March 31, 2026

at

8:45 am

EST

MIN READ

A Guide to Crypto Payment Rails (2026)

Over the past decade, the way money moves around the world has started to change in a very real and visible way. Systems that used to be the exclusive domain of banks, central institutions, and clearing networks are now being challenged by new payment rails built on public blockchains. These networks move money across the globe in real time, and for the first time, users can actually see where their money is at every step.

What is happening is more than just a technological upgrade, it is a shift in the financial system’s underlying infrastructure. Stablecoin-based payment rails, once considered experimental, are now used by fintech apps, enterprises, and even governments as part of their actual payment infrastructure. As more transactions move on-chain, we are transitioning from slow, message-based systems run by intermediaries toward networks where value transfers directly and settlement occurs on a shared ledger.

But, this shift also raises new questions. Faster and cheaper payments sound great, but they come with a catch. If every transaction is visible in real time, what happens to privacy? How will regulators and compliance teams keep up?

Summary

- Global payments are gradually moving away from opaque systems like SWIFT and toward blockchain networks that settle value quickly and operate around the clock

- Stablecoins have become the primary asset used for on-chain settlement, driving trillions in transaction volume and gaining traction in fintech and corporate use cases

- Crypto rails offer major advantages in cost, speed, and programmability, but they still face hurdles related to scalability, regulation, and the tension between transparency and privacy

- The future of payments will likely include both fully transparent blockchains and privacy-enabled rails, but the trend towards increased on-chain visibility is clear

What are Payment Rails?

Payment rails are the underlying systems and networks that allow money to move between parties. They define the rules, messaging formats, settlement processes and institutions responsible for executing a transfer of value. In the same way that physical rails transport goods across geographies, payment rails transport financial value across the global economy.

