July 15, 2026

at

6:20 am

EST

MIN READ

Bitcoin’s Four Year Cycles: Why They Happen And Are They Dead?

Historically, many market observers describe multi-year ‘cycles’ in Bitcoin prices that coincide with Bitcoin’s scheduled halving events. These patterns, collectively referred to as a ‘four-year cycle’, have become significant psychological events which define the way crypto watchers think and trade. The descriptions below explain commonly-observed phases and theories, though individual cycles can differ.

In this article, we will go over the various phases that occur during a four year cycle and what happened during previous Bitcoin cycles. We will also ask the question: Are Bitcoin cycles still a thing?

A Typical Four-Year Cycle

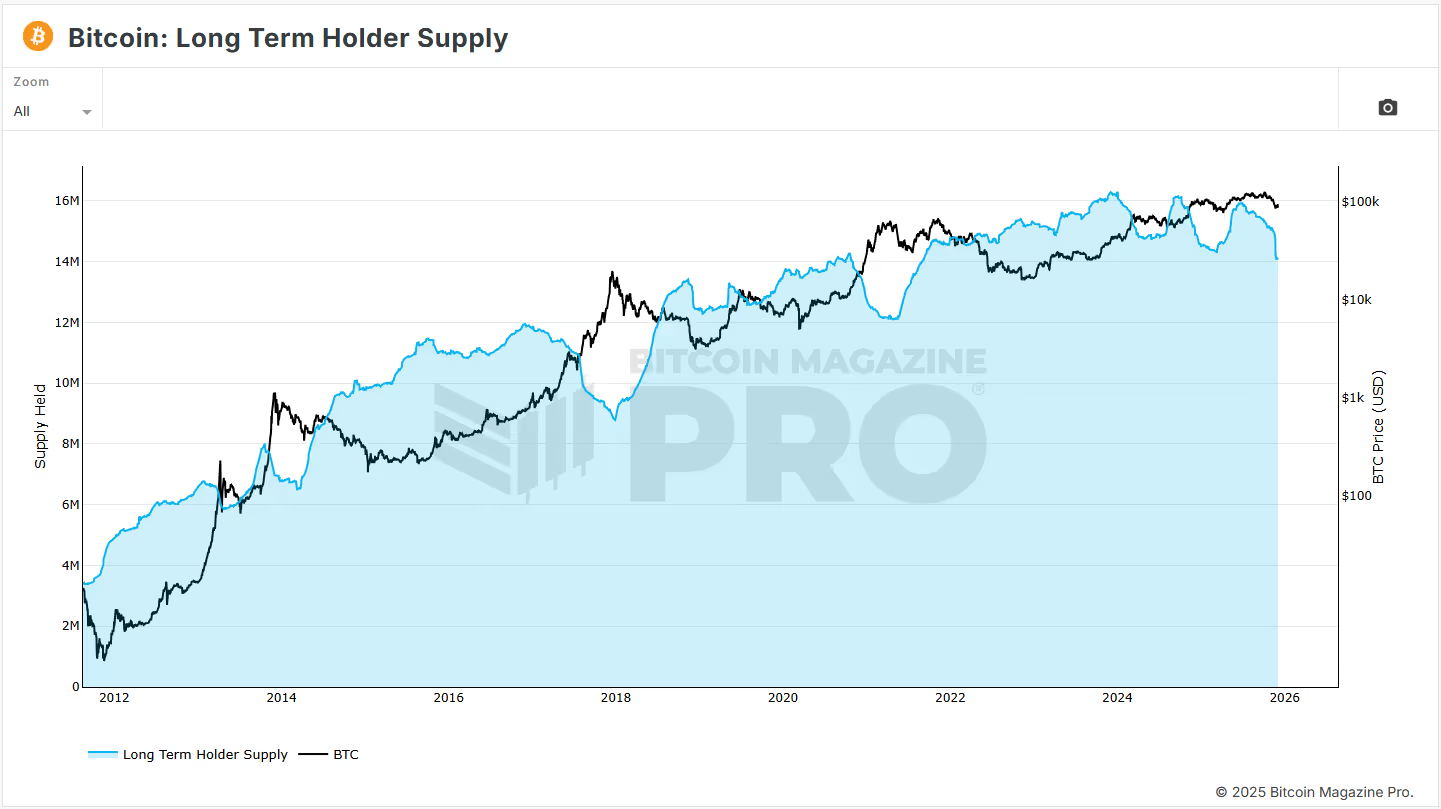

