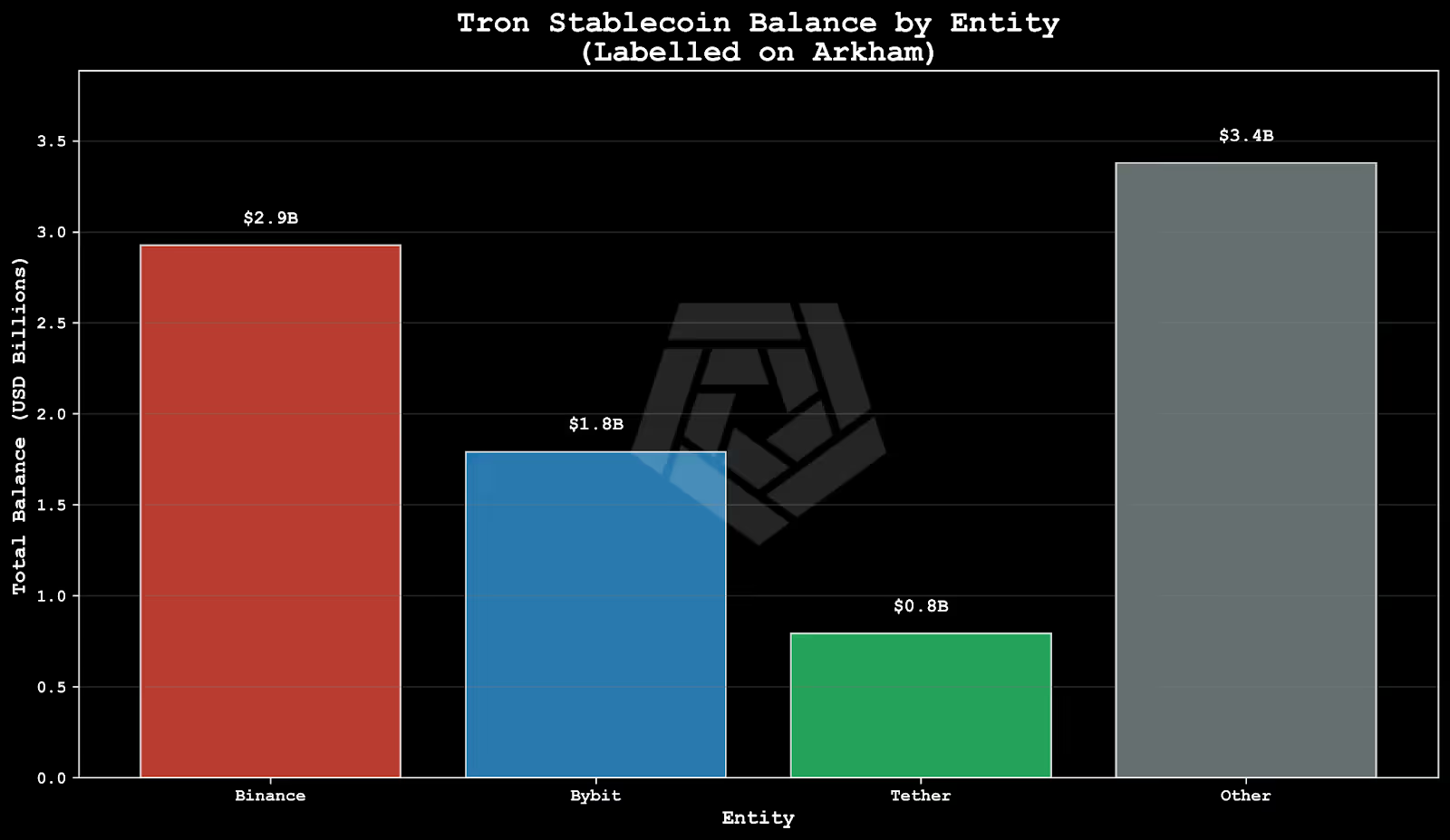

Stablecoin distribution skews toward mid-sized holders, suggesting a more retail-oriented user base compared to Ethereum's institutional concentration. Among labeled entities, Binance holds the largest balance at $2.9 billion, followed by Bybit at $1.8 billion.

