April 22, 2026

at

12:30 pm

EST

MIN READ

A Guide to Crypto Compliance: KYC, AML, Travel Rule and More

Crypto was built on the promise of permissionless finance: no gatekeepers, no intermediaries, no paperwork. As crypto’s adoption grew, that original vision ran headlong into the reality of the traditional financial system. With no accountability, crypto quickly became a target for money laundering, sanctions evasion, and terror financing. More than 15 years since Bitcoin was launched, the regulatory stance towards crypto is finally firming up.

The Financial Action Task Force’s (FATF) June 2025 update found that Travel Rule frameworks have been adopted or are in progress across 99 jurisdictions. With estimates of approximately $51B in on-chain activity linked to illicit actors in 2024, it is no surprise why regulators are pushing hard for compliance across the industry.

For exchanges, custodians, DeFi protocols, and any business involved in crypto, understanding these obligations is no longer optional. This guide breaks down the key terms, explains why compliance matters, and covers what happens when companies ignore the rules.

Summary

- Crypto compliance covers a set of regulatory obligations, including KYC, AML, and the Travel Rule, that govern how crypto businesses verify users and report suspicious activity.

- Global bodies like the FATF set compliance standards for virtual asset service providers, with regional frameworks like MiCA translating these into enforceable law.

- Failure to meet crypto compliance requirements has cost exchanges billions in fines and resulted in criminal charges for senior executives at major platforms.

- Blockchain intelligence tools like Arkham allow compliance teams to trace on-chain activity, identify illicit fund flows, and monitor wallets in real time.

What is Crypto Compliance?

Crypto compliance refers to the set of legal and regulatory obligations that cryptocurrency businesses must follow to prevent their services from being used for financial crime. These obligations mirror those applied to traditional financial institutions, covering identity verification, transaction monitoring, record keeping, and reporting, but are adapted for the unique properties of blockchain-based assets.

The challenge for crypto businesses is that these obligations vary by jurisdiction and are still evolving. A compliant exchange in Singapore may face different requirements than one operating in the EU or the U.S., and many of these platforms operate globally.

Glossary of Crypto Compliance

KYC (Know Your Customer) refers to the process by which a business verifies the identity of its customers before allowing them to use its services. In practice, this means collecting documents like passports or government-issued IDs and running them against databases to confirm a user is who they claim to be. An exchange asking a new user to upload a photo ID and proof of address before enabling withdrawals is performing KYC.

AML (Anti-Money Laundering) refers to the policies and controls a business puts in place to detect and prevent money laundering through its platform. AML programs go beyond onboarding: they cover ongoing transaction monitoring, staff training, and internal controls. A crypto exchange flagging a customer who deposits funds from a known darknet market address is acting on its AML obligations.

CFT (Combating the Financing of Terrorism) sits alongside AML as a core regulatory requirement. Where AML focuses on dirty money from criminal proceeds, CFT focuses specifically on funds destined to finance terrorist activity. A Virtual Asset Service Provider (VASP) screening a wallet address against a designated terrorist organization list is performing CFT checks. In most regulatory frameworks, AML and CFT obligations are grouped together as AML/CFT.

