September 30, 2025

at

10:05 am

EST

MIN READ

What Andrew Kang had to say about Tom Lee’s ETH thesis

Andrew Kang, founder of crypto venture firm Mechanism Capital and one of the most famous traders in the industry, posted an article on X last week which strongly criticised Tom Lee’s recent ETH thesis.

He called it “one of the most r*tarded combinations of financially illiterate arguments I’ve seen from a well known analyst in a while.”

Tom Lee has recently become a household name in the crypto world, with some people calling him Ethereum’s Michael Saylor, after he masterminded BitMine’s transition from Bitcoin miner to the world’s biggest Ethereum treasury company.

Anyone who follows Tom Lee on Twitter will know that he is extremely bullish on ETH and frequently posts about its strengths and why he thinks it is such a good asset to invest in.

Kang breaks down Lee’s ETH thesis into five key components:

(1) Stablecoin & RWA Adoption

(2) Digital oil comparison

(3) Institutions will buy and stake ETH to contribute to the security of the network in which they are tokenizing their assets & as operating capital

(4) ETH will be equal to the value of all financial infrastructure companies

(5) Technical Analysis

Kang then applies his great analytical abilities to explain why he thinks Tom Lee is so wrong before ending by saying that unless there is organisational change at Ethereum, the token is destined for ‘indefinite underperformance’.

Here’s the breakdown of Kang’s article.

1. Stablecoin & RWA Adoption

Tom Lee’s main ETH argument, as Kang sees it, is that as more real-world assets (RWAs) and stablecoins are used on Ethereum, revenue from fees will increase, which will drive up ETH's value.

Kang refutes this with data showing that despite a 100x-1000x increase in tokenized asset value since 2020, daily ETH fees have remained the same.

Kang states that Ethereum upgrades have made transactions cheaper, lots of new activity is happening on Solana and Arbitrum, and, importantly, the increase in tokenized asset value does not necessarily correlate to higher fees.

The key, for Kang, is high velocity assets that generate lots of fees, not high value assets that don’t get traded frequently.

Kang goes on to claim that high velocity assets are not transacting on Ethereum as much as Tom Lee believes. Solana, Arbitrum and Tempo are making big wins, at Ethereum’s expense. Kang comes across as quite bearish on Ethereum in this section of his article.

2. Digital Oil Comparison

Kang addresses Lee’s claim that Ethereum is "digital oil" due to how essential it is to the crypto ecosystem. While he agrees that ETH can be viewed as a commodity, like oil, he argues this is not a bullish case for its price. Real oil prices, when adjusted for inflation, have traded within the same general range for over a century. They have occasional spikes which always revert back to normal.

Lee’s point then is more about how essential ETH is to crypto, and less about how much the price of ETH will increase in the future.

3. Institutions Will Buy and Stake ETH

The third point of Lee's thesis insists that large financial institutions will purchase and stake ETH to secure the network and use it as operating capital for their tokenized assets.

Kang simply states that this is not happening. No large banks have bought ETH for their balance sheets, and none have announced any plans to do so, says Kang.

Whilst this does not exactly refute Lee's thesis about the bullishness of ETH, it does show that it is based more on belief than any serious data.

4. ETH Will Equal All Financial Infrastructure Companies

Kang’s rebuttal of Lee’s ETH thesis here is very short. He states simply:

“I mean, come on. Again, a fundamental misunderstanding of value accrual and just pure delusion.”

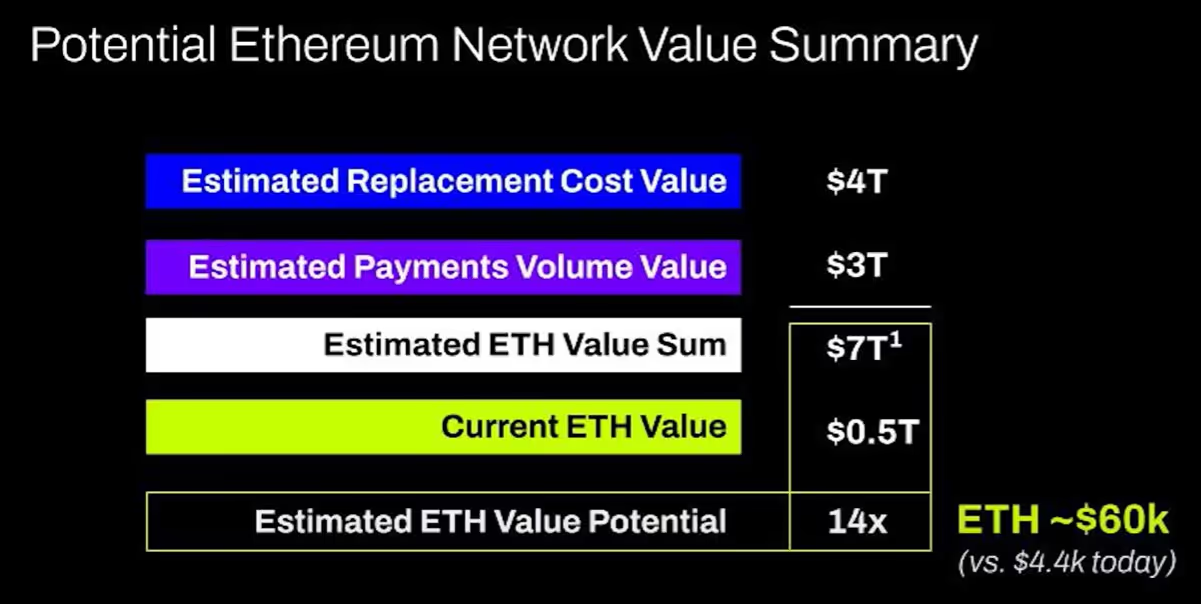

But, what does Tom Lee actually mean here? Lee has consistently stated his belief that Ethereum will be the rails upon which the new financial system will operate. The financial institutions of today will be building everything on Ethereum in the future and the Ethereum ecosystem will become the settlement layer for every financial transaction.