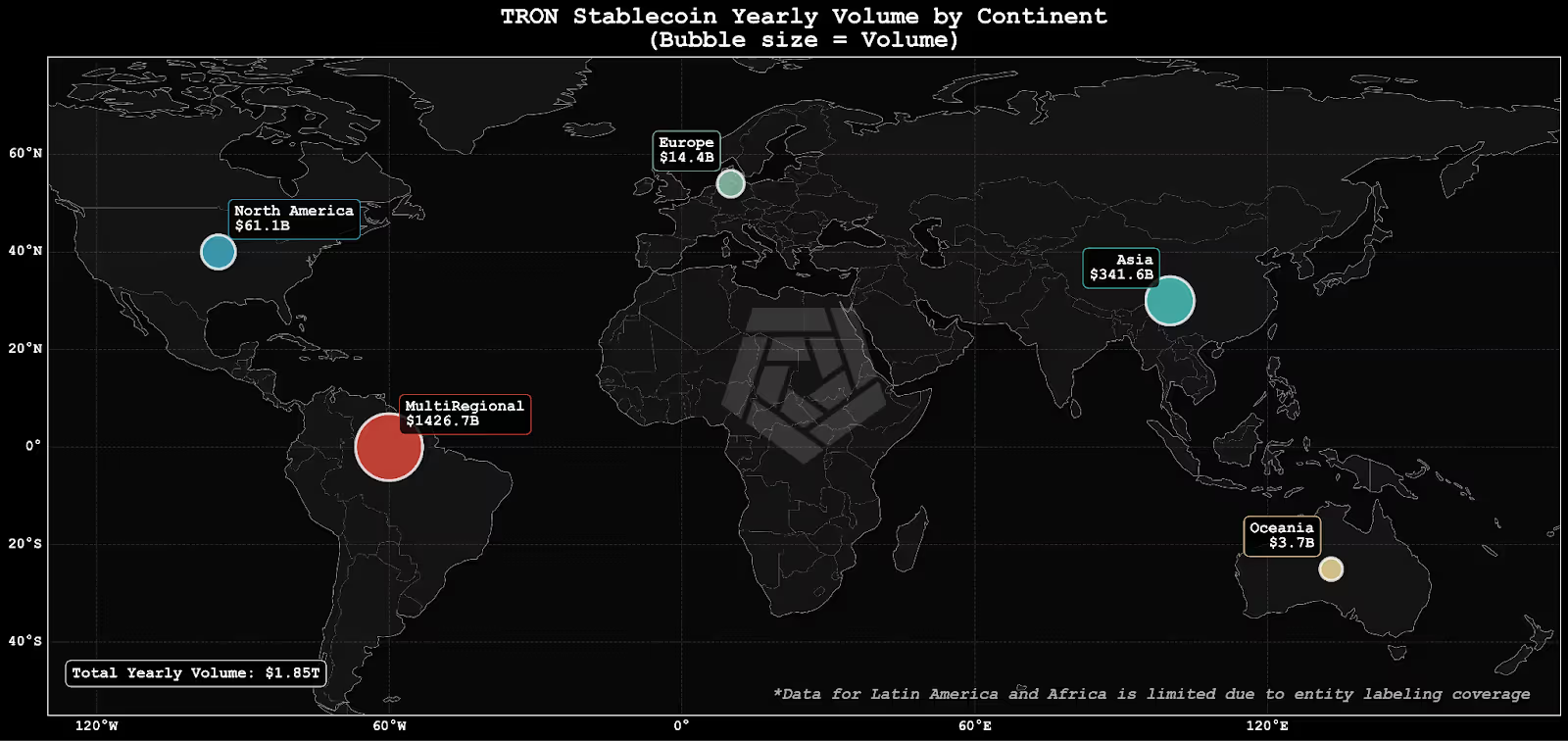

Geographically, activity is weighted toward Asia, accounting for nearly $341 billion annually. Emerging markets including Turkey, Indonesia, and India contribute significant volume, reflecting TRON's appeal where transaction costs drive demand for efficient infrastructure.