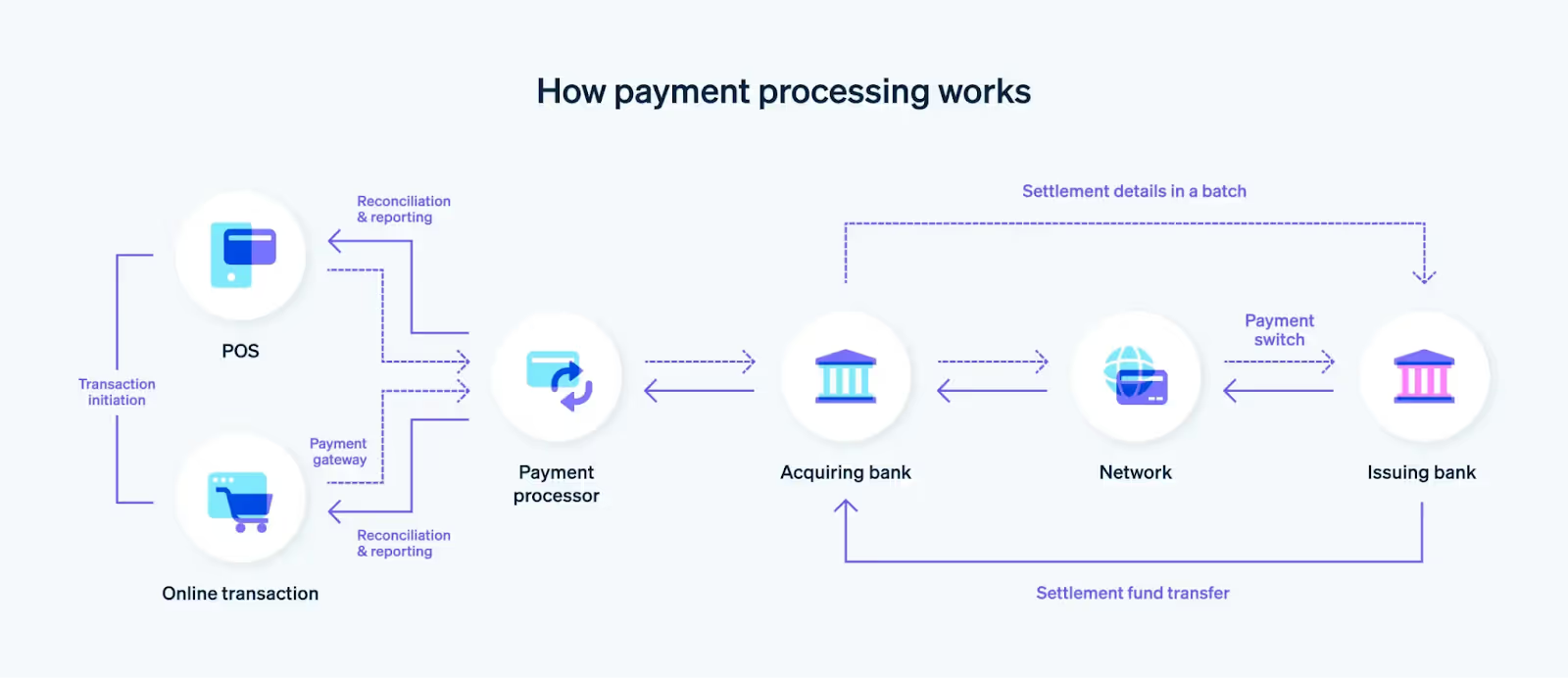

These rails can be operated by banks, for example ACH, card networks such as Visa and Mastercard, government infrastructure including Fedwire and SEPA, or decentralized networks such as Ethereum and Solana. While end users interact through apps or bank interfaces, the actual movement of funds depends on the operational design of said payment rails. This includes whether they are batch-based or real-time, centralized or distributed, and domestic or cross-border payments.

How do Traditional Payment Rails Work?

Traditional payment rails generally rely on a mixture of centralized banking systems, messaging networks, and clearing houses. The mechanics vary across jurisdictions, but most follow a multi-layered model where institutions exchange messages instructing funds to be moved, followed by delayed settlement between accounts held at central banks.

