May 28, 2026

at

1:20 pm

EST

MIN READ

A Beginner’s Guide To Stablecoins (2026)

What Are Stablecoins?

Stablecoins are a class of digital asset whose value is pegged to a specified real-world asset, with the most common peg being to the U.S. Dollar. Unlike Bitcoin, whose price can drop 10% in a single day, a USD stablecoin like USDC or USDT is designed to always be redeemable for 1 U.S. Dollar. The strength of this peg comes from several factors, including the reputation of the issuer and the backing of the stablecoin.

Most stablecoins track the U.S. Dollar, but the category is much broader than that. Stablecoins also track other currencies such as the Euro, Singapore Dollars or the Swiss Franc, gold, or even a basket of consumer goods. The defining feature of every stablecoin lies in the peg mechanism, which keeps the token's price from deviating from its intended peg.

How Do Stablecoins Work?

In general, stablecoins maintain their value through one of three methods: holding real-world reserves, using over-collateralized crypto positions, or running an algorithmic ruleset. Each approach involves a different tradeoff between simplicity, decentralization, and resilience.

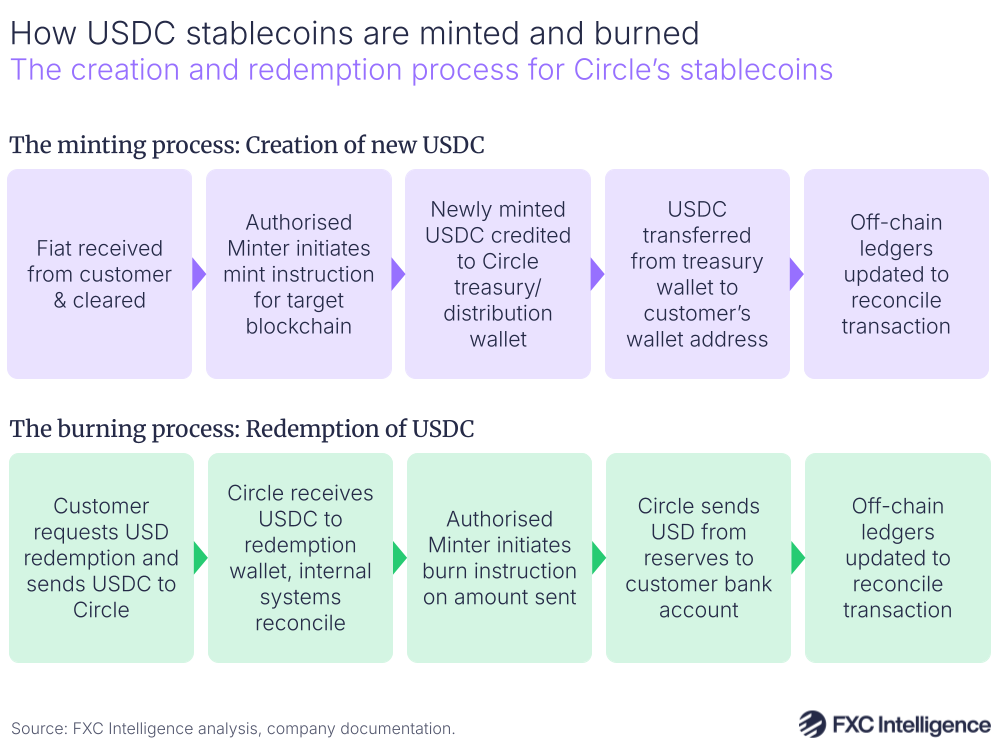

Fiat-backed stablecoins are the simplest in design. For each token in circulation, the issuer holds an equivalent amount of cash or cash-equivalents: U.S. Treasuries, money market funds, overnight repurchase agreements, in a bank or custody arrangement. When someone wants to redeem their stablecoin, the issuer burns the token and wires the fiat to the recipient. The current largest stablecoins by market capitalization, Tether's USDT and Circle's USDC, both utilize this model.

