November 28, 2025

at

4:55 pm

EST

MIN READ

The State of Ethereum: Digital Oil, L2s, TPS, ETFs, DATs

10 years on since the birth of Ethereum, it remains a central pillar of the blockchain ecosystem. Despite growing competition from faster and newer Layer 1s, its dominance in total value locked (TVL) underscores its continued strength in decentralized finance (DeFi). At the same time, Ethereum is navigating significant internal debates regarding the impact of its efforts into scaling the ecosystem, whether its narrative as “digital oil” still holds, and whether Layer 2 (L2) networks are bolstering or cannibalizing its value.

This article unpacks where Ethereum stands today: its performance to date, the evolving role of L2s, its adoption by traditional financial institutions, and what the future may hold for it.

Summary

- Ethereum retains dominant TVL and institutional adoption, but faces debates over value accrual to its token and L2-driven dilution risks

- ETH has underperformed Bitcoin in 2024–2025 despite ETF inflows and growing adoption as a treasury asset

- L2 expansion boosts scalability but raises questions on how much value returns to Ethereum versus staying on rollups

- The upcoming Fusaka upgrade enhances throughput, blob capacity, and node efficiency, positioning Ethereum for a modular, high-throughput future

What Has Happened With Ethereum in 2025?

2025 has been a dynamic year for Ethereum. On the DeFi front, Ethereum solidified its dominance against all other L1s by a huge margin. As of November 2025, Ethereum holds just over $70B in TVL, far outpacing the next two closest competitors, Solana and BNB Chain, which hold only $9.30B and $7.18B in TVL respectively. At its peak, the Ethereum L1 secured almost $100B in value.

At the same time, public companies, beyond just traditional crypto firms, have embraced ETH as a treasury asset, following the success of Bitcoin after the launch of Bitcoin spot ETFs in early 2024. Many of these Ethereum treasury companies pushed aggressively for staking, tapping on native yield to support their accumulation strategies while concurrently securing the network.

On the technical side, Ethereum’s development continued to progress steadily along the Ethereum Foundation’s planned roadmap. The Pectra upgrade went live on Ethereum mainnet on May 7th this year, setting the stage for its next major milestone: Fusaka, which has been scheduled for December 3rd, 2025.

Amidst these changes in the Ethereum ecosystem, debates between investors, developers and analysts have also intensified over whether Ethereum is scaling “enough”, even as L2s boom, concerns about value accrual, and Ethereum’s long-term role in its ecosystem.

Performance Compared With Bitcoin

Despite Ethereum’s dominance in the DeFi space and its acceptance by traditional finance as a viable investment, Ethereum’s performance this year has left much to be desired. Ethereum’s price performance in 2025 continues to diverge from Bitcoin, extending a trend that became pronounced in 2024. While Bitcoin surged to repeated all-time highs on the back of strong ETF inflows and a clear digital-gold narrative, Ethereum has struggled to keep pace.

This divergence has carried into 2025. Even with growing corporate ETH treasuries and expanding L2 activity, the market has been slow to reward ETH, reflecting the ongoing debates around token value accrual, fee compression, and whether L2 scaling dilutes or strengthens the economic thesis for ETH at the base layer.

Still, the narratives surrounding the two remain fundamentally different. Bitcoin’s proposition as a store of value is more mature and easily understood by institutional allocators. Ethereum’s value case, as the settlement and data-availability backbone for an entire modular ecosystem, is broader but also more complex and nuanced, creating a natural divergence in investors’ valuations of the asset.