Market observers suggest that the standard Bitcoin cycle starts with what is commonly known as the ‘accumulation’ phase. They theorize that this phase begins after the crash following the previous cycle’s peak. During this time, price volatility and on-chain activity has been relatively low, and sentiment has tended to be either neutral or negative. It is called the accumulation phase because long-term Bitcoin holders start loading up on BTC that they perceive to be at a discount. As a result, price during this time period has been marked by gradual recovery.

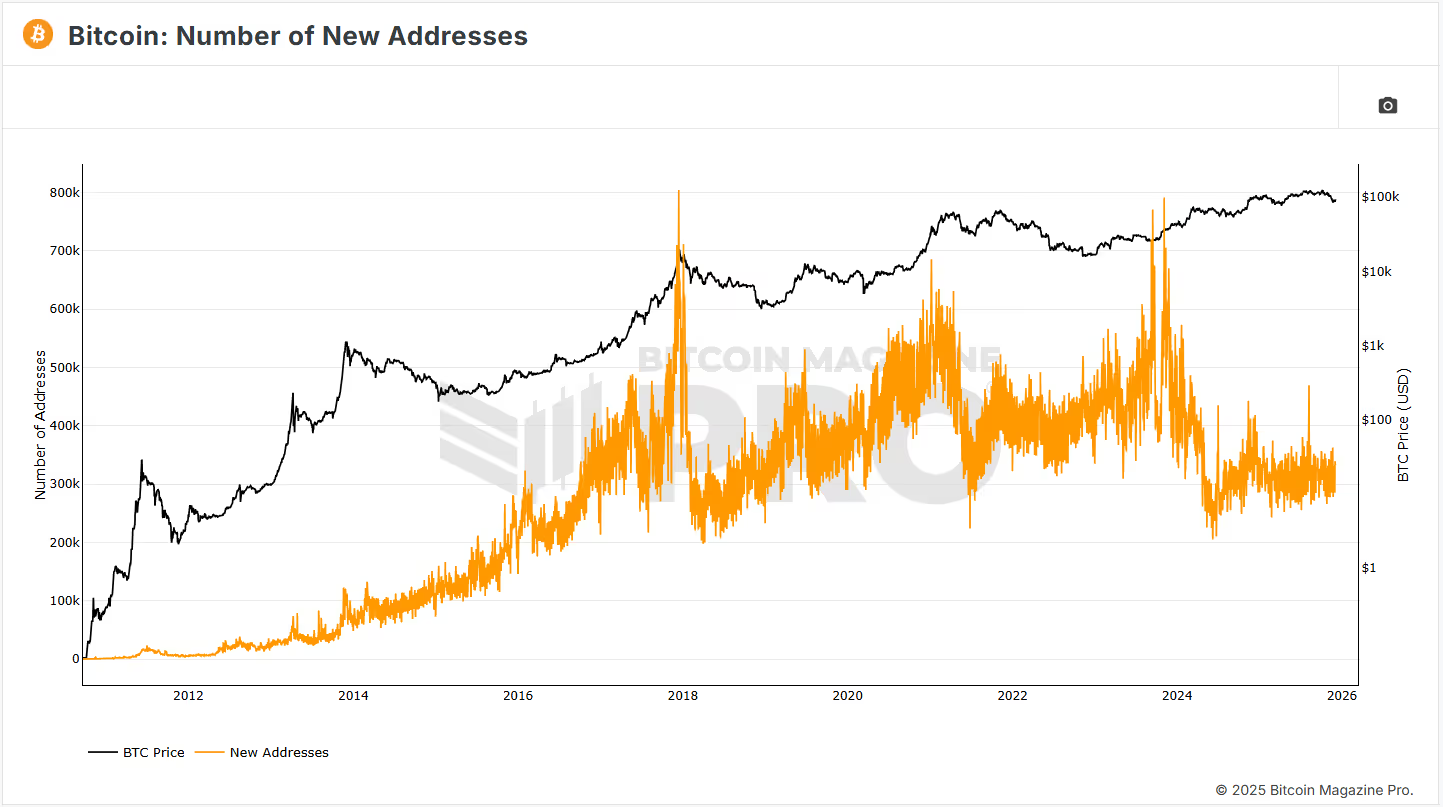

On-chain analytics reveal steady accumulation by certain investors, but the bulk of the retail crowd appears to be still wary from the previous big crash and remains uninterested in Bitcoin.