Kang specifically attacks Lee’s claim that ETH will equal all financial infrastructure companies but he provides no evidence for what Lee actually said to this effect, except for an image that looks like it was produced by BitMine. The image claims ETH’s market cap will be $7 trillion in the future, with the ETH price at $60k.

Kang doesn’t state what value he thinks financial infrastructure companies will have in the future, or even what value they have today, but from later comments in the article, Kang is definitely sceptical of ETH’s price reaching $60k anytime soon.

5. Technical Analysis

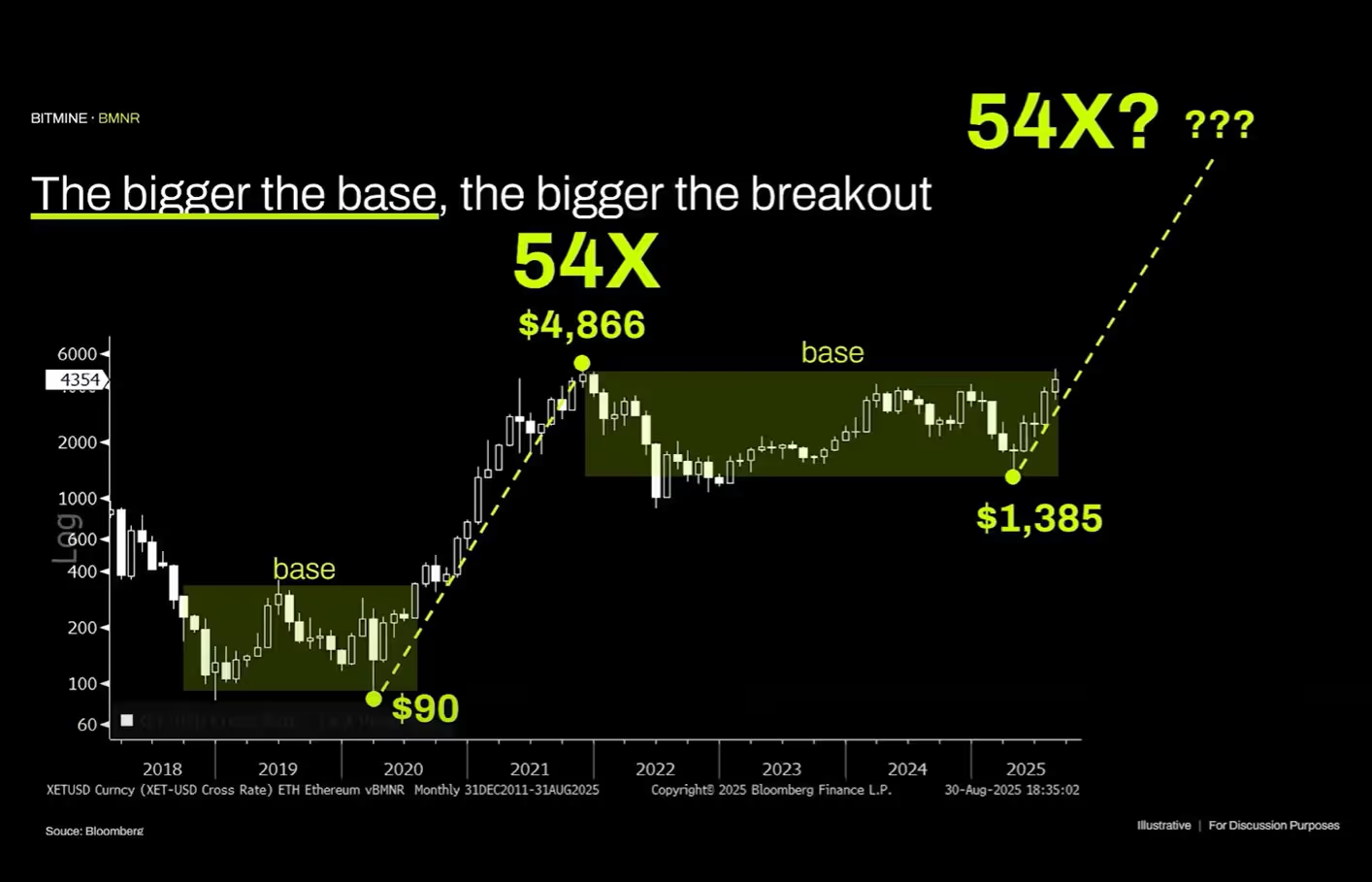

Finally, Andrew Kang criticises Lee’s use of technical analysis, claiming the BitMine Chair has been drawing ‘random lines to support his bias’.

Kang uses BitMine’s own charts to show that the technical analysis objectively shows Ethereum stuck in a multi-year range which recently reached its top. He says that in the future, ETH will likely operate within a $1,000-$4,800 band.

He further argues that ETH's high valuation is not supported by its fundamentals but by "financial illiteracy" among investors, much like the token XRP. He believes that while broad market liquidity has kept ETH's price afloat, it is destined for "indefinite underperformance" unless there are major changes to its core value proposition.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)

.png)

.png)