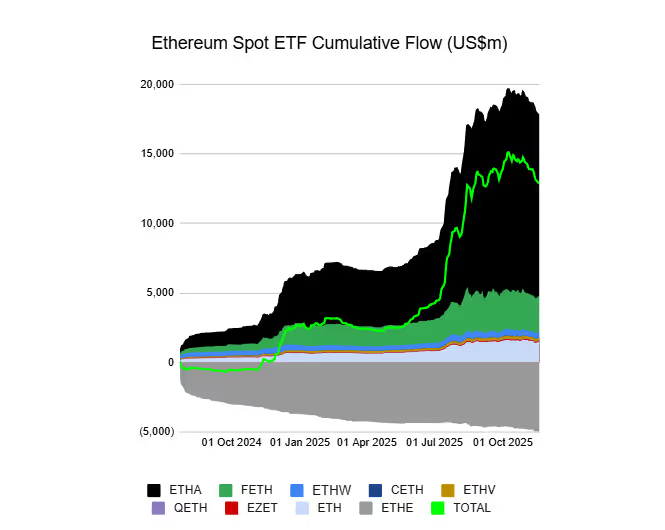

ETF Performance

Ethereum spot ETFs saw a surge in adoption in 2025, fueled by institutional demand and growing recognition of ETH as more than just a speculative asset. These ETFs have drawn both retail and professional investors looking for regulated exposure to Ethereum’s long-term value proposition.

However, inflows have not been uniformly smooth. While Ethereum spot ETFs saw over $12B in inflows over a 6 month period from April to October this year, the ETFs have also since seen strong outflows, triggered by macro instability and geopolitical tensions. On the whole, the Ethereum spot ETFs continue to heavily underperform their Bitcoin counterparts, seeing approximately 20% of the inflows since inception.

Nevertheless, looking at the bigger picture, ETFs continue to serve as a key vector for institutional capital to flow into Ethereum.

Ethereum Treasury Companies

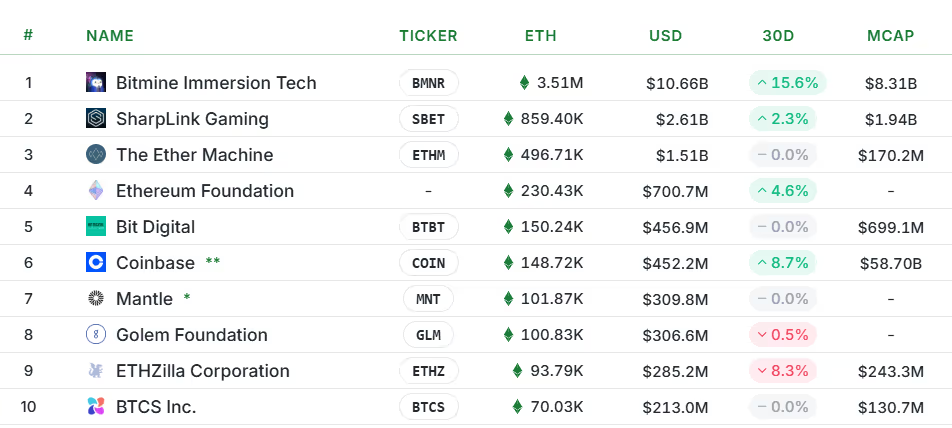

A key development in the ETH investment space in 2025 has been the rise of ETH digital asset treasuries (DATs). Following in the footsteps of Strategy (formerly MicroStrategy), ETH DATs are publicly traded companies that hold Ethereum as a treasury asset, usually forming their core business strategy. Leading ETH treasury companies include:

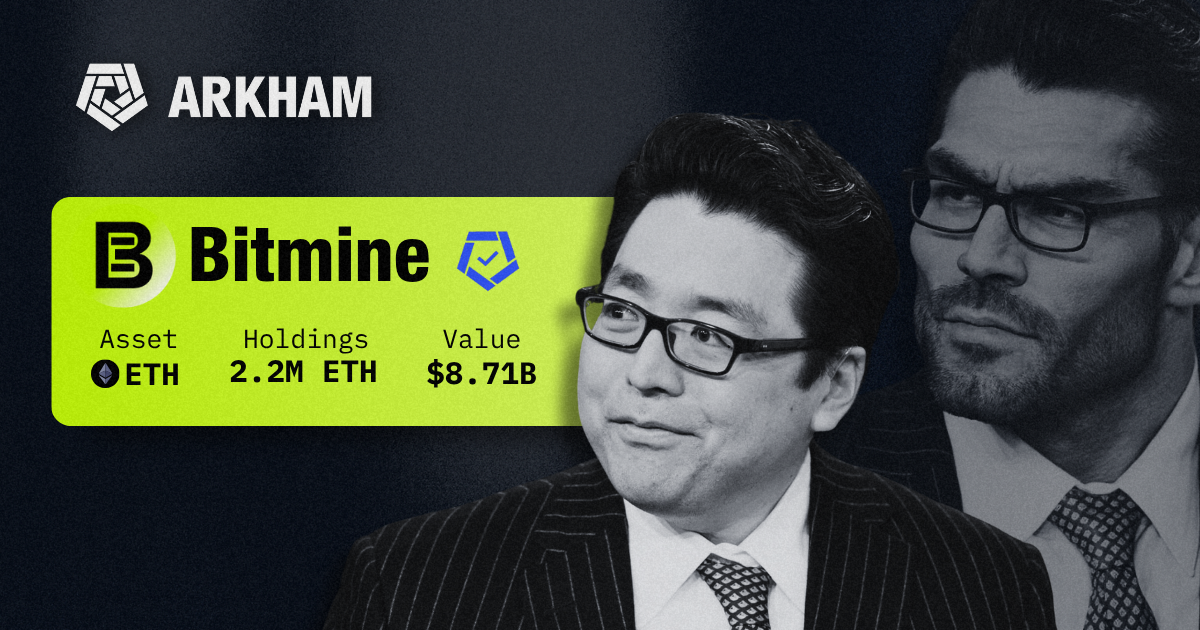

- BitMine Immersion Technologies (NYSE: BMNR): Helmed by prominent traditional finance investor, Tom Lee, BitMine is the current leading ETH treasury company, with a reported holding of 3.51M ETH ($10.66B).

- SharpLink Gaming (NASDAQ: SBET): Led by Ethereum co-founder and ConsenSys founder, Joseph Lubin, SharpLink Gaming was the first established ETH treasury company to launch, with over 859K ETH ($2.61B) held as of November 9th.

- The Ether Machine (NASDAQ:ETHM): The Ether Machine went public via a merger with SPAC, Dynamix Corp, led by Andrew Keys, the former Head of Business Development at ConsenSys.

- ETHZilla (NASDAQ: ETHZ): ETHZilla pivoted and rebranded from their biotechnology roots to focus on ETH accumulation, having now accumulated over 102K ETH ($306M).

Beyond the top players, several dominant crypto companies also hold significant portions of their treasury in ETH, including centralized exchange, Coinbase, and Bybit-backed Ethereum L2, Mantle.

Ethereum treasury companies are vital as they act as a bridge between traditional finance and the Ethereum ecosystem. By raising capital in traditional markets (via stock sales or convertible bonds), they create sustained, institutional-level buying pressure for ETH.

Crucially, many actively stake their ETH holdings or deploy them in DeFi protocols to generate yield, which not only provides a stable income stream for the company but also boosts the network's security and on-chain liquidity.

But perhaps more importantly, the rise in ETH DATs also highlights the institutional interest in the space, further cementing Ethereum legitimacy as an investment asset and its long-term financial stability.

Tom Lee: Ethereum’s Michael Saylor

One of the most influential forces in Ethereum’s market dynamics this year has been Tom Lee, the prominent traditional finance investor who took the reins at BitMine Immersion Technologies, rapidly transforming it into the largest ETH treasury company to date. Beyond BitMine’s aggressive accumulation strategy, which included the use of call options to increase their exposure to ETH, Tom Lee’s very public stance on his bullishness on ETH was instrumental in galvanizing institutional interest in the asset class. In many ways, Tom Lee could be considered the Michael Saylor of Ethereum.

Lee has conducted numerous public interviews on this subject, in which he argues that Ethereum was entering a “structural repricing phase”. He positioned BitMine’s strategy as a multi-year bet on Ethereum’s role as the settlement backbone of global digital assets. Wider market adoption of this narrative, coupled with BitMine’s constant buying pressure, may have played a role in the increase of ETH’s price and market cap, with the price of the asset rising from the mid-2000s in late June to just above prior ATHs in late August.