After the accumulation phase, which typically lasts 12 to 15 months, the cycle has historically transitioned into the start of a new bull market. This typically occurs prior to the halving, with the price of Bitcoin, and other crypto assets, beginning to climb in anticipation of the halving. The market begins to price in the effects of decreased future supply, and sentiment begins to change from neutral to optimistic. Liquidity starts returning to the market, and media attention picks up as well.

Once the halving occurs, the bull market has historically gone parabolic and prices start to ratchet upwards, sometimes slowly and sometimes explosively. The retail crowd has finally arrived and traders start throwing money into the market. Historically, at this point, new all-time highs are set as a massive new wave of investors begins throwing their money into the market. Some investors increase their leverage chasing the highs, and price action is more volatile.

Bull markets in the past have endured for roughly 12-18 months and typically ended with a sharp correction downwards in price. Leveraged traders have been flushed out, alt coins have seen even more drastic drops in price, and sentiment turns negative. The bear market typically starts at this point. During this phase of the cycle, many participants become forced sellers, dumping their holdings at a loss and escaping with what capital they can. Eventually, the dust settles and a market bottom slowly forms. Overall action and excitement has dropped significantly since the top, but determined builders continue on and development on new products and innovations marches quietly forward.

The Halving

In order to fully understand the four year Bitcoin cycle theory, it is important to have a solid grasp of what the halving is and how it impacts the price of Bitcoin.

Bitcoin’s halving is an important event that reduces the mining reward (paid in BTC) of adding a new block to the Bitcoin blockchain by half. This occurs every 210,000 blocks, which occurs roughly once every four years. In 2009, the reward for adding a new block to the Bitcoin blockchain was 50 Bitcoin per block. This has been halved four times since. The 2024 halving set the current new block mining reward to 3.125 Bitcoin. Assuming the four year pace holds, the halving will continue until Bitcoin reaches its cap of 21 million, which should occur somewhere around 2140.

The halving is Bitcoin creator Satoshi Nakamoto’s way of ensuring the scarcity of Bitcoin. One of the reasons Bitcoin was created during the 2008 financial crisis was as a response to central bank bailouts and inflationary fiat money printing. Most governments and their associated fiat currencies change their monetary policy constantly, making it difficult for holders to have long term faith in the value of their fiat money.

By way of the halving, Bitcoin mimics gold – one of humanity’s oldest stores of value – by becoming more scarce. Gold becomes harder to mine over time as mines are exhausted, and Bitcoin does this mathematically. As new supply of Bitcoin decreases, it becomes more scarce. Through supply and demand, the price of Bitcoin has historically coincided with upward price moves with each halving. Thus, the transparent and consistent nature of the Bitcoin halving, according to some proponents, makes Bitcoin an asset with strong store of value capabilities.

Recapping Previous Cycles

2013

The 2013 Bitcoin cycle was the very first cycle, Bitcoin having been invented in 2008. It was primarily driven by tech communities of the time such as internet forums and cryptography meetups. This cycle also garnered some early media attention revolving around events such as the first real-world purchase using Bitcoin (two pizzas for 10,000 Bitcoin) and narratives such as “Is Bitcoin digital gold?”.

During this cycle, Mt. Gox was the largest Bitcoin exchange. Mt. Gox was processing over 70% of all Bitcoin transactions worldwide by 2014. However, in 2014 Mt. Gox suspended trading and closed its website after it was revealed that 850,000 Bitcoin went missing. (An investigation in 2015 revealed that starting in 2011, most of the missing Bitcoin had been stolen straight out of the Mt. Gox Bitcoin wallet.) Because Mt. Gox was the majority of Bitcoin liquidity, this failure led to a major loss of trust in Bitcoin and price fell by 85%, starting the bear market.