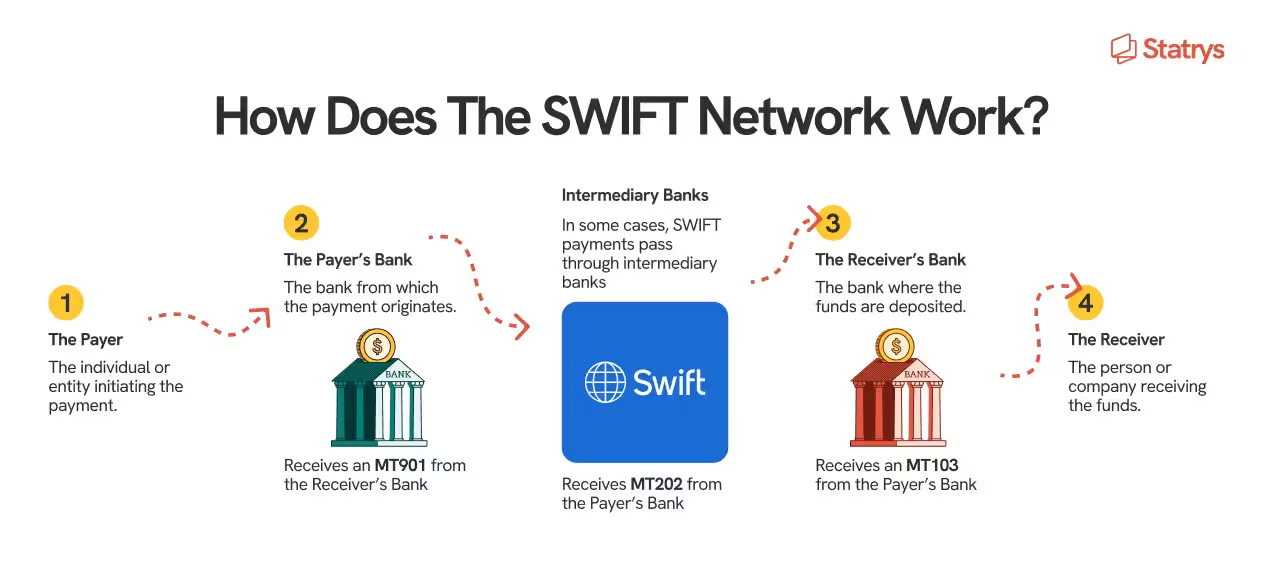

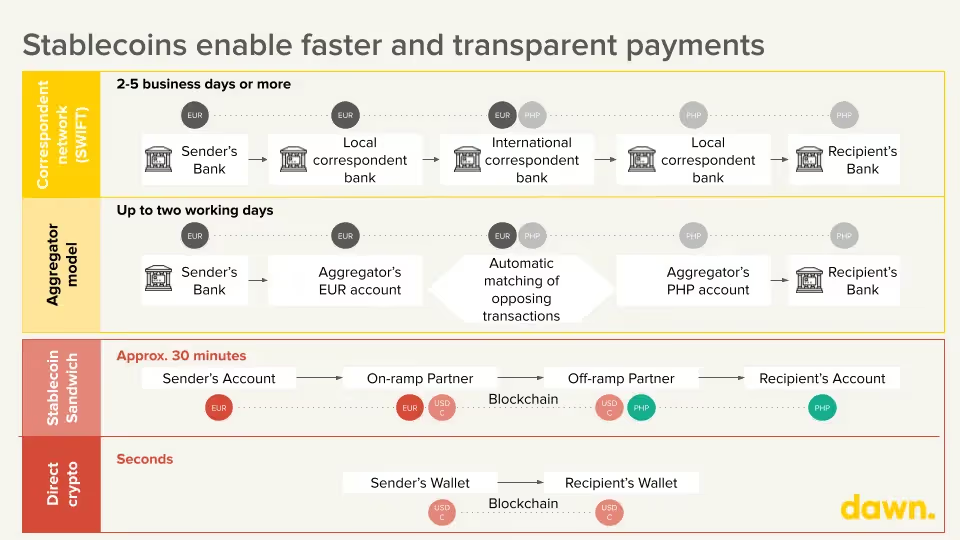

The Society for Worldwide Interbank Financial Telecommunication (SWIFT), is the backbone of cross-border payments. Contrary to popular belief, SWIFT does not move money. Instead, it provides secure messaging standards such as the MT103 format that allow banks to communicate payment instructions. A SWIFT payment requires correspondent banks to process the instruction, deduct fees, and settle balances through Nostro and Vostro accounts. Nevertheless, it is estimated that the entire world’s GDP passes through SWIFT’s networks roughly once every three days, highlighting the key role they play in the global economy.

The limitations of SWIFT are largely structural. Cross-border transfers experience high latency of one to three days due to the need to coordinate with intermediary banks. Intermediary banks and services can also add additional costs, in the range of USD 20-50 in fees, to a single transfer. Additionally, senders often are unable to trace where funds are along the transfer process, until they arrive.

Other notable payment rails include:

- Automated Clearing House (ACH): Used in the United States for domestic payments. ACH processes payments in batches, for low-cost recurring payments. These transfers do not execute in real-time.

- Fedwire and other Real-Time Gross Settlement (RTGS) systems: Settle high-value, time-critical payments individually and in real-time with finality, used for interbank transfers and financial market transactions globally.

- Card Networks: Networks like Visa and Mastercard authorize and route transaction data between the customer's bank and the merchant's bank to facilitate point-of-sale and e-commerce purchases globally

- Single Euro Payments Area (SEPA): Standardizes Euro-denominated payments, making cross-border bank transfers between the 36 participating EU countries as easy and inexpensive as domestic transfers.

Each of these systems is centralized, regulated, and built around institutional trust rather than cryptographic finality. While they serve critical roles in modern finance, they struggle to meet the demand for global, 24/7, internet-native commerce.

Issues with Traditional Payment Rails

Traditional payment rails still run the world, but their legacy technology is beginning to show. Many of the systems still in use today were built for a slower, pre-internet financial world. As a result, they rely heavily on intermediaries such as correspondent banks, clearing houses, and card networks. Each step adds fees and latency. This is especially noticeable with cross-border payments, where costs can easily exceed 5 percent and settlement often takes days.

Batch-based processing and limited operating hours also create friction for modern businesses that expect money to move as quickly as data. Delayed settlement ties up liquidity, slows financial operations, and increases operational overhead.

