May 25, 2026

at

5:35 am

EST

MIN READ

Is BTC Still a Risk Asset? Safe Havens, Institutional Adoption and Sovereign Risk

Few assets in modern markets attract as many polarizing views as Bitcoin. Depending on who you ask, it is a speculative bubble, revolutionary monetary technology, or something in between. The question of how to classify Bitcoin has become increasingly consequential as it becomes more and more institutionalised and is included in the portfolios of sovereign wealth funds, corporate treasuries, and regulated investment products.

This classification matters because it shapes investor behaviour. It determines where it sits in a portfolio, how much of it institutions are permitted to hold, and how investors respond when markets move against them. An asset treated as a speculative bet gets sold in a crisis, while an asset treated as a safe haven gets bought.

For most of its existence, Bitcoin has been firmly in the first camp. Its volatility, its sensitivity to monetary conditions, and its tendency to sell off alongside equities in periods of stress have made the risk asset label difficult to escape. But the market structure around Bitcoin has changed substantially, and with it, the argument that Bitcoin is something more than a high-beta trade has become harder to dismiss.

Summary

- Risk assets are investments whose value is sensitive to changing economic conditions, with Bitcoin as one of its most volatile examples.

- Gold has long served as the benchmark safe haven, and Bitcoin's correlation with equities versus gold reveals a divergence in how markets treat the two assets.

- Institutional adoption through spot ETFs and corporate treasury allocations has structurally changed who owns Bitcoin and why, subsequently how the market prices it.

- Governments acquiring Bitcoin as a strategic reserve asset, combined with Bitcoin's censorship-resistant properties, could cement its role as a sovereign risk hedge

What is a Risk Asset?

A risk asset is any asset with high price volatility and potential for strong returns. These assets tend to be particularly sensitive to the underlying health of the economy and to shifts in investor sentiment. When confidence is high and credit is cheap, investors migrate toward risk assets in search of returns. When fear takes hold, they flee to safety. In practice, the category includes equities, high-yield corporate bonds, commodities tied to industrial demand such as copper and oil, real estate, and cryptocurrencies.

The risks that govern these assets fall into a few broad categories. Financial risk relates to leverage, liquidity, and exposure to credit markets. Operational risk covers disruption to the underlying business or network. Strategic risk concerns the long-term competitive position of an asset or the sector it belongs to. Compliance risk has grown in relevance for crypto specifically, as regulatory clarity across major jurisdictions remains incomplete.

Across each of these dimensions, Bitcoin carries meaningful exposure. Its market is open around the clock, leveraged derivatives are ubiquitous, and the regulatory environment can shift with little warning, making Bitcoin, historically, a particularly volatile risk asset.

Risk on vs Risk off Assets

Market participants commonly describe sentiment in binary terms: risk-on and risk-off. In a risk-on environment, investors favour assets with higher expected returns and accept greater volatility to get them. Equities rise, credit spreads tighten, and speculative positions accumulate.

In a risk-off environment, the inverse holds true. Capital rotates toward assets perceived as stable stores of value: US Treasuries, the Japanese yen, the Swiss Franc, and gold. They tend to appreciate when equities fall as investors flee to safety, providing portfolio protection through negative or low correlation with broader market moves.

Safe havens share a few common characteristics. They are liquid, their value does not depend on any single counterparty, and they have demonstrated resilience across multiple market crises. Gold has held this role for centuries, underpinned by scarcity, physical durability, and its historical function as monetary collateral.

How Risky Is BTC Compared to Other Assets?