Crypto-backed stablecoins are stablecoins that use other cryptocurrencies - like Bitcoin - as collateral.

Collateralized Debt Positions (CDPs) are a sub-category within the sphere of crypto-backed stablecoins. CDPs function like a loan. You don't "swap" your assets; you lock them up as collateral to "mint" (create) new stablecoins as debt against your own assets.

Due to the volatile nature of crypto prices, these protocols usually demand more collateral than the amount borrowed. This is known as loan-to-value ratio and varies based on the deposited assets.

Sky’s (formerly MakerDAO) DAI/USDS is the best known stablecoin operating under this CDP model. The protocol allows users to deposit a large range of crypto assets, including BTC, ETH, ETH liquid staking derivatives, and more, borrow DAI/USDS up to a certain borrowing limit. When users want to withdraw their collateral, they simply have to repay the DAI/USDS loan plus a stability fee. Do note that for crypto-backed stablecoins, collateral can be liquidated if the collateral falls under the loan-to-value requirements to protect the solvency of the protocol.

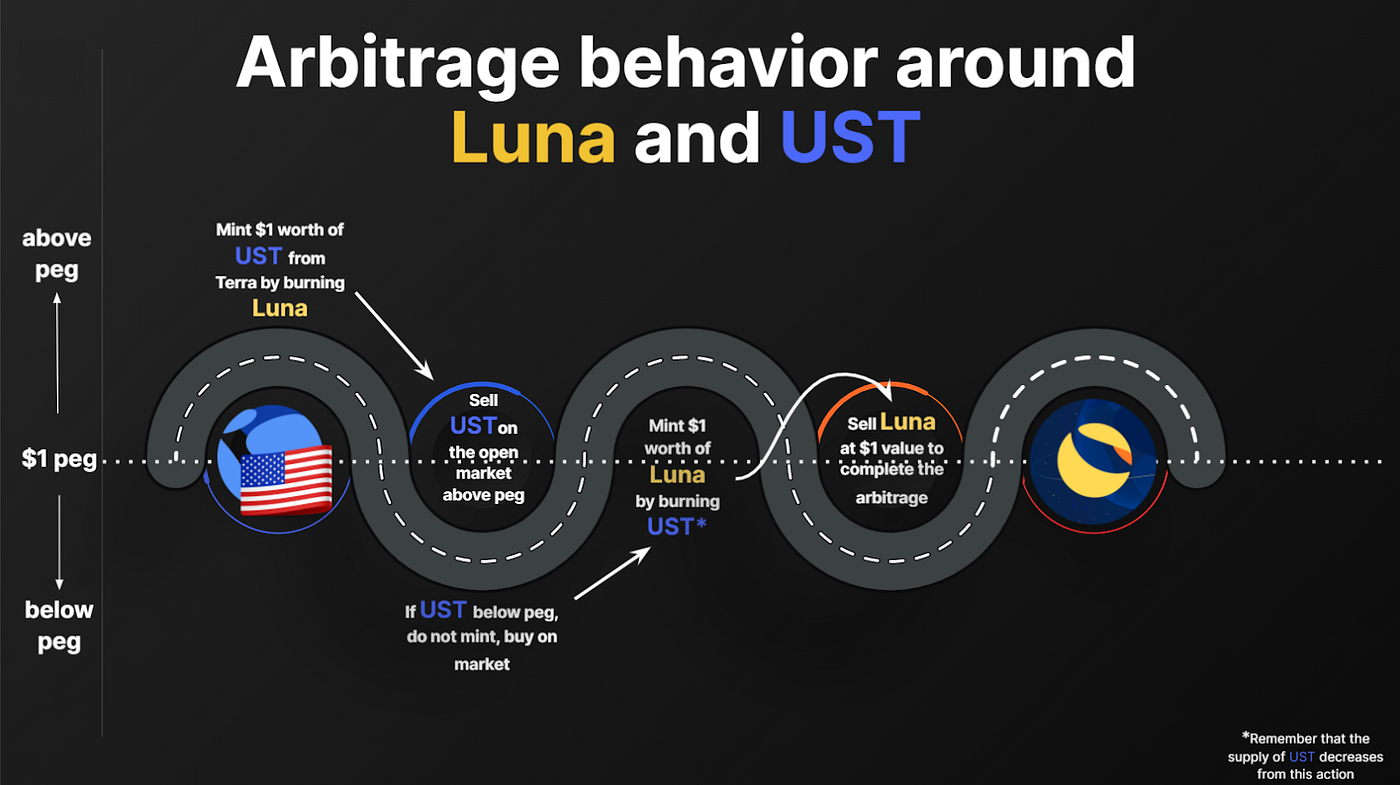

Algorithmic stablecoins operate on a defined ruleset, a set of code and formulas that govern how new supply is created or destroyed to keep the price anchored. Some algorithmic stablecoins are partially collateralized; while others are not. This set of stablecoins remains highly experimental, and its history includes some high-profile failures, most notably Terra-Luna, which famously wiped close to $60 billion in direct losses over just a week in their 2022 collapse.

What’s the Point of Stablecoins?

The core problem stablecoins solve is simple: while blockchains are great at moving value, Bitcoin's price volatility makes it impractical for most types of purchases where the payment made should be of a fixed value. Stablecoins bring fiat-denominated stability onto public blockchains, making them significantly more useful.

Stablecoins are a trading intermediary, allowing crypto traders to exit a volatile position into a stable one without needing to leave the chain or deal with a bank. Additionally, they greatly increase the viability of blockchains as payment rails. In 2025 alone, stablecoin transaction volume hit $33 trillion, overtaking the combined volume of Visa and MasterCard. Moreover, they have also become a savings tool in markets with weak local currencies, where accessing a dollar-pegged asset on a phone offers the kind of financial stability that a local bank account simply cannot.

How to Buy and Hold Stablecoins?