Traditional payment rails also face the issue of access and visibility. Banks, central banks, and card networks have tight control over these systems, which slows down innovation and makes outages or sanctions ripple quickly across the global economy. For end users, tracking a payment is still surprisingly difficult and often requires manual follow-ups or reliance on support teams to locate stuck funds.

What are Crypto Payment Rails?

The rise of crypto payment rails marks a significant shift, utilizing blockchain networks to enable the direct, intermediary-free transfer of value. Instead of merely sending instructions to banks, these rails achieve direct value settlement on a distributed ledger without the need for intermediaries.

In a blockchain environment, transactions are generally verified by a decentralized network of validators. Once confirmed, they become a permanent part of an immutable ledger, establishing a global, shared consensus on account balances. This fundamentally different approach offers several key advantages, including the potential for instant finality on certain chains, 24/7 global settlement, programmability via smart contracts, and complete transparent auditability. However, different blockchains present a range of trade-offs concerning throughput, cost, and decentralization.

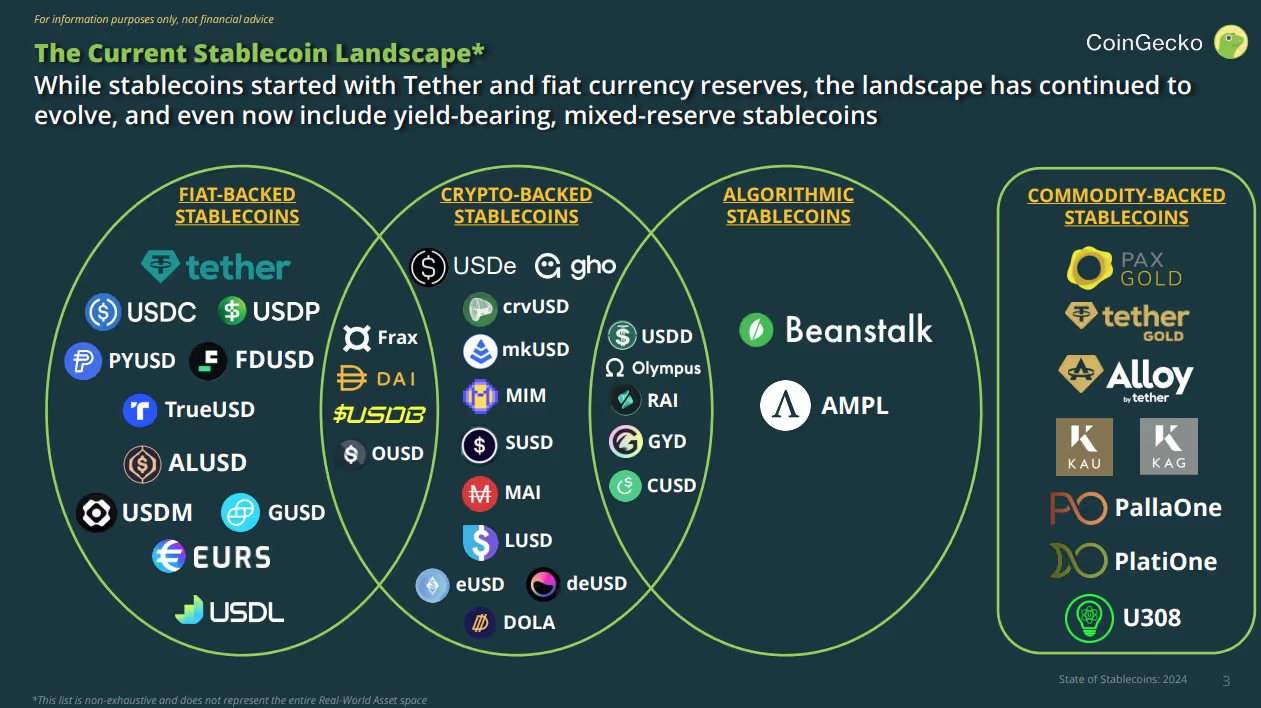

While native cryptocurrencies like ETH or SOL are also usable for transactions, stablecoins have emerged as the preferred medium for settlement. These digital assets are pegged to fiat currencies, combining the price stability of traditional money with the advanced programmability inherent to crypto rails. Leading examples of stablecoins include Tether’s USDT, Circle’s USDC, Paypal’s PYUSD, and more.