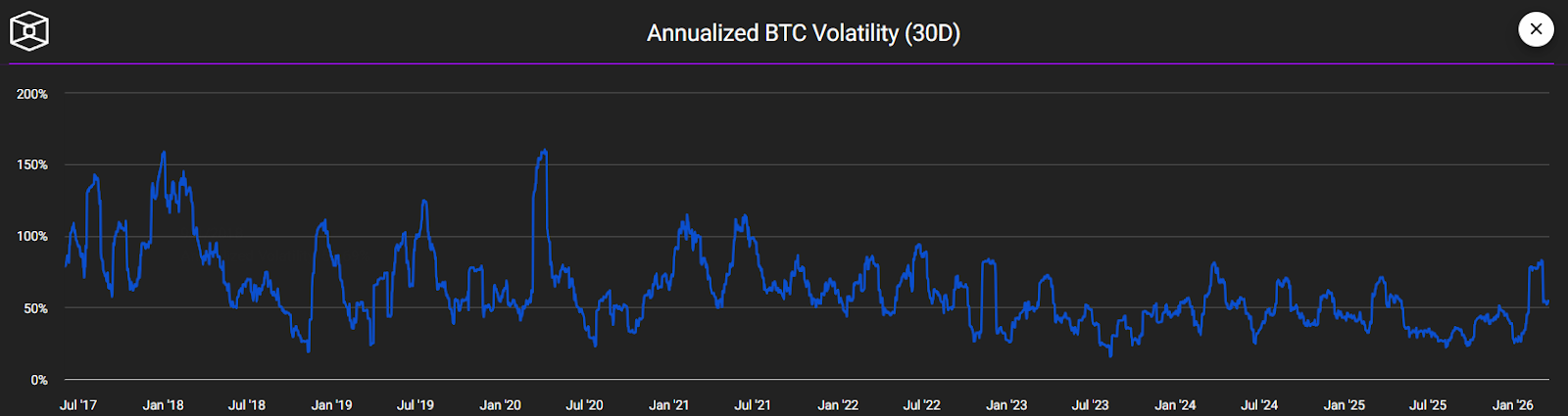

On a historical basis, Bitcoin has been one of the most volatile assets across all major investable assets. During the March 2020 COVID-19 market crash, Bitcoin fell roughly 50% in two days, a drawdown that significantly outpaced the S&P 500's decline over the same period. Similarly, during the 2022 bear market, as the Federal Reserve began its rate-hiking cycle, Bitcoin lost over 75% of its value from peak to trough, consistent with the kind of drawdown seen in high-beta tech equities rather than traditional stores of value.

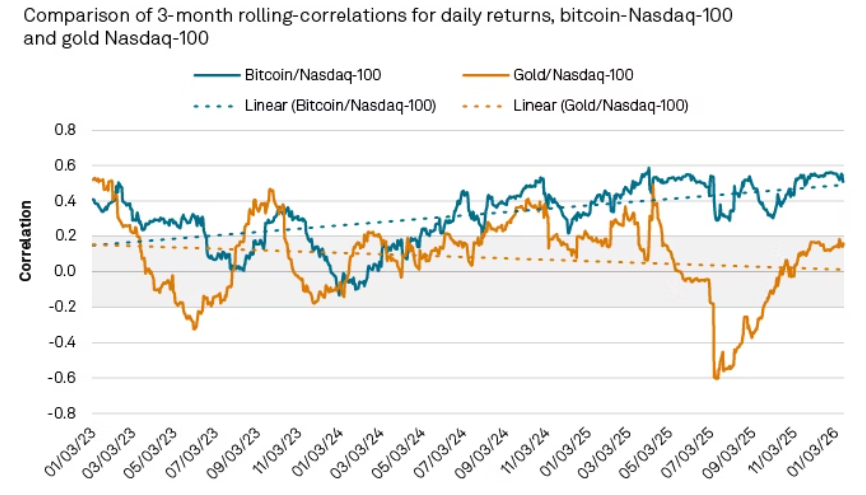

Correlation analysis reinforces this picture. During acute episodes of market stress, Bitcoin’s correlation with the S&P 500 has historically risen. From the perspective of portfolio construction, that is the opposite of what a safe haven asset should do. Assets that correlate with equities in a downturn offer no diversification benefit when it matters most.

Annualized volatility for Bitcoin has typically ranged between 40% and 60%, compared to roughly 15-20% for equities and 10-15% for gold. By that metric alone, BTC sits at the far end of the risk spectrum.