Purchasing a stablecoin is straightforward through any major centralized exchange, which generally supports the conversion of fiat to the exchange’s preferred selection of stablecoins, with most supporting USDT and USDC. The process is identical to buying any other token: create an account, complete identity verification, deposit funds, and swap fiat for the stablecoin of your choice. For more experienced users, swapping on-chain via a DEX is a viable option as well, especially when swapping from another cryptocurrency to a stablecoin.

Holding options range from keeping stablecoins on the exchange itself, which while convenient, relies on the exchange's security, to withdrawing them into a self-custodied wallet. For self-custodial options, a hardware wallet tends to be the most secure option for large amounts, although software wallets allow for easier access to funds. This can be important for DeFi power users, who may wish to move their stablecoins frequently between DeFi protocols.

How to Invest in Stablecoins?

With stablecoins poised to be one of the fastest growing sectors in crypto, it is no surprise that investors are eager to acquire exposure to it. After all, holding a stablecoin is not the same as investing in one, as the token itself is designed not to appreciate.

The most direct and accessible equity route is through shares in stablecoin companies like Circle Internet Group (NYSE: CRCL), the company behind USDC, which completed its IPO in 2025, or other private companies like Tether. Circle earns the majority of its revenue from interest on the US Treasury securities it holds in reserve against USDC's circulating supply. As of Q1 2026, USDC in circulation had grown 28% year-over-year to $77 billion, with reported Q1 revenues of $694 million. The stock trades on the NYSE, making it accessible through any standard brokerage account.

Investors who believe stablecoins will proliferate and want to gain exposure could, for example, wish to express this belief through shares in Circle, or through shares in Tether through private markets, if they so choose.

For exposure to decentralized stablecoins issuers, the majority of them have their own governance tokens, including Sky (SKY) and Ethena (ENA). This makes them easy to acquire, just like any other token, with many of them also available on most centralized exchanges. Investing via the token route does come with its own risks however, with the distinction between the rights of token holders and equity holders, as well as, tokenomics which traditional investors may not be familiar with.