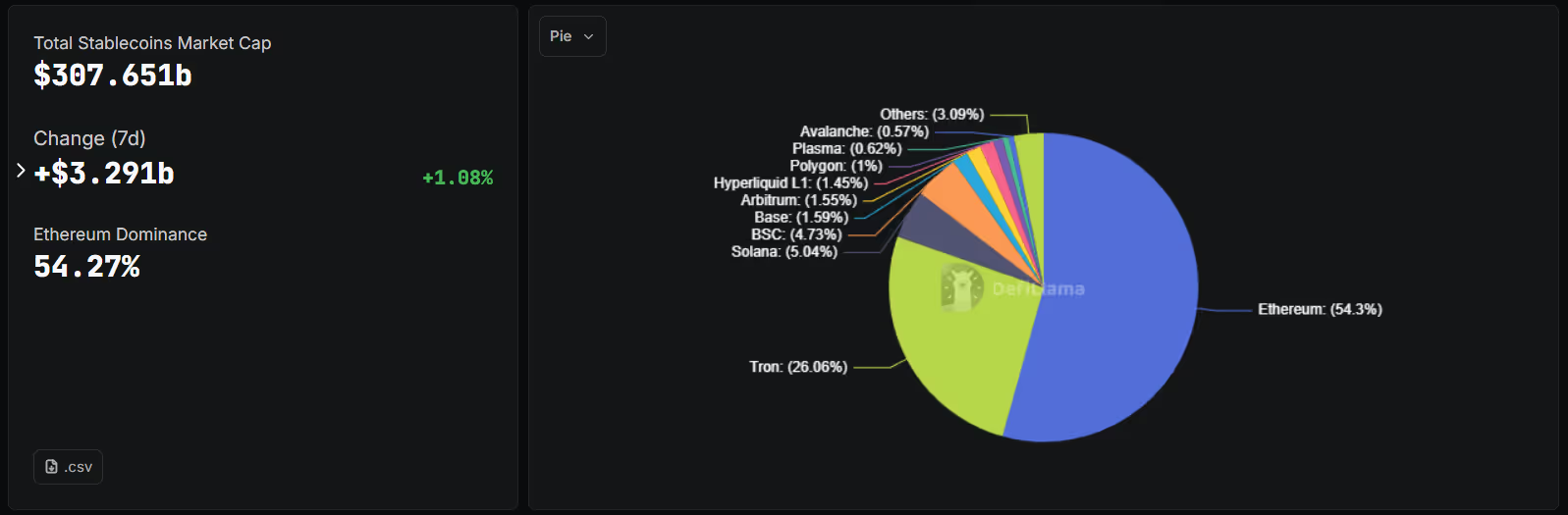

Across the major L1 networks, Ethereum remains the leading platform for stablecoin activity and is widely used as the settlement layer by institutional-grade issuers. In many emerging markets, Tron has also become a significant channel for USDT transfers due to its inexpensive transaction fees. Layer 2 networks such as Base, Optimism, and Arbitrum, along with high throughput L1s like Solana, offer additional low cost settlement options, which also position them as appealing venues for stablecoin activity.

These developments illustrate a growing real-world economic impact. Notably, stablecoin transaction volume exceeded $18 trillion US dollars in 2024, a figure that surpasses even Visa’s annual volume. Adoption is rapidly accelerating among major fintech companies, with players like Stripe, PayPal, Revolut, and Nubank incorporating stablecoin payments. The cost savings is most evident in cross-border remittances, where crypto often settles within seconds at a cost of under 1 percent, significantly lower than the global average remittance fee of 6.49% reported by the World Bank.

Benefits of Crypto Payment Rails

Crypto payment rails provide several advantages over traditional systems. Transactions on high-throughput chains can cost fractions of a cent, enabling micro-transactions and cost-efficient global transfers. Settlement is also near-instant and functioning 24/7, increasing its speed and availability to its users.