BTC vs Gold Comparison

With its long-standing role as the canonical store of value, gold is the natural reference point for any discussion of Bitcoin as a store of value. The comparison is frequent enough that it has acquired its own shorthand: Digital Gold. The underlying argument draws on genuine structural similarities. Both assets have capped or constrained supply, neither is a liability of any government or corporation, and both have historically been treated as a hedge against currency debasement.

The differences, however, are substantial. Gold has millennia of monetary history, deep institutional infrastructure, and near-zero technological risk. It does not require software to function, cannot be exploited through a protocol vulnerability, and its value is generally not subject to narrative shifts driven by social media.

Bitcoin, by contrast, has a fixed supply of 21 million coins enforced by code, is frictionless to transfer across borders, and carries no storage or custody overhead in the traditional sense. In the 2022 period of elevated inflation, gold notably preserved capital more effectively than Bitcoin, calling into question whether Bitcoin 's digital gold thesis held under the exact conditions it was meant to address.

The correlation between Bitcoin and gold has historically been low, sometimes negative. That divergence has narrowed at certain points in recent market cycles, which drives a theory that the two assets are being held by increasingly overlapping investor bases.

The Case for BTC as a Risk Asset

The weight of historical evidence supports classifying Bitcoin as a risk asset. Its price has consistently risen during periods of loose monetary policy, cheap credit, and broad speculative appetite, and fallen during tightening cycles and market dislocations. Its price action mirrors that of a typical risk asset.

The composition of the Bitcoin market further reinforces this view. Retail traders with high time preference, leveraged futures positions, and discretionary hedge funds represent a meaningful share of daily volume. When margin calls arrive or risk limits are breached, Bitcoin is sold alongside other speculative positions. The liquidation cascades that have repeatedly produced double digit percentage intraday moves are evidence of this market structure.

Regulatory uncertainty further adds to the volatility. In jurisdictions where the legal status of Bitcoin remains unclear, institutional mandates constrain the holding of Bitcoin to a speculative allocation rather than a core investment position. This framing alone preserves its risk asset character within most traditional portfolio frameworks, limiting the perspective of most investors to view it as such.

The Case for BTC as a Safe Haven

The counterargument has grown more substantive in recent years, driven by two distinct developments: the institutionalization of Bitcoin as a financial asset, and its emerging role as a hedge against failures of sovereign financial infrastructure.

Institutional Adoption of BTC

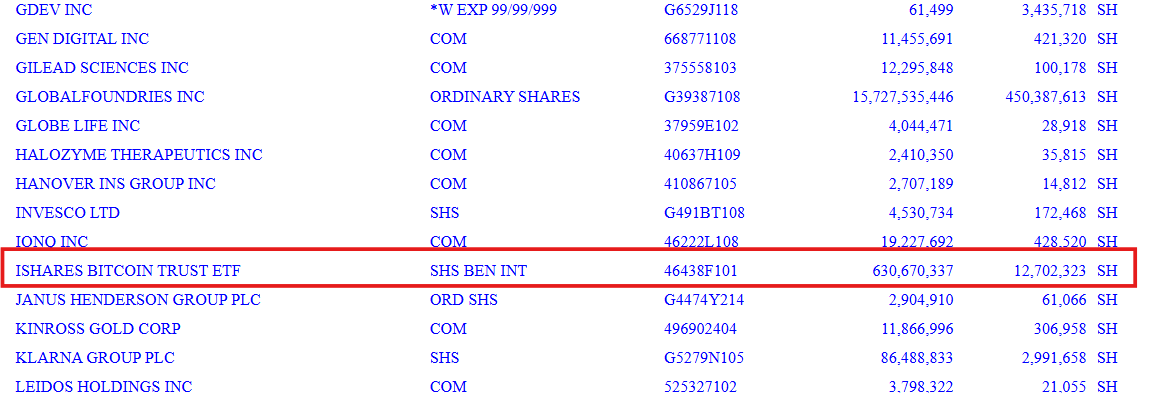

The approval of spot Bitcoin ETFs in the United States in January 2024 marked a structural inflection point for the asset. Products from BlackRock, Fidelity, and others brought Bitcoin within the reach of pension funds, endowments, and sovereign wealth vehicles that previously had no compliant route into the asset. BlackRock's IBIT has since attracted holdings from entities including Harvard Management Company and Mubadala Investment Company, the sovereign wealth fund of Abu Dhabi, funds which typically do not dabble in speculative assets. As of December 2025, the Mubadala Investment Company holds over 12M shares in IBIT, worth over $630M at the time. Across all of its sovereign wealth funds however, the total Abu Dhabi sovereign exposure to IBIT is estimated at approximately $1.3B.

