October 12, 2024

at

12:00 am

EST

MIN READ

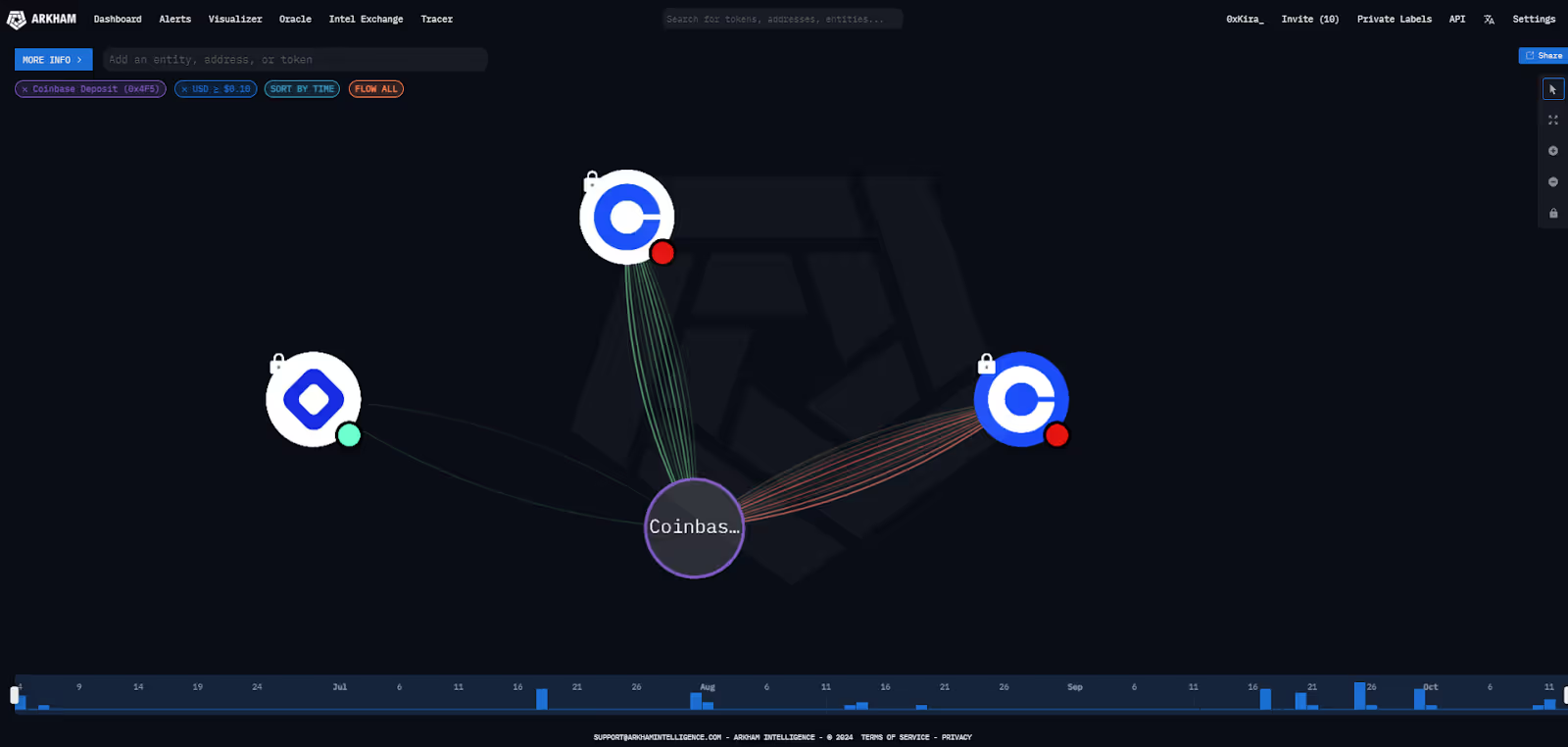

BlockFi Sends $190M USDC to Coinbase

A BlockFi-funded Coinbase deposit address (0x4F5) has just transferred 189.84M USDC to a Coinbase hot wallet, fuelling speculations that the long awaited repayment of customer funds from the BlockFi bankruptcy are finally commencing. The Coinbase deposit address was initially funded by a BlockFi hot wallet in June 2024.

The movement of stablecoins into a major exchange's hot wallet is a significant step. Hot wallets are operationally used for processing and sending transactions, which directly aligns with the expected need to distribute funds to many different customer accounts as part of a repayment plan.

The transferred USDC amount likely originated from a BlockFi wallet (0xf15) which had transferred 184.96M USDC to a Coinbase Prime Deposit Address (0x37B) the day before, which were then transferred into a Coinbase Prime hot wallet (0xCD5).

This on-chain path, from the initial wallet to an institutional platform like Coinbase Prime, illustrates the structured process of managing the assets. It shows a clear custodial chain before the funds are prepared for potential final distribution.

These fund movements come after BlockFi had managed to secure a sale of their FTX claims at a “substantial premium to their face value” back in July 2024. This allowed the crypto lending firm to proceed with the bankruptcy proceedings, winning approval from the courts to fully repay eligible customers and general unsecured creditors claims after almost 2 years since the collapse of centralized exchange, FTX.

For creditors awaiting resolution, these large-scale transfers are the most tangible sign of progress. The successful asset liquidation (the FTX claims sale) is now being followed by the necessary on-chain logistics to finally make those creditors whole.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)