Furthermore, developers can leverage smart contracts to build advanced financial features, such as automated escrow, conditional payments, recurring transfers, or streaming payments. These features also remove the need for trusted intermediaries, something that is not possible in traditional financial systems.

For regulatory and financial oversight, leveraging the blockchain provides unparalleled transparency. The permanence and immutability of blockchains facilitates real-time auditing and fraud detection, a key requirement for compliance.

Finally, crypto payment rails foster interoperability by establishing a common, shared settlement layer. This allows wallets, exchanges, and decentralized finance (DeFi) protocols to seamlessly integrate, significantly increasing financial composability and reducing friction across the entire digital asset ecosystem.

Issues with Crypto Payment Rails

However, crypto payment rails are not without their faults. In fact, they come with their own set of challenges, with the most obvious being network congestion. When activity spikes on chains like Ethereum, transaction fees can climb quickly, making the network temporarily impractical for smaller payments. This unpredictability complicates real-world adoption.

Regulatory uncertainty poses another obstacle. Stablecoins, which are the main asset used for on-chain settlement, are not treated consistently across jurisdictions. Some countries classify them as digital money, others treat them as securities, and many have yet to define them at all. This inconsistency slows broader institutional adoption.

Privacy also remains a complex issue for users who may not necessarily wish to have all of their transactions publicly tracked. Blockchains are transparent by default, which is useful for auditing but not ideal for private transactions. While privacy-focused technologies like Zcash attempt to address this through advanced techniques like zero-knowledge cryptography to enable shielded transactions, they continue to face regulatory pressure and have yet to achieve widespread adoption.

Finally, although stablecoins enable global settlement, many rely on centralized issuers. Their stability depends on reserve quality, operational controls, and regulatory compliance. These factors sit outside the blockchain itself and reintroduce some of the counterparty risk that crypto originally sought to eliminate.

Will the Future of Global Payments be Completely Transparent?

As more value moves on-chain, visibility into global capital flows is increasing at an unprecedented pace. Blockchain transparency is creating a new paradigm where institutional, corporate, and retail fund movements can be monitored publicly.