Lee also became a vocal advocate for the thesis that stablecoin growth is fundamentally tied to Ethereum’s long-term value, a narrative that gained further traction as global stablecoin supply hit new highs in 2025. According to Lee, stablecoins represent the “ChatGPT moment” for crypto, highlighting the potential to onboard the masses and drive mainstream adoption of the asset class. Under this thesis, Ethereum forms the natural settlement layer for that growth, with each incremental dollar of stablecoin supply indirectly increasing demand for blockspace and strengthening the economic loop that ultimately accrues value to ETH. This thesis is further bolstered by the rise in interest in tokenized assets, in stocks, commodities, treasuries and more, the majority of which is secured by the Ethereum blockchain.

In all, BitMine’s strategic ETH accumulation and Tom Lee’s high-conviction public commentary contributed to a powerful flywheel for ETH’s narrative. They helped reshape investor expectations of ETH and reinforced Ethereum’s narrative strength, especially in the traditional finance community, at a time when questions around value accrual and L2 fragmentation were otherwise dominating discourse.

The “Digital Oil” Narrative

Another one of the most persistent metaphors for Ethereum is that it is “digital oil” or “crypto-fuel.” Just as oil powers industries in the physical world, many investors view ETH as the engine fueling Web3. Unlike Bitcoin which is often touted as "digital gold", primarily a passive store of value, ETH’s value is derived from its fundamental utility as gas for all transactions, smart contracts, decentralized applications (dApps), rollups, and more, across the Ethereum and L2 ecosystems. This analogy largely stems from EIP-1559 and its deflationary pressure on the ETH supply, where fees are partially burned, effectively removing the "oil" consumed from circulation.

But the analogy also has its critics. Oil’s price, when adjusted for inflation, tends to be relatively stable in the long run, except during geopolitical crises where oil price spikes. A concern for Ethereum is that if its utility becomes commoditized, especially as L2s grow, its token may capture less of the value generated in the broader ecosystem. Additionally, critics also argue that L2s may internalize too much revenue, through sequencer fees and MEV, without sufficient value accruing back to ETH holders.

However, proponents counter that Ethereum’s modular future, with L1 as a data availability layer and L2 as execution layers, enhances its long-term relevance. In this view, ETH is more akin not just to oil, but to pipeline infrastructure or the land on which digital cities (L2s) are built, in the sense that they are essential, but not directly monetized in the same way.