Corporate treasury adoption has followed a parallel track. Strategy (formerly MicroStrategy) has accumulated over 761K BTC, worth over $51B, as its primary treasury reserve, and a growing cohort of listed companies across multiple sectors have followed with smaller allocations. When large, patient institutional holders accumulate and hold through drawdowns, they alter the effective supply available to the market and introduce a structural bid that did not exist in earlier market cycles.

Safe Haven From Sovereign Risk

The more philosophically distinct element of the safe haven argument concerns Bitcoin's nature as a scarce, non-sovereign, decentralized global asset. Unlike gold held in a vault or government bonds held in a clearing system, Bitcoin ownership is enforced by cryptographic proof rather than institutional trust. No government can freeze a Bitcoin wallet through a correspondent banking relationship. No central bank can increase its supply to fund deficit spending.

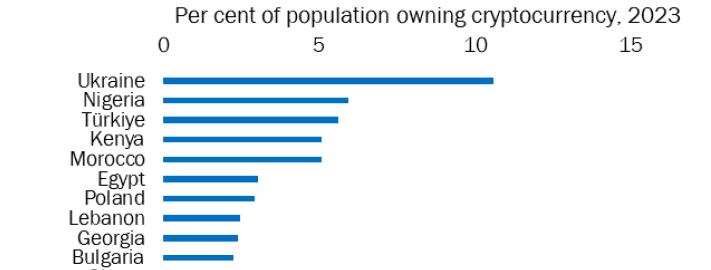

Bitcoin’s decentralization becomes ever more relevant in times of conflict. During the 2022 conflict in Ukraine, citizens used Bitcoin to transfer wealth across borders in circumstances where traditional banking infrastructure was unavailable or compromised. In countries experiencing currency crises, Bitcoin has served as an accessible alternative store of value when access to foreign currency accounts were restricted.

Tensions involving state actors with constrained access to the U.S. dollar-based financial system have further advanced this narrative. Iran, Russia, and other sanctioned nations have explored cryptocurrency as a partial workaround to SWIFT exclusion. While this behaviour reflects necessity as much as conviction, it demonstrates Bitcoin's functional utility as a non-sovereign settlement layer, independent of bias and regulation.

Government adoption at the strategic reserve level brings additional legitimacy to the asset as well. El Salvador made Bitcoin legal tender in 2021, and a number of U.S. states have moved to establish Bitcoin reserve funds. At the federal level, the United States has taken steps toward holding Bitcoin as a strategic reserve asset, a development that, if sustained, would represent a meaningful legitimization of Bitcoin within sovereign financial frameworks. When sovereign entities begin treating Bitcoin as a reserve asset alongside gold and foreign currency holdings, the credibility of the safe haven thesis increases.

Conclusion

Bitcoin's classification as a risk asset or safe haven is not a clear-cut question, and the honest answer is that it has elements of both. The historical record strongly supports the risk asset view: Bitcoin has consistently behaved as a high-beta speculative asset, selling off sharply during risk-off episodes and rallying hardest when liquidity is abundant. The structural argument for the safe haven view, however, has materially strengthened in recent years. Institutional adoption has changed the investor base, the fixed and non-sovereign supply of Bitcoin offers genuine protection against monetary debasement, and its censorship-resistant properties give it a role that no traditional financial asset can replicate in specific geopolitical contexts.

The more consequential question may not be what Bitcoin is today, but what it is becoming. As the institutional infrastructure matures and sovereign adoption expands, the balance between these two identities will continue to shift. For now, Bitcoin occupies a rare and ambiguous position: an asset that trades like a risk asset in the short term while accumulating the structural properties of a long-term store of value.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)

.png)

.png)