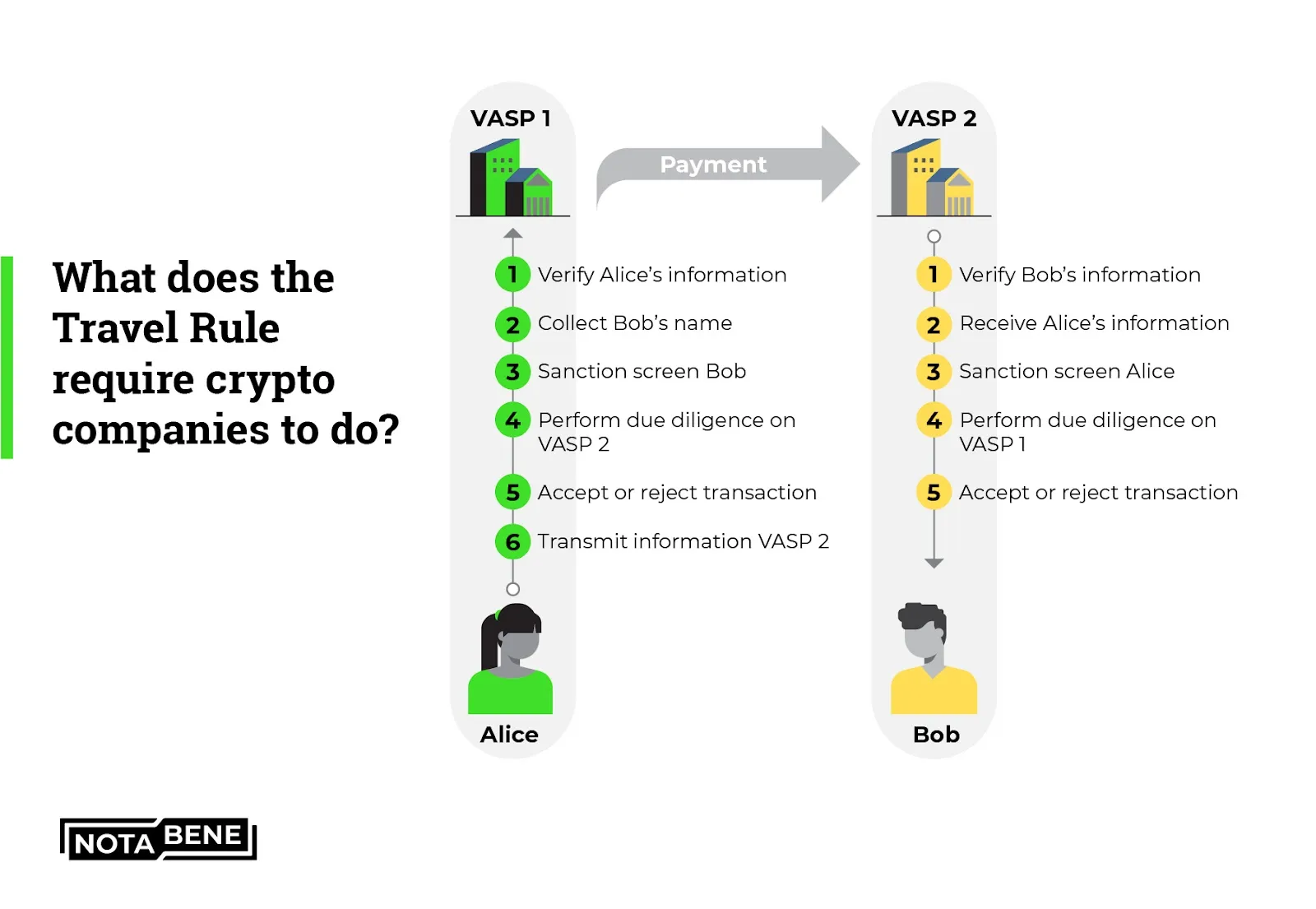

Travel Rule is the requirement that VASPs pass identifying information about transaction originators and beneficiaries when transferring crypto between platforms. Under the Travel Rule framework, VASPs must collect and verify information about the originator and beneficiary of a transaction, and share it with counterparties. This information must travel with the transfer to increase transparency and traceability. If a user sends Bitcoin from one exchange to another, both platforms are required to share that customer's details with each other, similar to the wire transfer rules that have long applied to banks.

SAR (Suspicious Activity Report) is a formal report filed by a financial institution or VASP with a financial intelligence unit when it detects activity that appears suspicious or potentially linked to financial crime. Filing a SAR does not mean a crime has occurred; it means the institution has flagged it for review by authorities. Between 2014 and 2020, BitMEX failed to file a Suspicious Activity Report on at least 588 specific suspicious transactions, a failure that resulted in a $100M enforcement action against the exchange in 2021.

VASP (Virtual Asset Service Provider) is the term used by the FATF to describe any business that exchanges, transfers, safeguards, or administers virtual assets on behalf of customers. Crypto exchanges, custodians, and certain wallet providers all qualify as VASPs. The crypto Travel Rule is a regulatory obligation for VASPs, not their users. This designation matters because it determines which AML/CFT obligations apply.

Transaction monitoring is the ongoing process of analyzing customer transactions to detect patterns or behaviors associated with financial crime. A compliance system that flags a customer for sending funds in rapid succession to multiple new addresses, or for receiving funds from a mixer, is performing transaction monitoring. It operates continuously, not just during the onboarding process.

