July 1, 2026

at

5:45 am

EST

MIN READ

A Guide To How Prediction Markets Work (2026)

A prediction market is a platform where participants buy and sell shares representing the probability of an event occurring. Prices move in real time as new information enters the market. By the time the event resolves, the market has produced a live, crowd-sourced probability estimate that is sometimes more accurate than expert forecasts or traditional polling. This guide explains what prediction markets are, where they came from, how they work mechanically, and what the blockchain infrastructure behind the leading platforms actually looks like.

Summary

- Prediction markets price the probability of future events, aggregating crowd beliefs through a financial mechanism that has existed in informal forms for centuries.

- Platforms like Polymarket and Kalshi are the two biggest prediction markets in 2026.

- Blockchain-based prediction markets use smart contracts, oracles, and CLOBs to handle trading and settlement without a central custodian.

- Prediction markets can cover almost anything but are commonly used for sports, politics and economics.

What Are Prediction Markets

A prediction market is a financial market where traders speculate on contracts representing the probability of a future event. Contracts pay out $1 if the specific outcome occurs, and $0 if it does not occur.

So, for example, during the U.S. presidential elections, a contract for "Donald Trump wins the election" was priced at $0.62, effectively pricing a 62% probability of that outcome. If you bought a share at $0.62 and held onto it until after the election, you would have made a profit of $0.38. Traders and speculators will buy large amounts of these contracts to try and make a significant profit.

Despite feeling like a betting shop, the mechanism behind prediction markets is closer to a futures market. Participants aren't placing wagers with a house, they are actually trading against other participants, with the collective bets determining the probability of a specific outcome occurring. This structure means the market price reflects the aggregated beliefs of everyone trading on the market, weighted by how much capital each participant is willing to put behind their view.

Prediction markets can cover almost anything: elections, economic indicators, sporting events, corporate announcements, geopolitical outcomes, weather, and more. As a result, the true constraint is often that the outcome needs to be unambiguous enough that it can definitively be determined to have happened.

How Do Prediction Markets Work

Prediction markets work by using prices to combine and aggregate people’s beliefs. When someone believes an event is more likely to happen than the current price implies, they buy the contract. When they believe an event is less likely to happen than the current price implies, they sell. As new information enters the world (usually from the news), market participants update their positions, and prices shift accordingly.