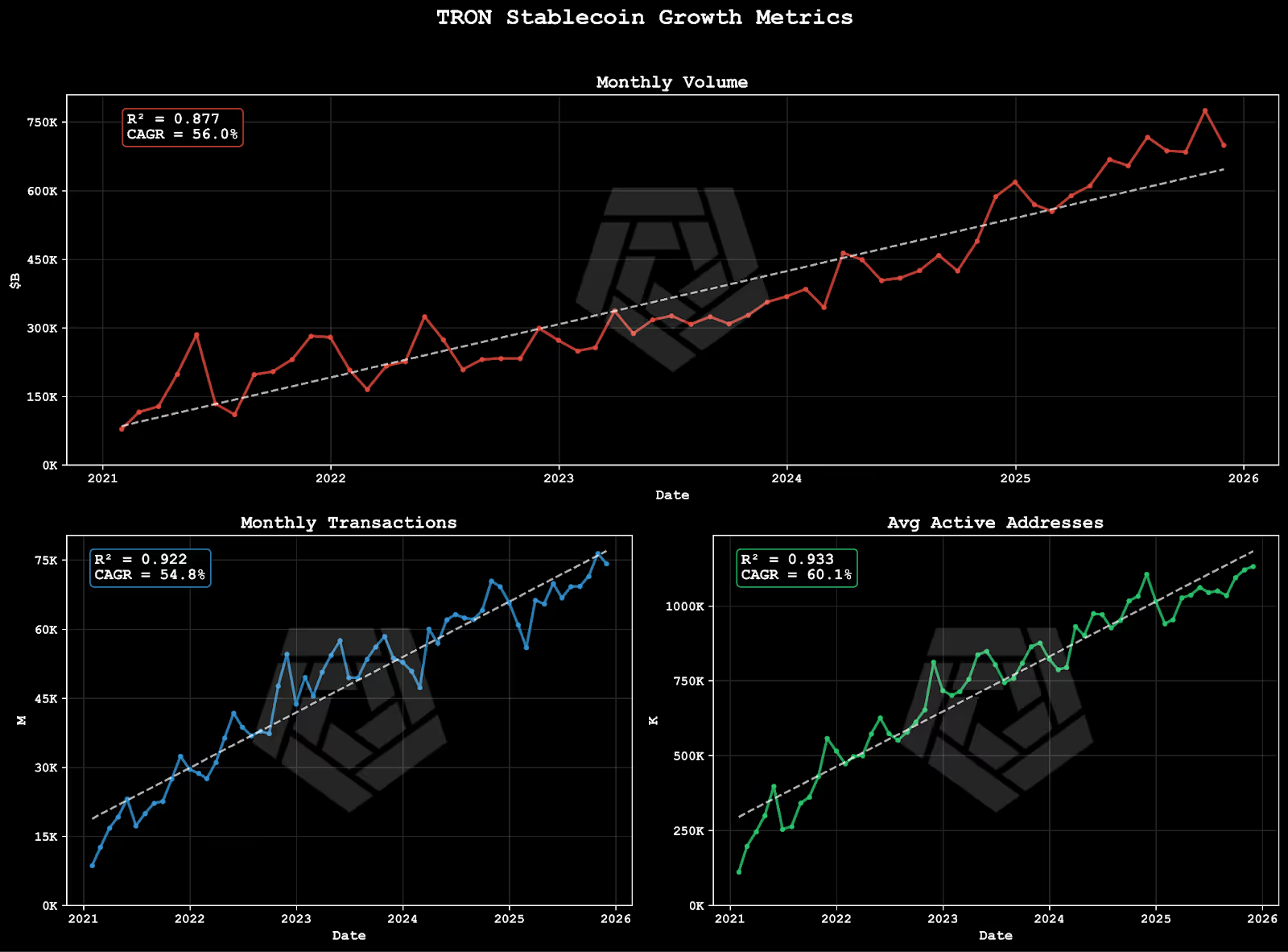

Growth metrics remain strong, with compound annual growth rates between 54% and 60% since 2021. Year-over-year growth shows daily volume increasing 45.9%, transactions rising 11.2%, and active addresses growing 9.8%. The network now averages over 1 million active addresses daily, indicating expansive adoption.

TRON Stablecoin Ecosystem Overview

Market Composition and Supply Metrics

TRON has quietly become a critical piece of infrastructure in the global stablecoin ecosystem. With over $80 billion in stablecoin supply, the network ranks as the second-largest blockchain by this metric. Its appeal is straightforward: near-zero transaction fees, fast confirmation times, and EVM-compatible tooling make it the preferred rail for high-volume, cost-sensitive transfers, particularly in emerging markets and for remittance use cases where every basis point matters. While Ethereum remains the dominant chain for DeFi and institutional custody, TRON has carved out a distinct niche as the workhorse network for everyday stablecoin movement.

The largest USD stablecoin on TRON by far is Tether's USDT, with over $80 billion in circulating supply on the network. Daily activity reinforces this dominance: the network routinely processes over $20 billion in USDT volume across more than 2 million transactions, making TRON Tether's most active settlement layer.

Position Relative to Competing Chains

TRON occupies a distinct middle ground in the multi-chain stablecoin landscape. While Ethereum remains the largest chain by total stablecoin supply and Solana has emerged as a high-throughput competitor, TRON has carved out its niche as a cost-efficient familiar infrastructure for mid-to-large value transfers. This segmentation becomes clear when examining supply distribution, fee structures, and transaction patterns across chains.

Ethereum has historically dominated stablecoin supply, but since mid-2020 TRON has steadily closed the gap. Through the 2022-2023 bear market, TRON's stablecoin supply remained resilient and even continued growing while Ethereum's contracted, narrowing the spread between the two chains. By late 2024, TRON briefly approached parity with Ethereum before both resumed growth into 2025. In the next bear market, it would be reasonable to expect TRON to regain market share as Ethereum undergoes another speculative contraction. Solana, meanwhile, has emerged as a fast-growing third player, though its stablecoin supply remains a fraction of either incumbent.