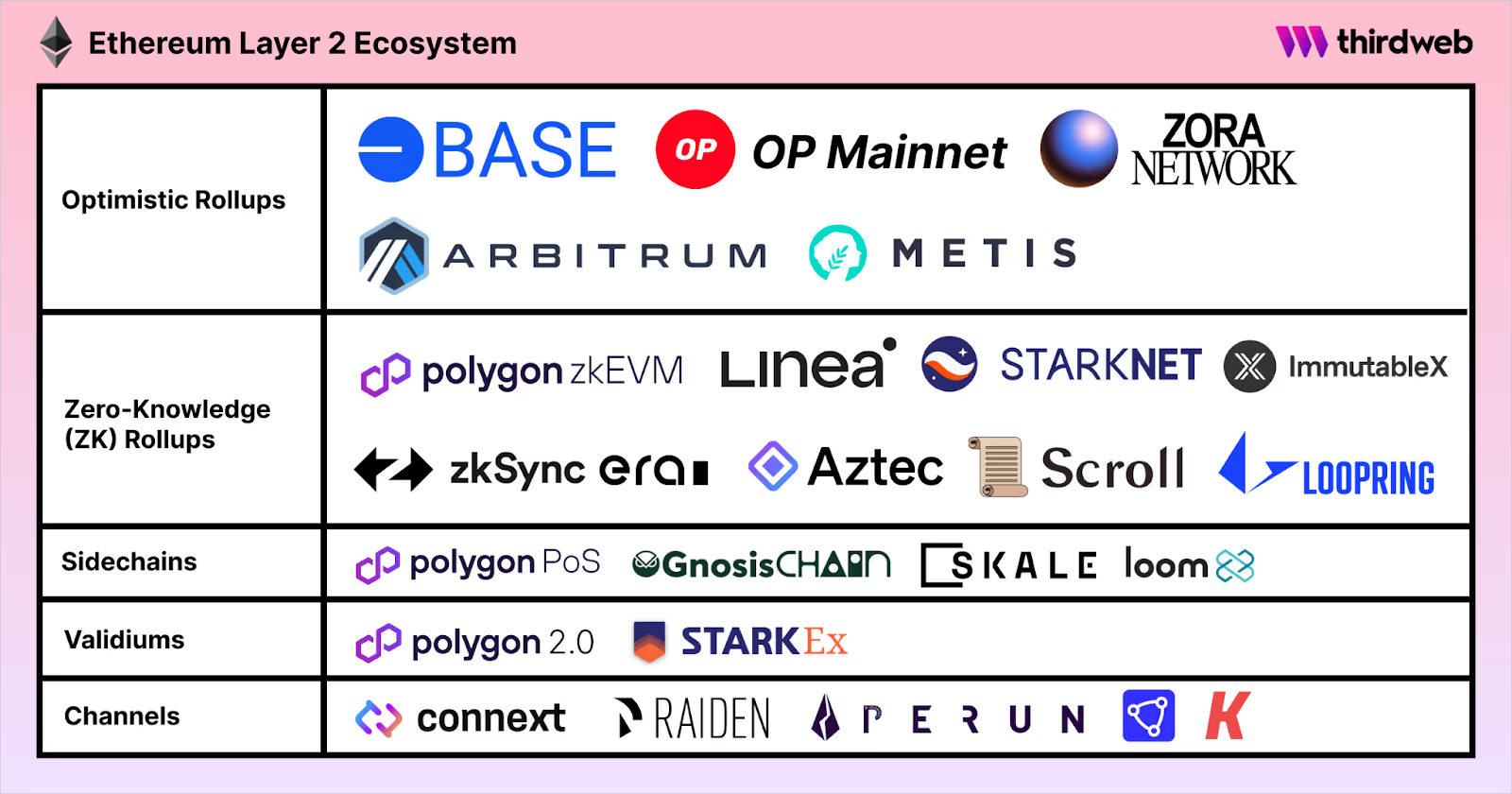

Ethereum and Layer-2s

Ethereum’s L2s, such as Arbitrum, Optimism, ZkSync and many more, form a core part of its scaling strategy. By offloading execution from Ethereum’s base layer, they reduce congestion, lower fees, and scale the ecosystem’s transaction capacity. These L2s have seen explosive growth over the past two years, driven by users seeking cheaper and faster chains. However, this proliferation has also raised a fundamental question concerning how much of this newly generated economic value actually flows back to Ethereum, versus being captured by the L2s themselves.

Although some of the value flows back through ETH staking and blob fees, which are the fees paid by L2s to post data on Ethereum, critics argue that L2 sequencers operators, who order transactions on the L2, and L2 validators may internalize a disproportionate share of Maximal Extractable Value (MEV) and sequencer revenues, limiting the value accrued to ETH holders. Studies in 2025 on MEV have shown that optimistic MEV, such as arbitrage and speculation, remains a major gas consumer on L2s like Base and Optimism. On the other hand, L2 proponents argue they are responsible for strengthening Ethereum’s moat. They rely on Ethereum’s security and data availability while enabling much higher transaction throughput, effectively scaling Ethereum’s utility without compromising decentralization.

Furthermore, EIP-4844, which was implemented in 2024’s Dencun upgrade, enabled further L2 scaling via blobs, which are large, temporary data units. These blobs allow L2s to post data to Ethereum in a way that’s cheaper per byte than traditional calldata, significantly lowering L2 costs and further reducing the value that flows back to the Ethereum L1 from its L2s.