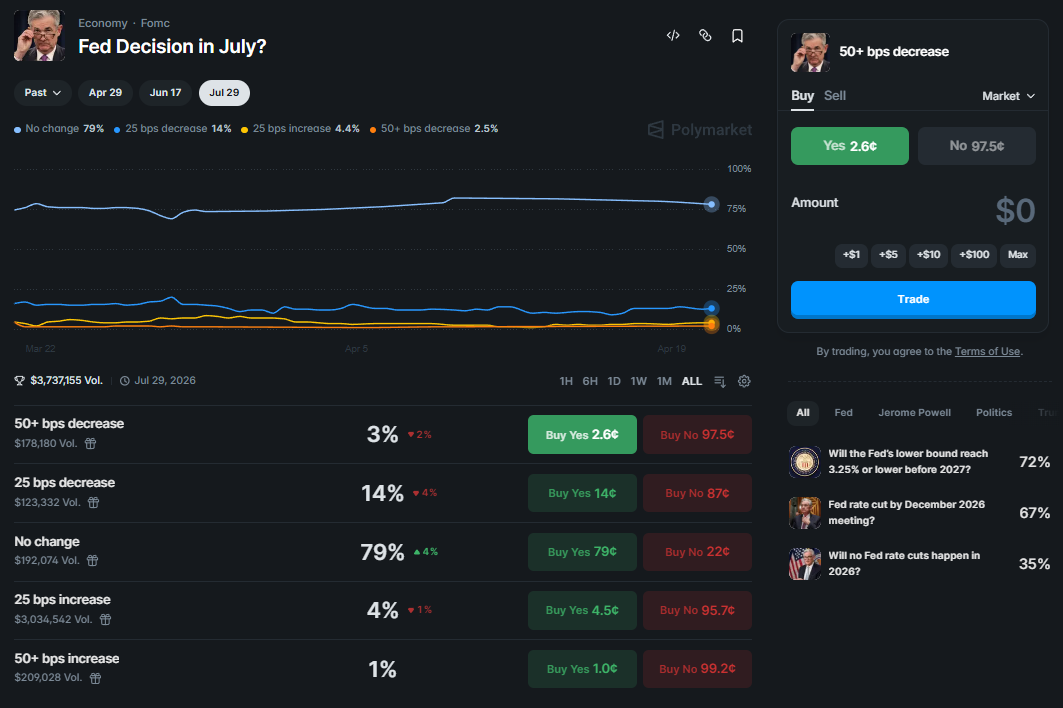

On Polymarket, markets are structured as binary outcome contracts denominated in USDC. A market like "Will the Federal Reserve cut rates in Q1 2026?" has two sides: YES and NO. Each pair of shares always adds to $1. A trader who buys YES at $0.40 is buying a contract that pays $1 if the Fed cuts, for a gain of $0.60, or zero if it does not. The same logic applies to markets covering several possible outcomes, where each outcome will have its own YES or NO options that resolve to either $1 or $0.

Kalshi has the same binary logic but within a regulated U.S. framework. Kalshi is regulated to serve retail U.S. customers directly and lists markets across finance, weather, economic data releases, and politics. Kalshi’s mechanics on how a contract works are similar to Polymarket’s, though it operates with fiat settlement and is subject to CFTC oversight.

Non-blockchain platforms like PredictIt, the Iowa Electronic Markets, and various political betting exchanges in the UK (Ladbrokes, Betfair, and Paddy Power offer political betting) use conventional order books and centralized infrastructure. These platforms handle custody, settlement, and dispute resolution internally. The tradeoff is that users must trust the operator, markets are limited by regulatory constraints, and the platforms cannot operate permissionlessly across borders.

The Blockchain Mechanics of Prediction Markets

When prediction markets moved on-chain, the fundamental mechanics of how they work changed in a few meaningful ways:

Peer-to-peer settlement: Direct transfer of funds between participants without the need for intermediaries.

On platforms like Polymarket, positions are held in smart contracts on the Polygon blockchain network, with the smart contract distributing funds automatically to winning position holders upon resolution. There is no central counterparty holding trader funds. This removes an element of custodial risk that plagued predecessors to Polymarket and Kalshi.

Smart contracts: A contract embedded in code that is self-executing upon certain conditions being met.

From creation to resolution to payout, the lifecycle of a prediction market on a specific event is governed by smart contracts rather than human operators. Market rules are set on-chain and executed deterministically. This makes it harder for an operator to unilaterally alter market terms, withhold funds, or selectively settle disputes in ways that favor the platform.