Risks of Stablecoins

Despite being marketed as a token with a stable value, stablecoins are not without their own set of risks.

Reserve risk is the central concern for fiat-backed coins. If the assets backing a stablecoin are partially lost or frozen, confidence in the stablecoin can quickly crumble, causing it to lose its peg. In March 2023, roughly $3.3 billion of USDC's reserves or approximately 8% of the total at the time, were held at Silicon Valley Bank when it collapsed. USDC briefly depegged to $0.878 before the U.S. government stepped in to protect depositors and restore the peg.

Smart contract risk affects both crypto-backed and algorithmic stablecoins. Any exploitable vulnerability in the underlying code can drain reserves faster than governance can respond. This usually presents itself in unlimited or unauthorized minting, where an exploiter mints a large amount of the stablecoin without any backing, before swapping to other assets.

Algorithm failure is a risk specific to algorithmic stablecoins with the clearest case being TerraUSD (UST), which was backed by its own governance token, Luna (LUNA). When the peg was initially lost due to market volatility, user redemptions triggered uncontrolled minting of the LUNA token, which caused its value to crater. The drop spooked UST holders as LUNA was the backing asset for UST, resulting in the infamous death spiral for both UST and LUNA’s value.

USDT vs USDC

At present, the two largest stablecoins by market capitalization are Tether’s USDT and Circle’s USDC.