2017

The 2017 cycle is when Bitcoin went mainstream among retail investors. With Ethereum’s launch in 2015, smart contracts and their revolutionary potential entered the public consciousness. Ethereum saw its price explode from $10 to $1400 during this cycle. This time is remembered also for the ICO mania, where thousands of ERC-20 tokens were launched and investors threw money at any token that had a whitepaper. Bitcoin also saw an explosion in price from the massive influx of new investors, surging from $200 to $20,000 in 2.5 years. The industry was regularly being reported on by mainstream media (see image above).

Eventually, the ICO mania that fueled much of the run up ended up being a major catalyst for the crash. In an ICO, investors swapped their Ethereum or Bitcoin for a new project’s cryptocurrency. Flush with ETH, many projects started dumping their holdings for cash, putting downward pressure on the price. The SEC also began cracking down on ICOs by labeling them as unregistered security offerings and prosecuting a large number of projects, many of which were Ponzi schemes and scams. In this climate, over-leveraged investors either panic sold or were forced to sell as prices began to collapse, and Bitcoin saw a nasty 84% drop to $3,200.

2021

The 2021 Bitcoin cycle came alongside Covid-era money printing. Governments around the world looked to kick start the economies that the pandemic had brought to a halt, and fiscal stimulus was their solution. This explosion in global liquidity helped fuel Bitcoin’s run to then-all time highs in 2021. This cycle was also characterized by a shift from Bitcoin being a form of “internet money” and towards being a more serious “macro asset”. Companies like Strategy (formerly MicroStrategy) and Tesla bought billions of dollars worth of Bitcoin, and payment apps such as PayPal and CashApp began to support buying and selling Bitcoin. 2020’s DeFi summer and 2021’s NFT craze helped draw in massive retail participation during this cycle. Retail investors and institutions both bid crypto prices up, and Bitcoin hit $69,000 at the top.

The end of this Bitcoin cycle was caused by the collapse of several high profile protocols and companies within the space. First, the Luna stablecoin UST depeg wiped out $60B in a very short period of time. Companies and firms such as Voyager, Celsius, BlockFi, and Three Arrows Capital had varying levels of direct and indirect exposure to Luna, directional bets on the market, and exposure to each other, and consequently went bankrupt as a result. BlockFi in turn underwent restructuring and secured a line of credit from FTX. It finally went bankrupt when FTX unravelled.

Popular cryptocurrency exchange FTX and associated trading desk Alameda were found to be committing massive levels of fraud, and were forced to liquidate assets to try and repay users. The U.S. federal government also ended their stimulating monetary policy and began aggressively raising interest rates, sucking liquidity out of the market. All of these events played a part in a vicious drop in Bitcoin’s price, down to $15.5k during the bear market bottom.

2025

The 2025 cycle saw increased institutional adoption, with major traditional finance players making moves in the space. Spot Bitcoin ETFs were approved in January 2024, and companies such as BlackRock, Fidelity, and VanEck began offering Bitcoin as a standard investment product. Many companies also adopted Strategy’s Digital Asset Treasury (DAT) model, acquiring cryptocurrency to add to their balance sheet. The cycle was unique because Bitcoin hit a new all time high of $73k before the halving had occurred in April 2024. Additionally, institutions were the primary driver of price discovery, and retail participation did not reach the levels that previous cycles had seen.

Why Do Cycles Occur?

Stock-to-flow

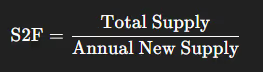

There are multiple potential reasons as to why Bitcoin four year cycles occur. One common explanation revolves around S2F (Stock to Flow), a model that is typically used to measure the scarcity of commodities such as gold and silver.

This model compares Stock (existing supply) to Flow (annual new supply). The higher the ratio, the more scarce a commodity is. We can easily apply S2F to Bitcoin, since Bitcoin has both a fixed total supply and mining rewards that are on a fixed schedule. With each halving, Bitcoin’s S2F ratio doubles since new supply is cut in half. Currently, Bitcoin has a S2F of ~110, whereas gold has a S2F in the 60s, making Bitcoin the significantly more scarce asset under the S2F model.