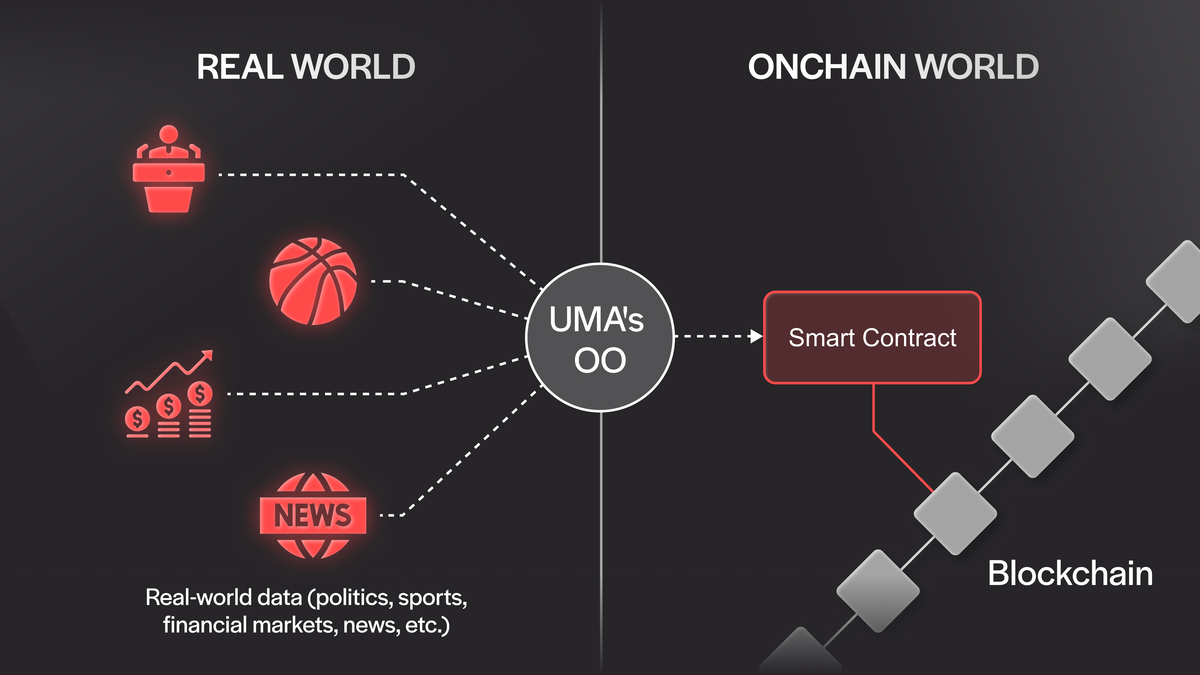

Oracles: Software that connects blockchains to external, off-chain data.

The one point where on-chain prediction markets must interface with the real world is resolution. Oracles do this by supplying verified external data to the smart contract. Polymarket uses UMA Protocol's Optimistic Oracle for dispute resolution. When a market resolves, anyone can propose an outcome. If it goes unchallenged within a window, it is accepted. If challenged, UMA token holders vote on the correct resolution. This decentralized approach introduces complexity in edge cases where outcomes are genuinely ambiguous and there is still a centralization risk as large UMA token holders are able to manipulate resolution outcomes with their votes.

Central Limit Order Books (CLOBs): A mechanism used to connect buyers and sellers of contracts based on price and time.

Polymarket's trading engine uses a central limit order book hosted off-chain to match buy and sell orders efficiently, with settlement occurring on-chain. This hybrid model is better than a fully on-chain order book because the cost of executing each order update on a fully on-chain order book would make trading prohibitively expensive. Kalshi uses a similar CLOB structure, though its infrastructure is entirely traditional, like a regulated centralized exchange.

Collateral: Assets provided by the buyer of a contract to secure the loan.

Prediction market contracts on Polymarket are fully collateralized in USDC. This means that if you want to mint a pair of YES and NO shares worth $1 in total, you must deposit $1 of USDC into the smart contract. This eliminates counterparty credit risk entirely. There is no leverage, no margin call, and no scenario in which a winning position fails to pay out because the counterparty defaulted.

Kalshi's design as a regulated DCM means it operates under CFTC margin rules, which govern how much collateral participants must post and how it is held. Kalshi uses a conventional clearing model rather than the smart-contract-based approach of Polymarket, but the economic function is similar: ensuring losing sides of trades can meet their obligations.

One notable structural difference between Polymarket and Kalshi is access. Polymarket is available globally and does not require identity verification for most interactions, operating through crypto wallets. Kalshi requires US-based account registration and identity verification as part of its CFTC-compliant structure. The tradeoff is that Kalshi can serve U.S. retail customers legally, while Polymarket formally restricts U.S. users despite being technically accessible to anyone with a crypto wallet.

Analyzing Prediction Market Data On-Chain

As prediction markets like Polymarket have moved on-chain, the data they produce is now accessible to anyone. Every transaction, position, and outcome is recorded and verifiable. To help participants navigate this ecosystem, Arkham Intel has built a comprehensive analytics platform on top of our existing platform that is dedicated to prediction market data.

Bringing on-chain analytics to prediction markets allows for several new ways to track and interpret market behavior:

Trader ELO Rating: An Elo/MMR-style system that ranks traders based on prediction accuracy.