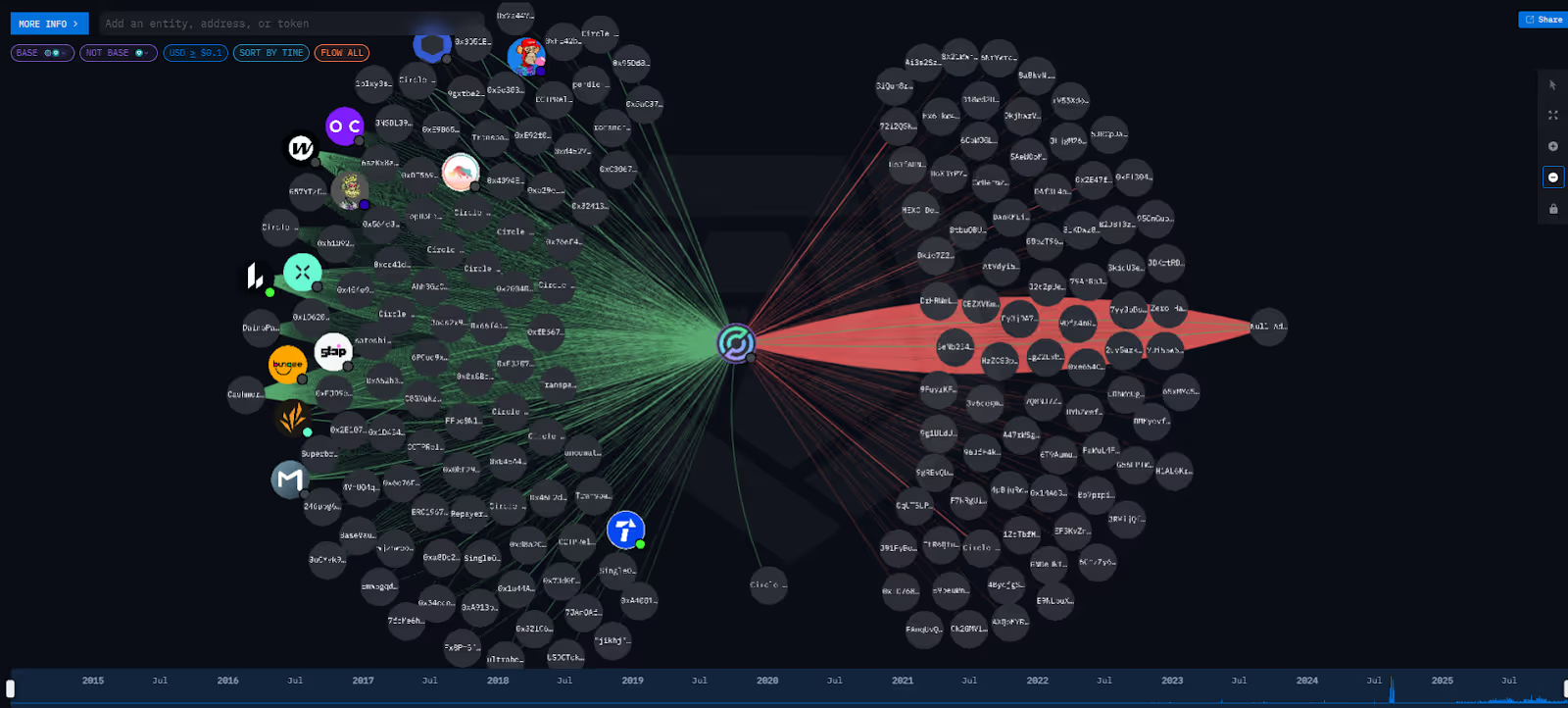

On-chain analytics platforms like Arkham Intelligence facilitate easy tracking of transactions and on-chain entities via its ecosystem of tools, enabling data to be turned into actionable insights.

- Entity Identification: Arkham maps blockchain addresses to known entities including exchanges, funds, market makers, and institutions, providing attribution that traditional banking systems cannot offer.

- Real-Time Alerts: Users can receive notifications when specific wallets or entities perform transactions, enabling monitoring of capital flows with minute-level granularity

- API Access: Developers and institutions can integrate Arkham’s data into trading systems, compliance tools, or risk engines.

Such platforms point to a future where money moving across multiple blockchains can be tracked, organized, and analyzed almost instantly, offering transparency that would be impossible in traditional financial systems.

Nevertheless, payments in the future probably won’t look the same everywhere. A mix of solutions will likely be adopted, from fully transparent blockchains to systems that protect privacy.

At one end of this spectrum are the fully transparent chains, such as Solana and Ethereum. These networks are poised to handle regulated payments, large institutional flows, and general consumer spending, all requiring a high degree of auditability.

Partially private solutions sit in the middle. These solutions leverage technologies like zero-knowledge proofs and selective disclosure. This allows for necessary compliance checks to be performed while simultaneously preserving core user privacy.

Finally, the far end of the spectrum is occupied by strong privacy-preserving chains, which are intended for specific, highly sensitive use cases. However, these technologies frequently attract heavy regulatory scrutiny, as seen in the crackdown on on-chain mixers like Tornado Cash.

Ultimately, global payments probably won’t ever be fully transparent, but more and more value is moving onto public, immutable ledgers, steadily increasing the overall transparency of the financial system.

Conclusion

Payment rails, the unseen infrastructure that moves money across the world, are facing a systemic transformation. Traditional systems such as SWIFT, ACH, and card networks remain critical, but their limitations in speed, cost, and transparency have opened the door for blockchain-based alternatives. Crypto payment rails, powered by stablecoins and high-efficiency blockchains, now process trillions annually and serve as real settlement infrastructure for fintechs and enterprises.

These rails offer lower costs, faster settlement, programmability, and unparalleled transparency. Yet they also raise new challenges related to privacy, regulation, and scalability. As platforms such as Arkham demonstrate, on-chain transparency is becoming a defining feature of the next generation of payments, a shift that will influence compliance, financial intelligence, and economic behaviour worldwide.

The future of payments is unlikely to be fully transparent or fully private. Instead, the landscape will consist of a mix of solutions tailored to different needs. However, what is clear is that more and more value is moving on-chain, and this shift is reshaping how money travels across the world.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)

.png)

.png)

.webp)