Psychological

Another simple explanation revolves around psychology and self-fulfilling prophecies. Bitcoin’s price is strongly influenced by narratives, herd behavior, and expectations about the future. Because Bitcoin does not have some sort of intrinsic value like earnings that a more traditional financial asset would have, Bitcoin’s value is based primarily on what people think it will be worth in the future. As a result, the price of Bitcoin is quite reflexive and more sensitive to things such as halving anticipation, rumors, and narratives. Because the four year Bitcoin cycle has played out for multiple cycles in a row, investors are more likely to trade the asset according to how previous cycles played out, creating a self-fulfilling prophecy.

Liquidity

Others argue that Bitcoin’s cycle is based primarily off of global liquidity. In his Substack article “Long Live The King”, BitMEX founder Arthur Hayes argues that Bitcoin’s four year cycles are directly tied to global liquidity, highlighting the impact of both the US Dollar and China’s Yuan. Hayes explains that the 2013 peak was caused by post 2008 financial crisis money printing, the 2017 peak was caused by a devaluation of yen against the dollar, and the 2021 peak was caused by post COVID money printing.

More recently, narratives around the end of Quantitative Tightening (QT) – where the Fed reduces the number of assets on its balance sheet, therefore reducing liquidity –, the resumption of Quantitative Easing, and falling interest rates have led to some commentators claiming the 2025 BTC cycle will not stick to the same patterns as in previous years.

Retails vs Institutions

Retail and institutional ownership dynamics also play a significant role in driving Bitcoin’s cycles. Institutional investors are typically more disciplined and have a longer time horizon, leading to these investors buying during fear and putting in market bottoms. Retail investors on the other hand, tend to be more emotional and are more likely to buy based on fear of missing out. As a result, retail investors are more likely to chase price momentum and use leverage. Retail investors tend to create more volatility during a cycle, especially towards the later stages.

Why Are People Saying The Cycles Are Over?

There are several reasons why people might claim that Bitcoin cycles are a thing of the past. One big reason is the increase in institutional participation in Bitcoin through things like ETFs, corporate treasuries, hedge funds, etc. These financial entities behave differently from retail by buying on fixed schedules, using reasonable amounts of leverage, and diligently managing risk. This type of behavior dampens volatility and therefore dampens cycles.

Another potential reason is that cryptocurrency has grown significantly from early cycles. Bitcoin is increasingly tied to macroeconomic factors such as interest rates and Federal Reserve policy, which lessens the effect that halvings have on Bitcoin’s price. Whereas the halving occurs every four years, Federal Reserve policy is not on a similar fixed schedule. The halving itself is also becoming less important due to the diminishing impact it has on block rewards. Whereas the first halving reduced the reward from 50 BTC to 25 BTC, the last halving had a much smaller impact going from 6.25 BTC to 3.125 BTC.

How Will We Know That Cycles Are Over?

Paying attention to how the current cycle plays out will give us a much better idea on whether four year cycles are a thing of the past or not. Let’s go over some of the key signs that might indicate this.

- Previous cycles have seen a blow-off top post halving, typically 12-18 months after.

- Previous cycles have ended with massive leverage wipeouts and cascading liquidations, causing drawdowns of over 70%.

- If the price of Bitcoin begins to track perfectly to changes in global liquidity, then Bitcoin has become a macro asset, not a halving-based cycle asset.

- Previous cycles have seen an explosion in retail participation in later stages of the cycle, causing altcoins to go parabolic. A lack of retail participation means that a cycle has been dominated by institutional buying, which could lead to less volatility and flatten the cycle.

Conclusion

Bitcoin has had a long and consistent history of four-year cycles. We’ve seen Bitcoin slowly rise out of the bear market into the halving, consistently explode in price afterwards, and then fall rapidly as leveraged traders are wiped out. Many factors have historically contributed to this, all combining to create the four-year cycle that we’ve come to grow familiar with. That said, Bitcoin has slowly but surely matured into the $1.8T behemoth it is today. The arrival of institutions, ETFs, and sovereign wealth means that the participants of this market have changed considerably since the first cycle. Bitcoin appears to grow increasingly sensitive to macroeconomic factors, yet is still governed partially by familiar forces such as psychology and mining economics. It is unclear whether Bitcoin’s cycles are completely over, but each cycle is unique and it is entirely possible that future cycles will look nothing like what came before them. Understanding the evolution of this asset and its participants over time is key to understanding what future cycles might look like, but in the end, only time will tell if the usual patterns are here to stay or a relic of the past.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)