Every correct prediction that a trader makes increases their Elo score relative to other traders. Correct predictions at lower odds increase a trader's Elo by more than correct predictions at higher odds.

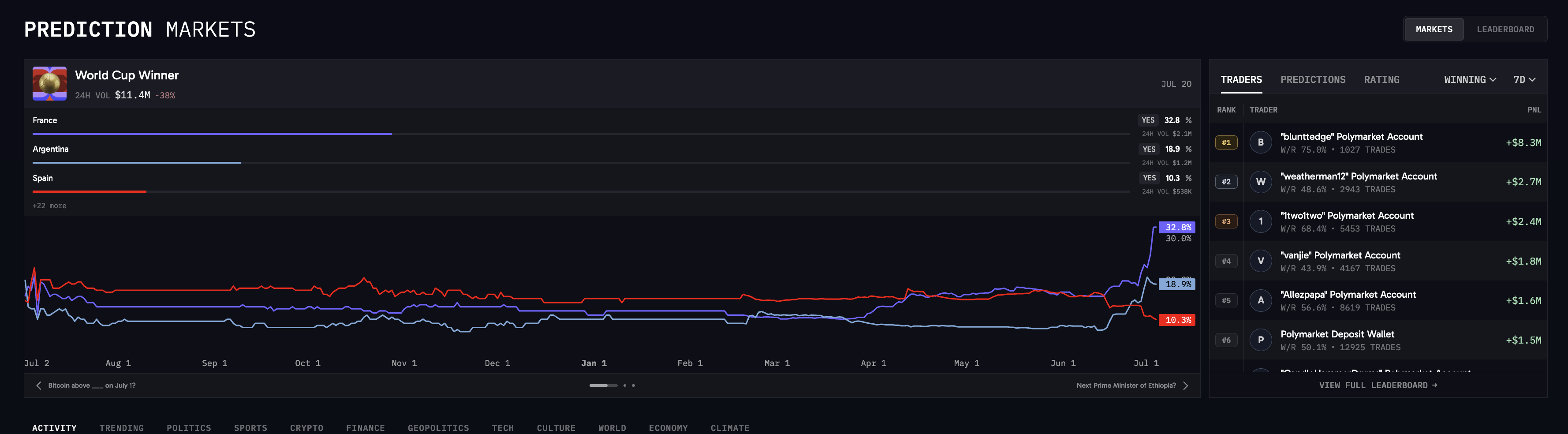

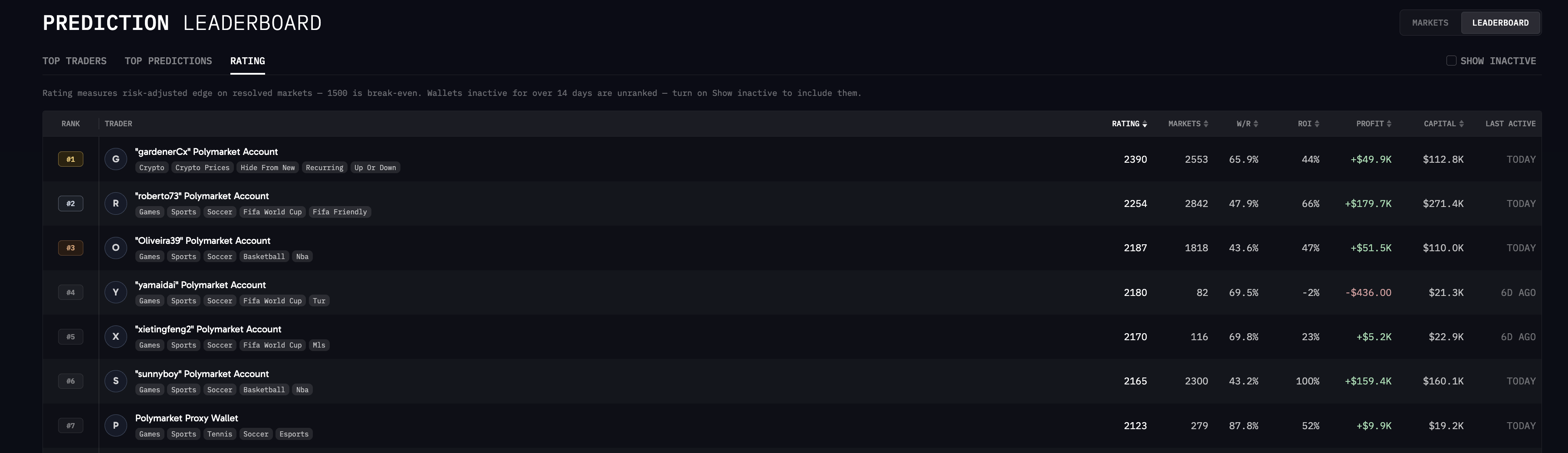

Trader analytics: Comprehensive tracking of top prediction market participants based on Profit and Loss (PNL).

Users can view a feed of the top prediction market traders by PNL, alongside a history of their open and past positions. The platform provides analytics on individual performance, including Return on Investment (ROI) and overall win rates. Users can also set alerts on specific transactions and examine a trader's broader on-chain activity beyond just their prediction market wagers.

Here’s a list of the specific metrics available to users:

- Account Value: To show the scale at which they are trading and their "skin in the game."

- Active Positions: To reveal real-time convictions, allowing users to track, copy, or fade current strategies.

- Total PNL & Total ROI: To measure raw bottom-line success versus actual trading efficiency (leveling the playing field between whales and small accounts).

- Volume: To distinguish between highly experienced, frequent traders and casual participants.

- Biggest Win: To determine if a trader's PNL is based on consistent skill or one lucky outlier.

- Win Rate: To gauge consistency and accuracy.

The screenshot below from Arkham Intel Predictions Analytics shows a trader’s top closed positions, ordered by PNL:

Live market monitoring: A real-time feed of prediction market trades across the ecosystem.

Participants can monitor a live tape of prediction market trades as a whole, or filter down to all trades for a specific market they are currently tracking. Markets can be viewed across a range of active categories - politics, sports, and crypto - providing visibility into market movements and participant behavior as real-world events unfold.