Network Characteristics

TRON's network metrics explain its stablecoin dominance. With median transfer fees of just $0.09 compared to Ethereum's $3.73, and confirmation times of 3 seconds versus 12, TRON offers a practical middle ground: fast and cheap enough for everyday transfers, yet established enough to handle billions in daily volume. Solana offers even lower fees and faster finality, but TRON's longer track record, EVM-compatible environment and simpler fee model have kept it at the top of stablecoin transaction counts alongside the newer chain.

*Median Transfer Fee (USD) for transactions involving a stablecoin

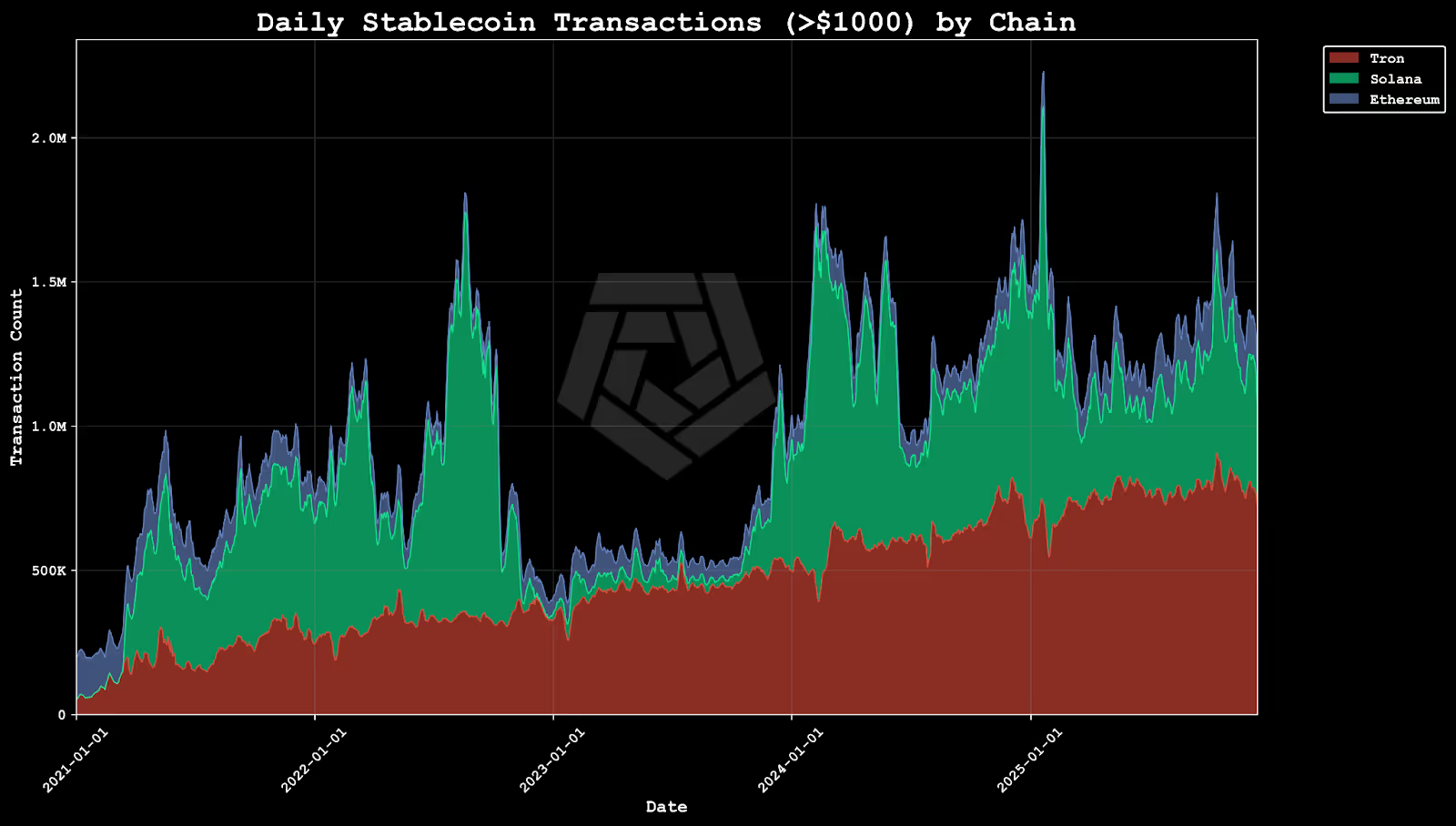

TRON has consistently dominated the share of larger stablecoin transactions since late 2022, frequently accounting for 60-80% of all transfers above $1,000 across the three major chains. Ethereum, which held a significant share in early 2021, has steadily declined to under 15% as users migrated to cheaper alternatives. Solana's share has grown since mid-2024, briefly challenging TRON during periods of heightened on-chain activity, but TRON has maintained its position as the primary network for larger value stablecoin movement.