Sanctions screening is the process of checking customers and transaction counterparties against government-published lists of sanctioned individuals, entities, and jurisdictions. In crypto, this includes screening wallet addresses against lists published by bodies like the U.S. Office of Foreign Assets Control (OFAC). An exchange blocking a withdrawal to a wallet address linked to a sanctioned North Korean entity is fulfilling its sanctions screening obligations.

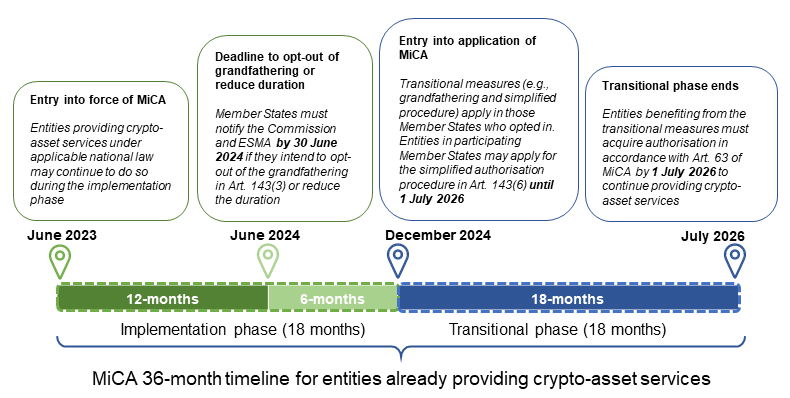

MiCA (Markets in Crypto-Assets Regulation) is the European Union's comprehensive regulatory framework for crypto assets and the businesses that service them. MiCA's main objective is to create clear and consistent rules for Europe's crypto market, increasing transparency, supporting fair growth, and protecting consumers from fraud and market manipulation. Full enforcement began on 30 December 2024, although Crypto-Asset Service Providers have a transitional period of 12 to 18 months, depending on their location, to achieve full compliance. MiCA is the most significant regional crypto regulatory development globally, and non-EU platforms serving European customers are also included in its scope.

FATF (Financial Action Task Force) is the international standard-setting body for anti-money laundering and counter-terrorism financing. Its recommendations serve as the baseline that most jurisdictions translate into national law. Countries that fail to implement FATF standards risk being placed on the FATF's grey or black lists, which carries severe consequences for their access to the global financial system.

Proof of Reserves refers to a mechanism by which a crypto exchange or custodian publicly demonstrates that it holds sufficient assets to cover all customer liabilities. Following the collapse of FTX in 2022, demand for exchange transparency surged. A proof of reserves audit typically uses cryptographic techniques, such as Merkle trees, to allow users to verify that their individual balances are included in the total without revealing private account details.

Chain of custody in the crypto context refers to the documented trail of an asset's movement across wallets and platforms. When a compliance team traces funds from an initial illicit source through a series of intermediate wallets to a final destination, establishing that chain of custody is what gives the evidence evidentiary value. It is the crypto equivalent of documenting the handling of physical evidence in a criminal investigation.

Why Crypto Compliance Matters

On a company level, non-compliance can break a company. But on the broader systemic level, compliance underpins whether crypto can function as a legitimate part of the global financial system.

Regulators have made their priorities clear. Enforcement actions in 2025 saw crypto exchanges bear $927.5M in AML/CFT penalties, with BitMEX, KuCoin, and OKX facing fines for inadequate compliance programs. These are signals that regulators across multiple jurisdictions are actively pursuing platforms that are in violation of compliance regulations.

The operational case for compliance extends beyond avoiding fines. Institutional capital, which has been flowing into crypto in increasing volumes, requires counterparties with robust compliance programs. Without them, banks won't provide services, institutional investors won't trade, and payment networks won't integrate. Compliance is increasingly a prerequisite for accessing the traditional financial infrastructure that crypto businesses require to scale.

For users, compliance provides some protections too. KYC requirements make it harder for stolen funds to be liquidated quietly. Sanctions screening prevents platforms from becoming conduits for state-sponsored theft or terror financing.

How to Implement Crypto Compliance

A functional crypto compliance program consists of several interconnected components.