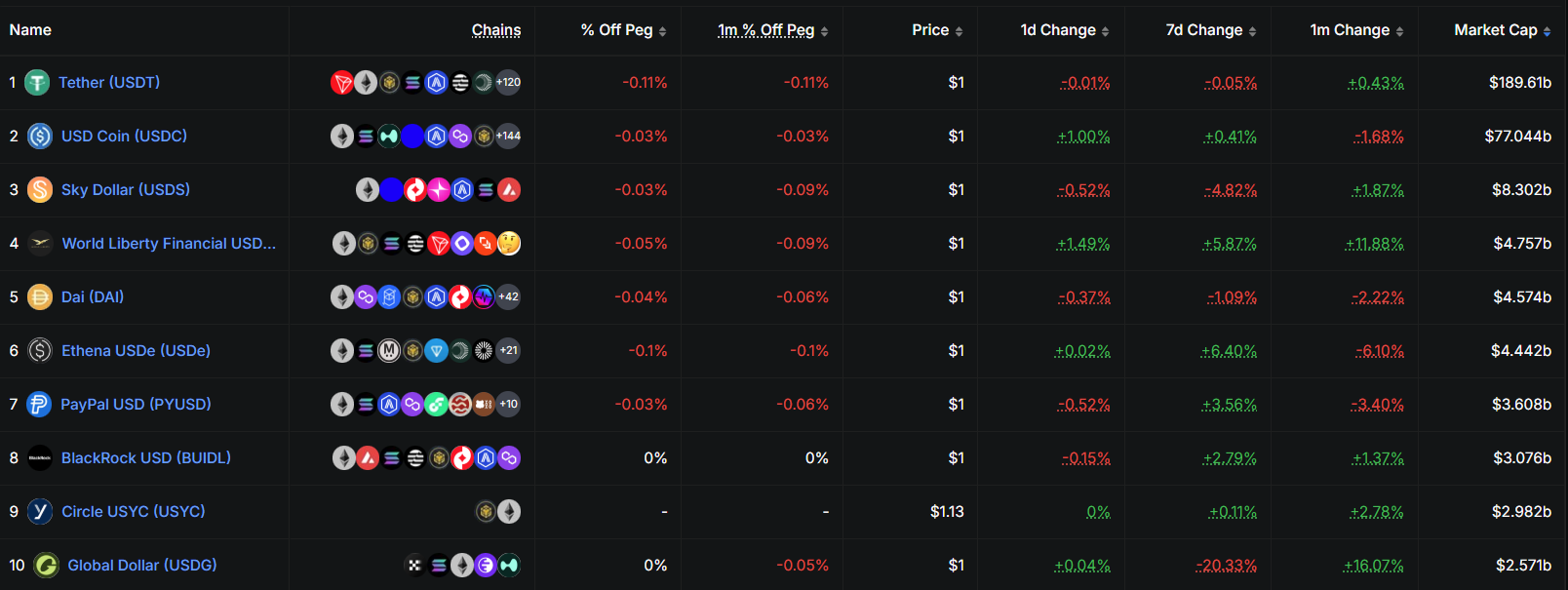

Both tokens are fiat-backed and designed to trade at $1, but they differ in several aspects. Tether’s USDT is the larger of the two, forming approximately 58% of the total stablecoin market at around $189 billion as of May 2026. Tether is incorporated in the British Virgin Islands, although it has recently shifted its headquarters to El Salvador. Tether also holds Bitcoin in its reserves alongside Treasuries, and does not operate under U.S. regulatory oversight in the same way Circle does. As of September 2025 however, Tether launched USAT, a stablecoin compliant with U.S. regulations surrounding stablecoins with a current market capitalization of just under $160 million after eight months.

Circle’s USDC is the more institutionally-oriented product, with reserves managed by BlackRock and consisting primarily of cash and short-dated U.S. Treasuries. USDC holds roughly 24% market share at around $77 billion in circulation. It is the preferred stablecoin in regulatory-sensitive settings, with Circle's Q1 2026 earnings showing that USDC accounted for 63% of stablecoin transaction volume in the quarter. Even on decentralized venues like Hyperliquid, USDC has assumed the role of the default settlement asset.

Other Notable Stablecoins

Beyond the two dominant players, the remaining 18% of the stablecoin market is fragmented across more than 100 other stablecoins. Sky’s USDS and DAI form a large portion of that with their crypto-backed model, with a combined market capitalization of just under $13 billion.