Ethereum’s Fusaka Upgrade

Ethereum’s next big upgrade, the Fusaka upgrade, has been scheduled for December 3rd, 2025, representing a major inflection point in Ethereum’s roadmap. Key technical features include:

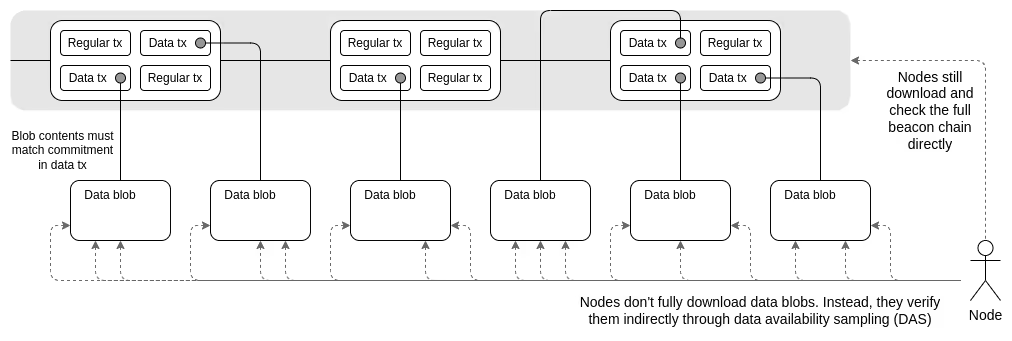

- PeerDAS (EIP-7594): This protocol allows validators to sample parts of blob data rather than download the full blob, reducing bandwidth and storage demand

- Blob Parameter Only (BPO) Forks: Immediately after Fusaka, two planned forks will increase the per-block blob target and max from 6/9 to 10/15 (BPO1) and then to 14/21 (BPO2)

- Higher Gas Limit (EIP-7935): Set default gas limit to 60 million, enabling more transactions per block

- Verkle Trees: For more efficient state commitments and verification, especially benefiting light clients

- EVM Optimizations & Precompiles:

- EIP-7951: Adds support for secp256r1 curve, enabling integration with hardware security modules (e.g., Apple Secure Enclave, FIDO2)

- EIP-7939: Introduces a CLZ (Count Leading Zeros) opcode to make bit-counting and compression more gas-efficient

- Engine API Adjustments: Refinements to the interface between the consensus and execution layers to support these updates

The impact of Fusaka is expected to be substantial. By reducing the cost and complexity of running a node, PeerDAS may significantly lower operational barriers, allowing a wider range of participants to validate the network and reinforcing Ethereum’s decentralization. The expanded blob capacity promises cheaper and more scalable data availability for rollups, which could directly translate into lower transaction fees and higher throughput on L2 networks. As blob supply increases, L2s gain more room to post their data at consistent, predictable costs, a direct benefit to end users who often experience fee fluctuations during periods of congestion.

On the base layer, the higher gas limits and EVM optimizations give developers more flexibility and headroom to experiment with complex applications, while Verkle Trees set the stage for a more lightweight and sustainable network architecture. Altogether, Fusaka positions Ethereum to serve as a more robust, efficient settlement and data-availability layer at a moment when the ecosystem is rapidly expanding. It is not just an incremental upgrade but a foundational shift that aligns Ethereum with the demands of a fully modular future.

Conclusion

As of 2025, Ethereum finds itself at a pivotal moment. Its robust DeFi presence and institutional adoption remain strong, but so too are existential questions concerning Ethereum’s long-term economic sustainability and the nature of its relationship with its L2s.

The Fusaka upgrade may be Ethereum’s answer to many of these concerns. By boosting blob capacity, raising gas limits, and introducing PeerDAS, Ethereum is fundamentally retooling itself to better support a high-throughput, modular ecosystem, where L2s play a central role but remain anchored by the security and decentralization of Ethereum L1.

Whether ETH continues to live up to its “digital oil” narrative will depend on how value is shared among layers, how gas and data costs evolve, and how the broader economy of tokenized assets (DATs) and institutional participation grows.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)