TRON’s stablecoin transaction activity has proven durable, continuing to climb through both bull and bear cycles. By contrast, Solana’s stablecoin usage has been far more cyclical, falling sharply after the FTX collapse and remaining muted through 2023 before recovering later.

Supply Analysis

Historical Trends and Growth Patterns

TRON's stablecoin supply has grown nearly tenfold since the start of 2021, reaching over $80 billion today. The trajectory of supply growth, monthly issuance and redemption patterns, and the distribution of balances across the network reveal how TRON has cultivated a distinct user base.

Issuance and Redemption Dynamics

Stablecoin supply on TRON expands and contracts through direct issuance and redemption with Tether. When demand for USDT on TRON increases, Tether mints new tokens directly to the network, typically in large tranches to authorized partners and exchanges. Conversely, when users or institutions redeem USDT for fiat, those tokens are burned, reducing circulating supply. The monthly net supply changes on TRON reflect this dynamic: sustained periods of net issuance indicate growing demand for TRON-based USDT, while redemption months often coincide with broader market deleveraging or migration to other chains.

Holder Distribution Characteristics

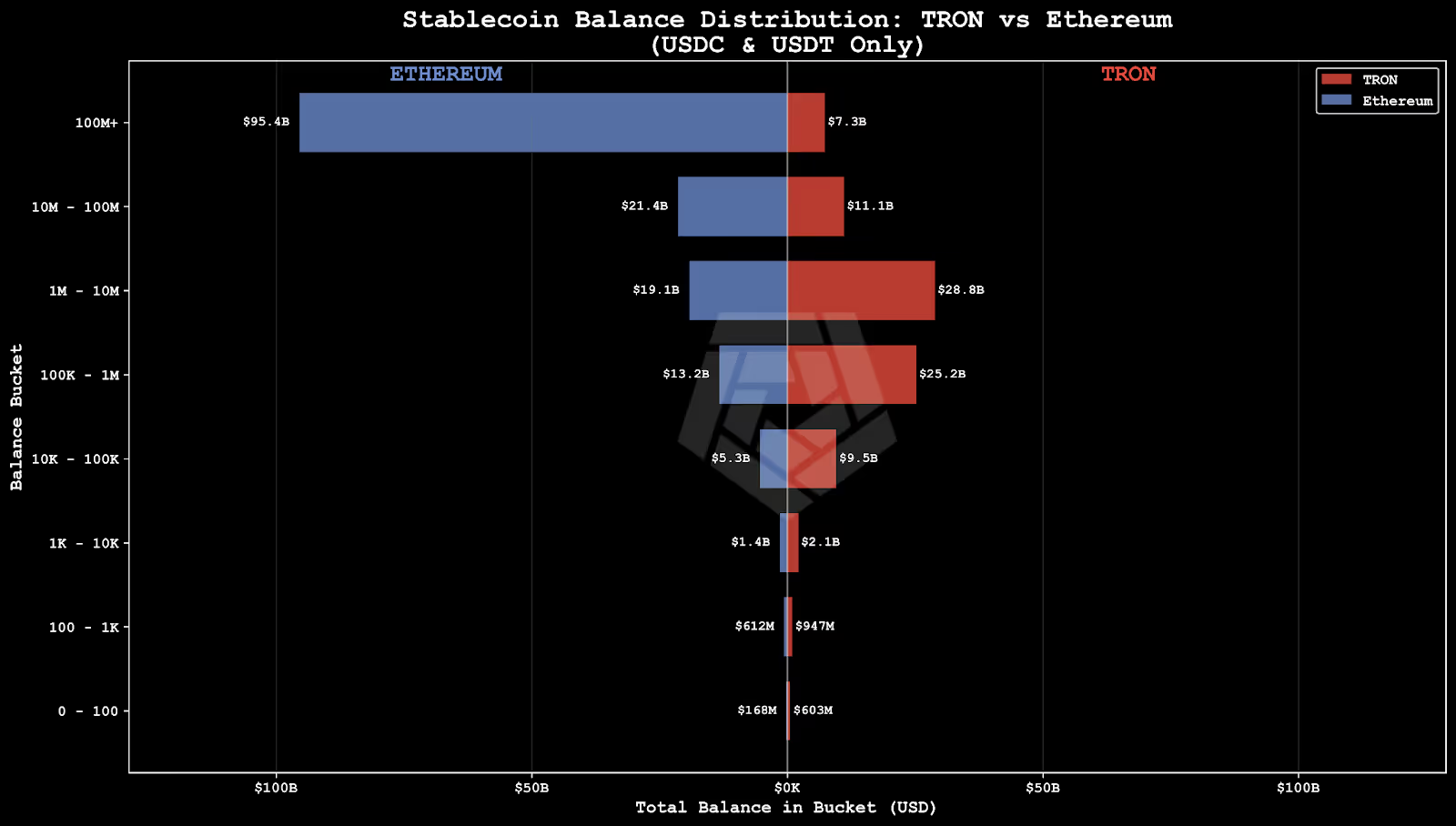

Understanding who holds stablecoins on TRON provides insight into the network's role in the broader ecosystem. By analyzing balance distributions across address cohorts and identifying known entities, a clearer picture emerges of the network's user base and how it differs from Ethereum's more institutionally concentrated holdings.

Ethereum's stablecoin supply is heavily concentrated in wallets holding over $100 million, indicating high institutional concentration, while TRON presents a more normal distribution, with the vast majority of the supply in wallets of $100K to $10M, reflecting a more diverse user base.

Onchain Activity

Transaction Patterns and Metrics

Beyond supply metrics, on-chain activity reveals how TRON's stablecoin infrastructure is actually being used. Daily transaction counts, transfer volumes, and active addresses have all grown substantially since 2021, with compound annual growth rates exceeding 50% across key metrics.

Monthly volume, transactions, and active addresses have all followed strong and steady upward trends since 2021, with compound annual growth rates between 54% and 60%

TRON processes over $21 billion in daily stablecoin volume across 2.2 million transactions, with year-over-year growth of 45.9% in volume and 11.2% in transaction count.