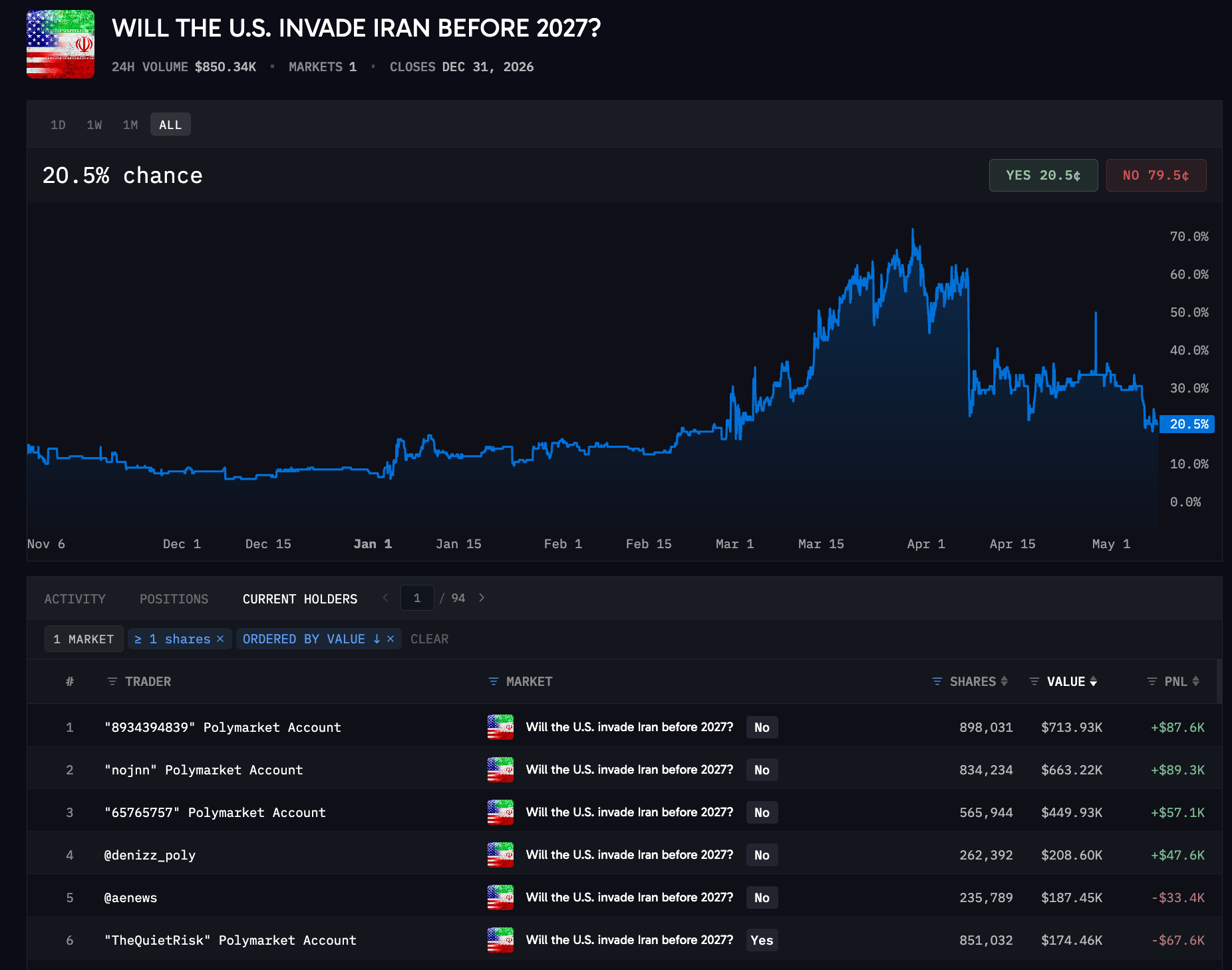

The following screenshot shows Prediction Market analytics for ‘Will the U.S. Invade Iran Before 2027?’. The table at the bottom shows analytics on the current contract holders ordered by value.

Entity deanonymization: The integration of real-world identities and known entities with on-chain prediction market data.

Arkham's existing catalogue of over 3.5 billion address labels and 800,000 verified entities allows users to deanonymize many on-chain traders. Users can now see the activity of known traders, funds, and key opinion leaders, contextualizing the capital flowing into specific YES or NO contracts.

There are also 20 different Polymarket-specific tags that provide insights into hundreds of thousands of different addresses. Key tags include:

- Polymarket Whale

- Polymarket High PnL Trader

- Polymarket High ROI Trader

- Polymarket High Win Rate Trader

- Polymarket Market Maker

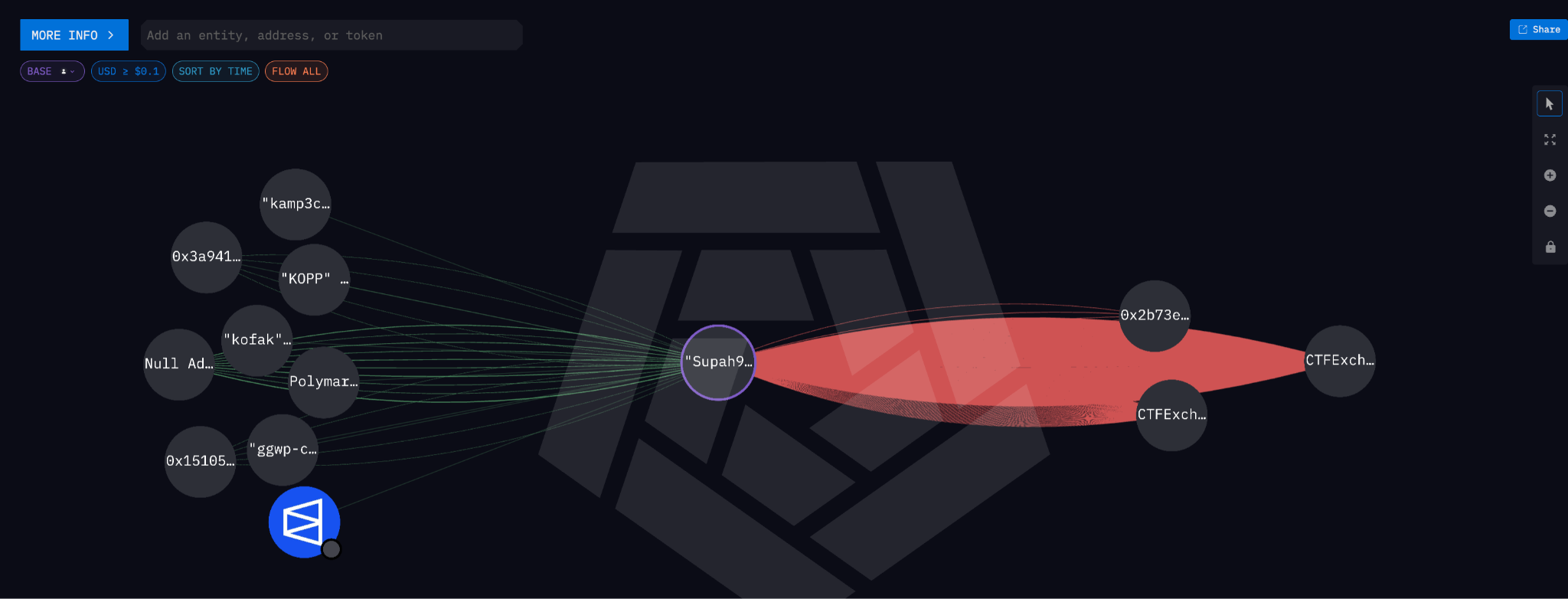

Data visualization: Tools to map on-chain trading behavior directly onto market pricing.

Within individual markets, trades can be sorted by current and past positions based on PNL, or by the current holders of YES and NO shares. A built-in filtering mechanism allows users to select any specific address and overlay that trader's exact entry and exit points directly onto the market's price chart, providing a visual representation of their trading strategy and timing.

History of Prediction Markets

The conceptual roots of prediction markets go back centuries. Scholars have found records of betting on papal elections in 16th-century Rome and wagers on U.S. presidential races as far back as 1868, with active markets reported in newspapers of the era. These were informal markets, but they functioned on the same principle: participants risked money on outcomes, and the aggregate of those bets produced a price.

In 1945, Austrian economist and philosopher Friedrich Hayek set the stage for the modern prediction market, with his essay “The Use of Knowledge in Society”. The piece proposed the concept of price as a source of information, suggesting that prices in the market were a reflection of the market’s collective views. However, this crucial concept remained largely conceptual due to the proliferation of wider scale polling technologies and stricter anti-gambling laws. In 1988, researchers at the University of Iowa had built the Iowa Electronic Markets (IEM), an academic prediction market that has run continuously since and remains one of the most studied examples in the field.

In the early 2000s, Intrade took prediction markets from an academic experiment to the general public. It quickly became the most visible commercial prediction market, allowing users to trade on political events, sports, and financial outcomes through a centralized web platform. At its peak, Intrade's prices were cited regularly by journalists and analysts as credible probability estimates. However, the platform shut down in 2013 following regulatory pressure and revelations of internal financial mismanagement.

After the shutdown of Intrade, PredictIt filled the void, operating under a no-action letter from the CFTC. The platform allows political trading at low volume caps per contract and per account. Its regulatory constraints limited liquidity but allowed it to operate legally within the U.S. Kalshi instead took a different approach, going through the full CFTC registration process as a designated contract market (DCM), giving it the legal standing to offer event contracts to U.S. users without position caps. Kalshi launched in 2021 and has since expanded its market categories substantially to become one of the two leading prediction markets alongside Polymarket.