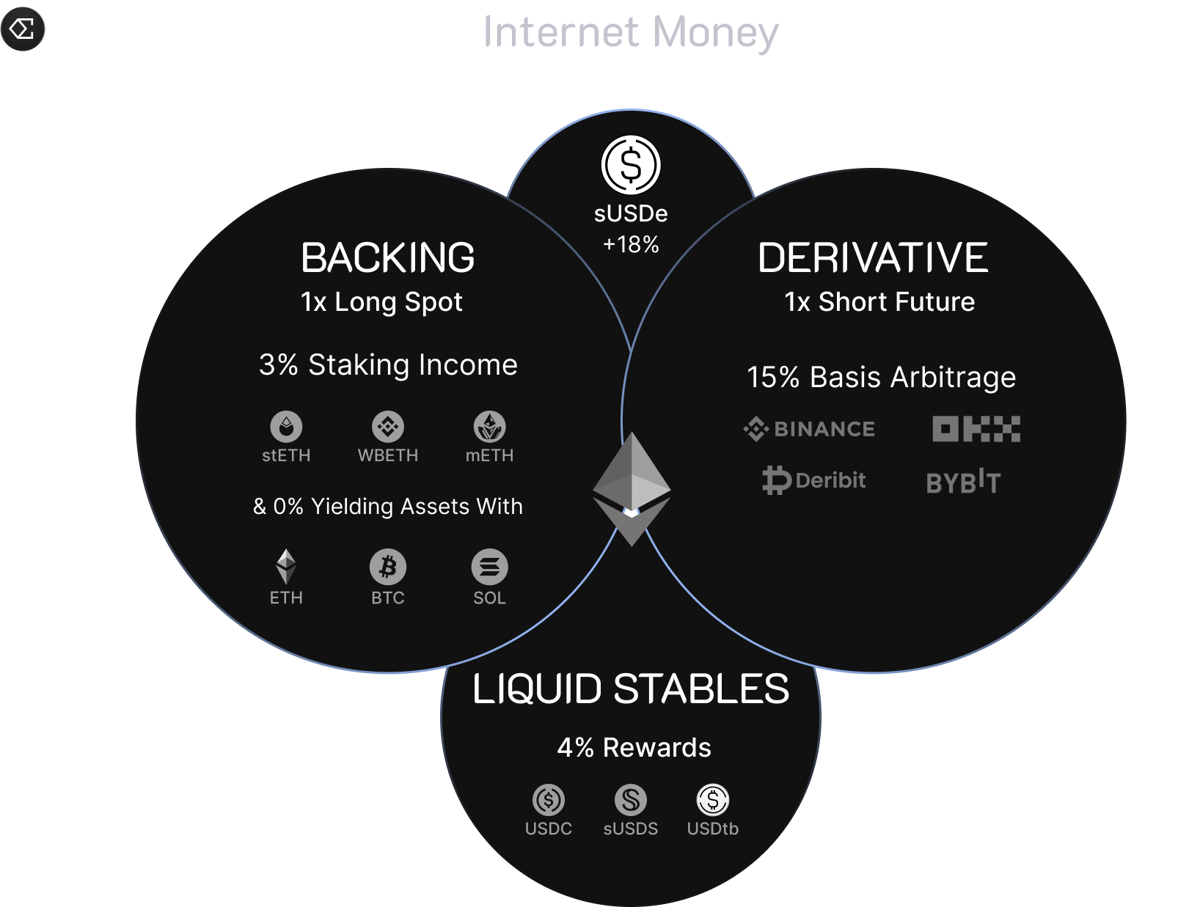

USD1, a newer entrant issued by Trump’s World Liberty Financial, has also risen into the top five by market cap at approximately $4.75 billion, bolstered by the Trump family’s association to the project and their partnerships. On the decentralized end, Ethena's USDe at over $4 billion is now the largest algorithmic stablecoin by a wide margin.

Stablecoin Regulation

The GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins) was signed into law on July 18, 2025, marking the first comprehensive federal framework specifically for payment stablecoins in the United States. The law requires stablecoins to be backed 1:1 with US dollars or equivalent low-risk assets, mandates reserve disclosures, and restricts who may legally issue a payment stablecoin, designating them as "permitted payment stablecoin issuers" subject to oversight from the OCC, Federal Reserve, or state-equivalent regulators.

The GENIUS Act explicitly classifies compliant stablecoins as neither securities nor commodities, carving them out from SEC and CFTC jurisdiction. Its effective date is the earlier of January 18, 2027 or 120 days after implementing regulations are finalized. As of May 2026, the OCC, FDIC, and Treasury's FinCEN have each published proposed rules for public comment.

The CLARITY Act is the broader crypto market structure bill still working through the Senate. Its most contested provision, however, concerns stablecoin yield. It determines whether platforms can offer returns or yield on stablecoin holdings. While the bill was initially delayed over disagreements on how stablecoin yield should be handled, a compromise was reached between Senators Thom Tillis and Angela Alsobrooks in May 2026. The agreement draws a distinction between passive, deposit-like interest, which will be prohibited, and activity-based rewards tied to actual use such payments, transfers, and on-chain participation, which will be permitted.

Despite the compromise, the banking industry, represented by the American Bankers Association (ABA), has raised objections urging the Senate to further tighten prohibition on interest-like rewards, adding friction to the final stretch for the bill.

Conclusion

Stablecoins have quietly evolved from an intermediary for crypto traders into a core element of the digital finance infrastructure. With $33 trillion in annual transaction volume and a landmark regulatory framework in the GENIUS Act, the sector has moved well past the question of legitimacy. Regulatory clarity will continue to shape the landscape, particularly around the contentious issue of stablecoin yield.

For now, stablecoins remain one of the most consequential, if unglamorous, developments in modern finance. They may be designed never to change in value, but their impact on how money moves around the world is anything but static.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)