Transfer Flow Characteristics

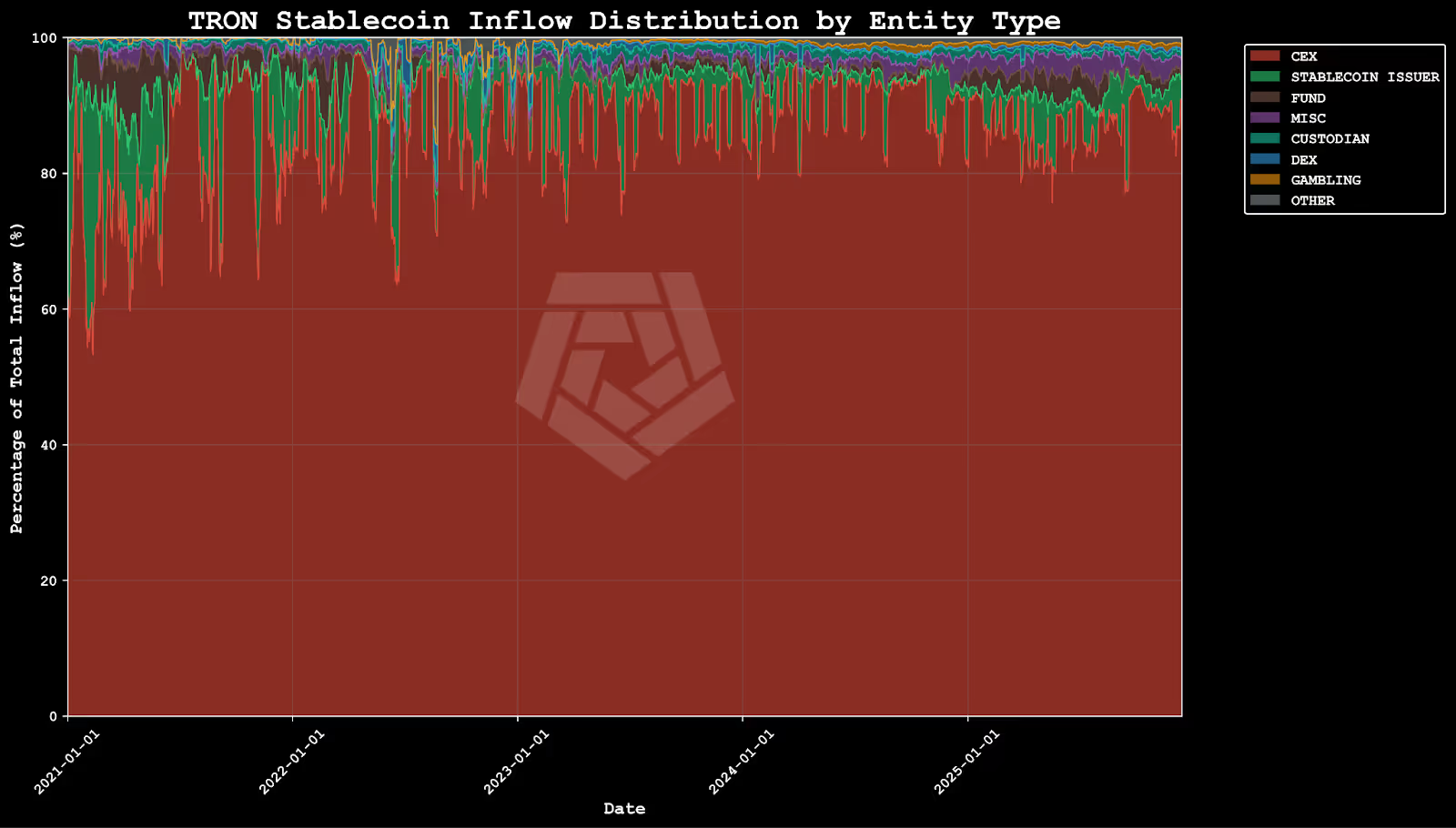

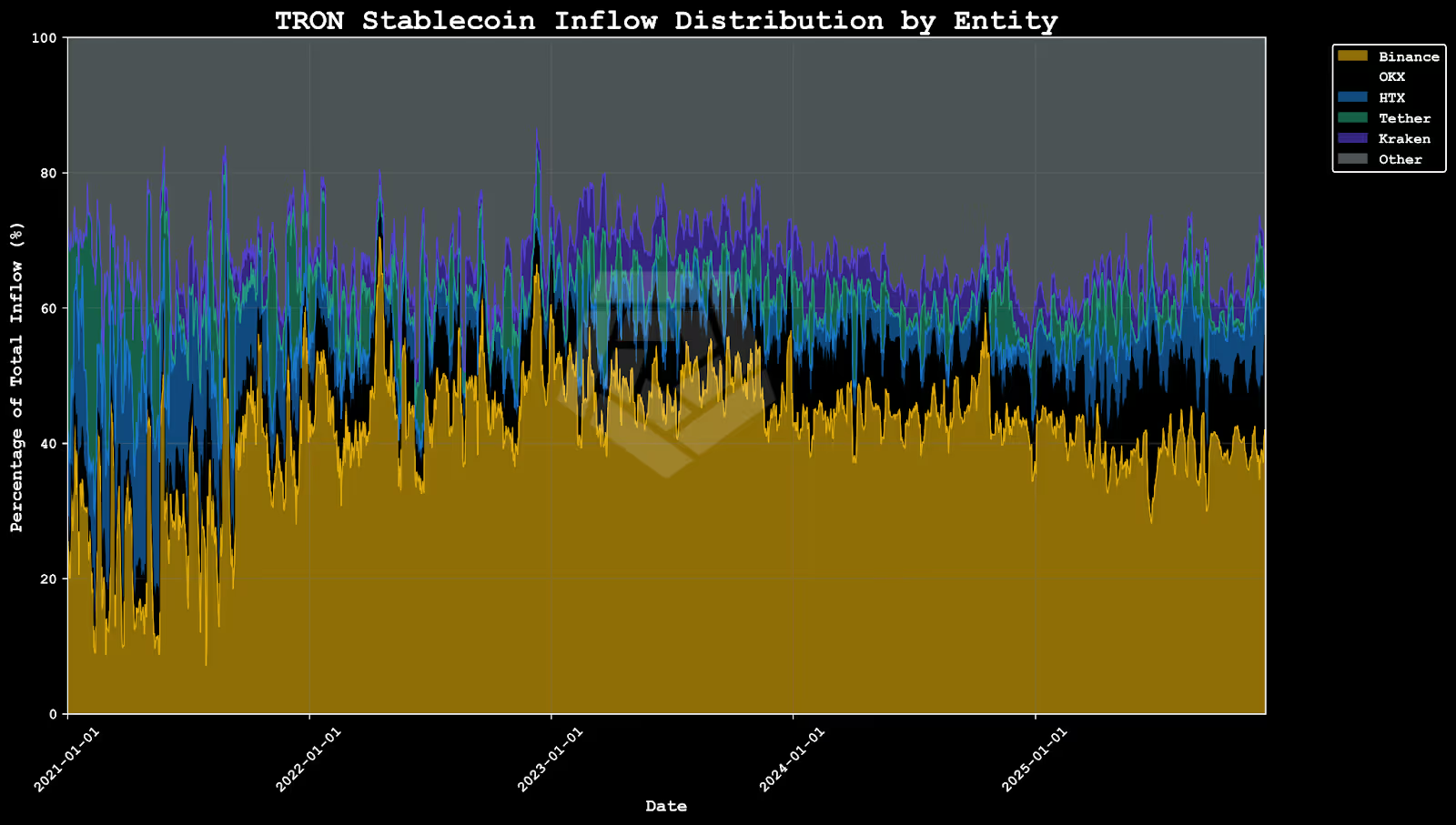

The flow patterns on TRON reveal a network dominated by exchange activity. Centralized exchanges account for the vast majority of inflows, with Binance alone capturing 30-50% of all labeled flows throughout the period.