The foundation is a risk-based approach. Not every customer or transaction carries the same risk, and a proportionate compliance program reflects that. A high-volume trader with a history of counterparty diversity warrants more scrutiny than a retail user making occasional small purchases. FATF's framework explicitly endorses risk-based approaches, allowing VASPs to allocate compliance resources where the risk is highest.

Identity verification at onboarding is the first concrete step. This means collecting identity documents, verifying them against authoritative sources, and screening new customers against sanctions lists and politically exposed person (PEP) databases. Enhanced due diligence applies to higher-risk customers, involving deeper background checks and source of funds verification.

Transaction monitoring must be ongoing. Compliance teams need systems that flag unusual patterns in real time, including structuring transactions to stay below reporting thresholds, rapid movement of funds across multiple wallets, or transactions involving addresses linked to known illicit activity. Alert thresholds need to be calibrated carefully: too sensitive and the team drowns in false positives, too loose and real risks go undetected.

Travel Rule compliance requires technical infrastructure for sharing originator and beneficiary information with counterparty VASPs. This may involve upgrading AML controls, integrating secure messaging solutions, and enhancing transaction monitoring. Several purpose-built Travel Rule protocols already exist to handle this data exchange between platforms.

Finally, compliance requires documentation. SARs must be filed where required, records must be retained according to jurisdictional requirements, and internal policies must be written, reviewed, and enforced. Regulators look closely at whether a compliance program exists on paper only or whether it operates in practice.

What Happens When Companies Fail to Comply

The consequences of non-compliance range from financial penalties to criminal prosecution, and in the most serious cases, to the complete destruction of the business.

Binance is a defining recent example. Binance pleaded guilty in the United States and paid over $4B to resolve its criminal liability, including billions in both criminal penalties and forfeiture of proceeds of its illicit activities. The DOJ found that Binance's own internal communications showed its compliance employees recognized that Binance did not have the necessary protocols to flag or report transactions for money laundering risks. Then Binance CEO Changpeng Zhao pleaded guilty and was ultimately sentenced to four months in prison and ordered to pay a $50M criminal fine, and was forced to resign as CEO.

BitMEX followed a similar path. Executives failed to institute AML or KYC programs at BitMEX despite closely following US regulatory developments that made clear their legal obligation to do so. BitMEX was fined $100M in connection with a previously entered guilty plea to criminal violations of US anti-money laundering laws, on top of earlier civil penalties, bringing total costs past $200M.

In both cases, their leadership was aware of compliance obligations, made deliberate decisions to deprioritize them, and eventually faced consequences that far exceeded whatever cost compliance would have required. As of November 2025, more than 50 crypto firms had their licenses revoked under MiCA, primarily due to failure to meet AML/KYC rules or reserve requirements.