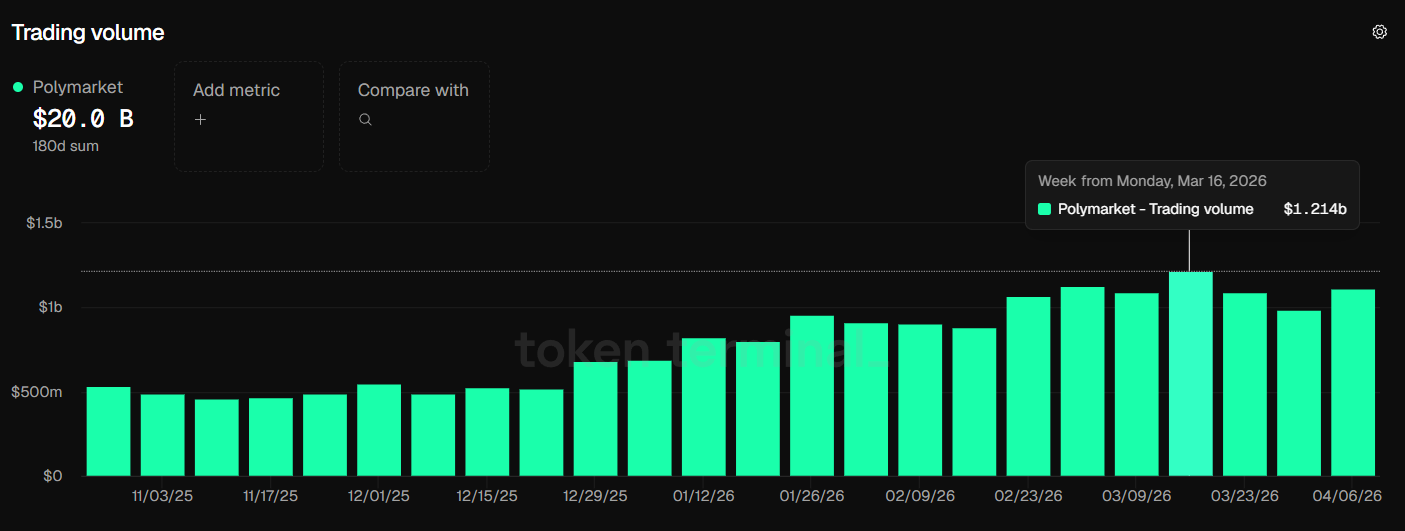

The on-chain era for prediction markets kicked off with Augur, which launched on Ethereum in 2018 and attempted to build a fully decentralized prediction market. Augur's design was technically sophisticated but suffered from low liquidity, complex user experience, and a disputed resolution mechanism that made markets difficult to settle cleanly. Polymarket launched in 2020 and took a more streamlined approach, building on Polygon and prioritizing user experience. It has since become the dominant venue globally by trading volume, clearing approximately $800M in weekly volume over the past six months.

Kalshi launched in 2021, becoming the first CFTC-licensed prediction market in the U.S. To accelerate growth, Kalshi embedded its markets into mainstream retail platforms like Robinhood - which now drives over half its volume. Kalshi has now overtaken Polymarket as the industry leader, with $39.5 billion in total notional volume compared to Polymarket's $29.2 billion. Kalshi is currently valued at $22 billion.

Conclusion

Prediction markets have moved from academic curiosity to active financial infrastructure in just under 30 years. The 2024 election cycle demonstrated that these platforms can attract real liquidity and generate probability estimates that compete seriously with traditional polling and forecasting. The two models that have emerged: Polymarket's permissionless, on-chain approach and Kalshi's regulated, CFTC-registered structure, represent different bets on how this market develops. One prioritizes global accessibility and decentralization; the other prioritizes regulatory clarity and U.S. retail access.

U.S. regulators have historically been skeptical of event contracts that resemble gambling, and the CFTC's posture toward platforms like Polymarket remains an open question. On the technical side, oracle design continues to be a weak point, with the accuracy of on-chain prediction markets dependent on having reliable, manipulation-resistant resolution mechanisms. What is clear, however, is that the core mechanism, which uses financial markets to aggregate probabilistic beliefs, is here to stay.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)