This pattern reflects TRON’s role as a high-throughput settlement network, supporting stablecoin movement into exchanges and broader financial ecosystems. Users deposit stablecoins to exchanges for trading, withdrawal to fiat, or transfer to other networks, reinforcing the network's position as low-cost infrastructure for moving value between platforms rather than a self-contained financial ecosystem.

Use Cases & Market Dynamics

Primary Use Case Analysis

USDT on TRON serves primarily as a settlement and transfer rail rather than a foundation for on-chain applications. Its low fees and fast confirmations make it particularly attractive for remittances, peer-to-peer transfers, and moving funds between exchanges.

Geographically, activity is heavily concentrated in Asia, which accounts for the largest share of regional volume, with significant usage also observed in North America.

The network turns over approximately 20-30% of stablecoin supply daily as total volume transacted, indicating active utilization rather than passive holding. As stablecoin adoption continues to expand globally, particularly in regions with limited banking infrastructure or currency instability, TRON's positioning as low-cost infrastructure suggests continued growth potential.

Market Behavior Observations

The behavioral patterns on TRON reflect a user base optimizing for efficiency over functionality. Stablecoins flow rapidly through the network, with the majority of volume moving directly to centralized exchanges rather than interacting with DeFi protocols or smart contracts. This velocity remains consistent regardless of broader market conditions, suggesting that TRON's core use case as a transfer layer is relatively insulated from speculative cycles.

The geographic distribution of activity, weighted heavily toward Asia and regions with active crypto trading markets, aligns with the exchange-centric flow patterns. Users treat TRON-based USDT as a utility for moving value cheaply between platforms and jurisdictions, in addition to being an asset to deploy productively on-chain.

Several factors underpin TRON's continued stablecoin growth. The network's fee advantage creates a compelling value proposition for high-frequency users and cost-sensitive corridors, particularly in emerging markets where transaction costs matter more than access to sophisticated DeFi products.

Deep exchange integrations, especially with Binance and other Asia-focused platforms, ensure liquidity and accessibility. Tether's own commitment to the network, evidenced by consistent minting directly to TRON, signals ongoing issuer support. The EVM-compatible development environment lowers barriers for wallet providers and payment processors seeking to add TRON support alongside existing Ethereum infrastructure. As regulatory clarity around stablecoins improves and adoption extends further into payments and remittances, these structural advantages position TRON to capture a significant share of incremental volume.

Conclusion

TRON has carved out a distinct and durable position in the global stablecoin ecosystem. Unlike Ethereum, which serves as the primary venue for DeFi activity and institutional custody, or Solana, which competes on raw throughput and minimal fees, TRON has optimized for efficient, high-volume value transfer.

The network's growth trajectory speaks to the strength of this positioning. A tenfold increase in stablecoin supply since 2021, sustained through both bull and bear markets, indicates demand that transcends speculative cycles. Compound annual growth rates exceeding 50% across volume, transactions, and active addresses suggest organic adoption driven by utility rather than hype. The resilience of TRON's supply during the 2022-2023 contraction, when Ethereum's holdings declined, further demonstrates appeal to users prioritizing cost efficiency.

Several structural factors underpin TRON's competitive position. The fee differential with Ethereum remains substantial, offering meaningful savings for high-frequency users and cost-sensitive corridors. Deep integration with major exchanges ensures liquidity and accessibility. Tether's consistent minting directly to the network signals ongoing issuer commitment. The EVM-compatible development environment reduces friction for wallet providers and payment processors, enabling rapid integration.

The exchange-dominated flow patterns and geographic concentration in Asia and emerging markets paint a coherent picture of TRON's user base: traders moving funds between platforms, remittance senders minimizing costs, and users seeking stable dollar exposure in regions with limited banking infrastructure.

Looking ahead, continued stablecoin adoption in emerging markets represents a significant growth opportunity. Regulatory developments may either validate or constrain this trajectory. Competitive pressure from Solana could erode TRON's fee advantage, though established liquidity and integration depth provide defensive moats.

The evidence supports a clear conclusion: TRON has established itself as essential infrastructure for stablecoin transfer at scale. As stablecoins mature into broader financial infrastructure, TRON is positioned to continue to rapidly grow as a global center of stablecoin activity.