The Role of Blockchain Intelligence in Compliance

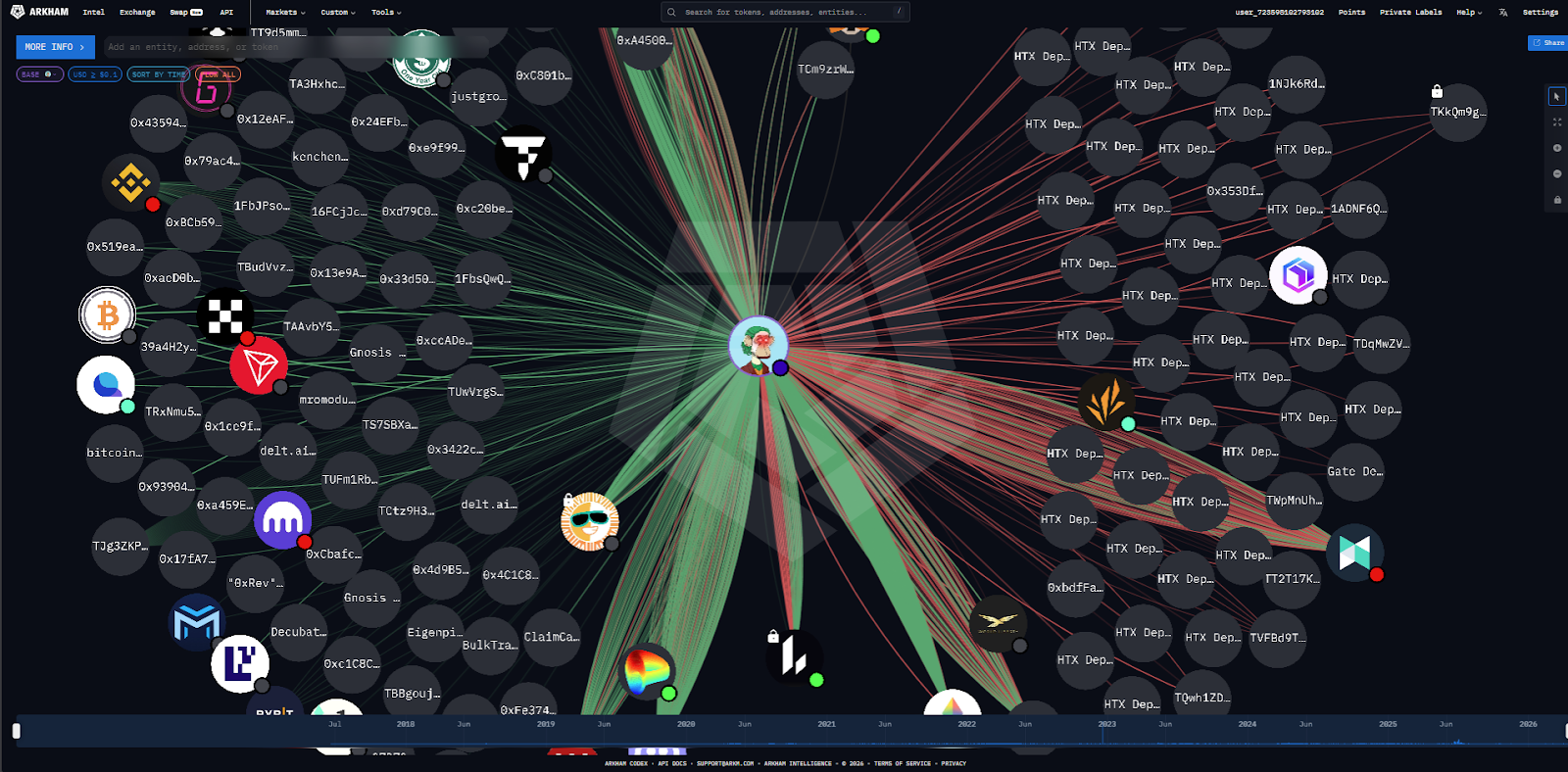

The public nature of blockchain ledgers creates a compliance resource that has no equivalent in traditional finance. Every transaction is recorded permanently and is auditable by anyone with the right tools. For compliance teams, this is a huge aid.

Blockchain analytics platforms like Arkham provide tools for linking cryptocurrency activity to real-world entities, deanonymizing blockchain transactions, and transforming raw on-chain data into actionable intelligence for compliance, research, and investigative purposes. Compliance teams at exchanges use these platforms to screen incoming transactions against known illicit sources before funds are accepted, and to investigate alerts generated by transaction monitoring systems.

Arkham's API provides access to Ultra, its crypto address-matching engine, which links blockchain addresses to real-world entities, giving users the ability to customize data flows, monitor transactions, and integrate them into their own systems.

The combination of on-chain data and entity labeling closes a gap that pure KYC cannot. A customer may pass identity verification at onboarding and later receive funds from a compromised source. Transaction monitoring and blockchain intelligence working together can catch that in near real time. Compliance teams at cryptocurrency exchanges rely on Arkham to identify potentially suspicious activities and maintain regulatory compliance.

Conclusion

Crypto compliance has moved from an abstract regulatory concern to a central operational requirement. The frameworks are in place, the enforcement is live, and the penalties for non-compliance have been established in cases large enough that no serious platform can feign ignorance.

As jurisdictions adopt FATF standards and regional frameworks like MiCA reach full enforcement, the scope of crypto compliance only continues to grow. Proof of reserves and chain of custody are becoming table stakes for platforms that want to be taken seriously by institutional counterparties.

The good news is that the tools exist to do this well. Blockchain's transparency, combined with analytics platforms that can surface the connections between addresses and real-world entities, gives compliance teams visibility that would have been impossible in traditional finance. The question is whether platforms choose to use it.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)