April 4, 2026

at

6:00 am

EST

MIN READ

Crypto Backed Loans: A Guide To Borrowing Against Your Bitcoin (And Other Digital Assets)

For most of crypto's history, holding Bitcoin or Ethereum meant one thing: you wait. You accumulate, you hold through the volatility, and you hope. But sitting on a large position while needing liquidity has always been an uncomfortable trade-off. Selling meant triggering a taxable event and losing your exposure and potential upside. Doing nothing meant capital locked up with no utility.

Crypto-backed loans change that equation. By putting up digital assets as collateral, borrowers can access liquidity while keeping their underlying position intact. The concept has existed in DeFi since the earliest days of Aave (then known as ETHLend), Maker and Compound, but the landscape has since shifted considerably. Centralised lenders entered the space, imploded spectacularly during the 2022 bear market, and now traditional financial institutions are moving in to fill the gap. The market for crypto-backed lending is growing fast, and it's worth understanding how it actually works.

Summary

- Crypto backed loans let holders borrow against digital assets without selling, avoiding taxable events while maintaining market exposure.

- DeFi protocols like Aave and MakerDAO pioneered on-chain crypto lending, while CeFi lenders later expanded access to less savvy users before a wave of collapses in 2022.

- Liquidation risk during market downturns is the single biggest danger, as rapid price drops can wipe collateral before borrowers can react.

- Traditional financial institutions including banks and fintech lenders are now entering the crypto lending market, signalling broader institutional acceptance.

What Is a Crypto-Backed Loan?

A crypto-backed loan is a type of secured loan where the borrower deposits cryptocurrency as collateral in exchange for funds, typically in fiat currency or stablecoins. The loan proceeds can then be used for anything, including day-to-day expenses, investing in other assets, covering short-term cash needs, and more.

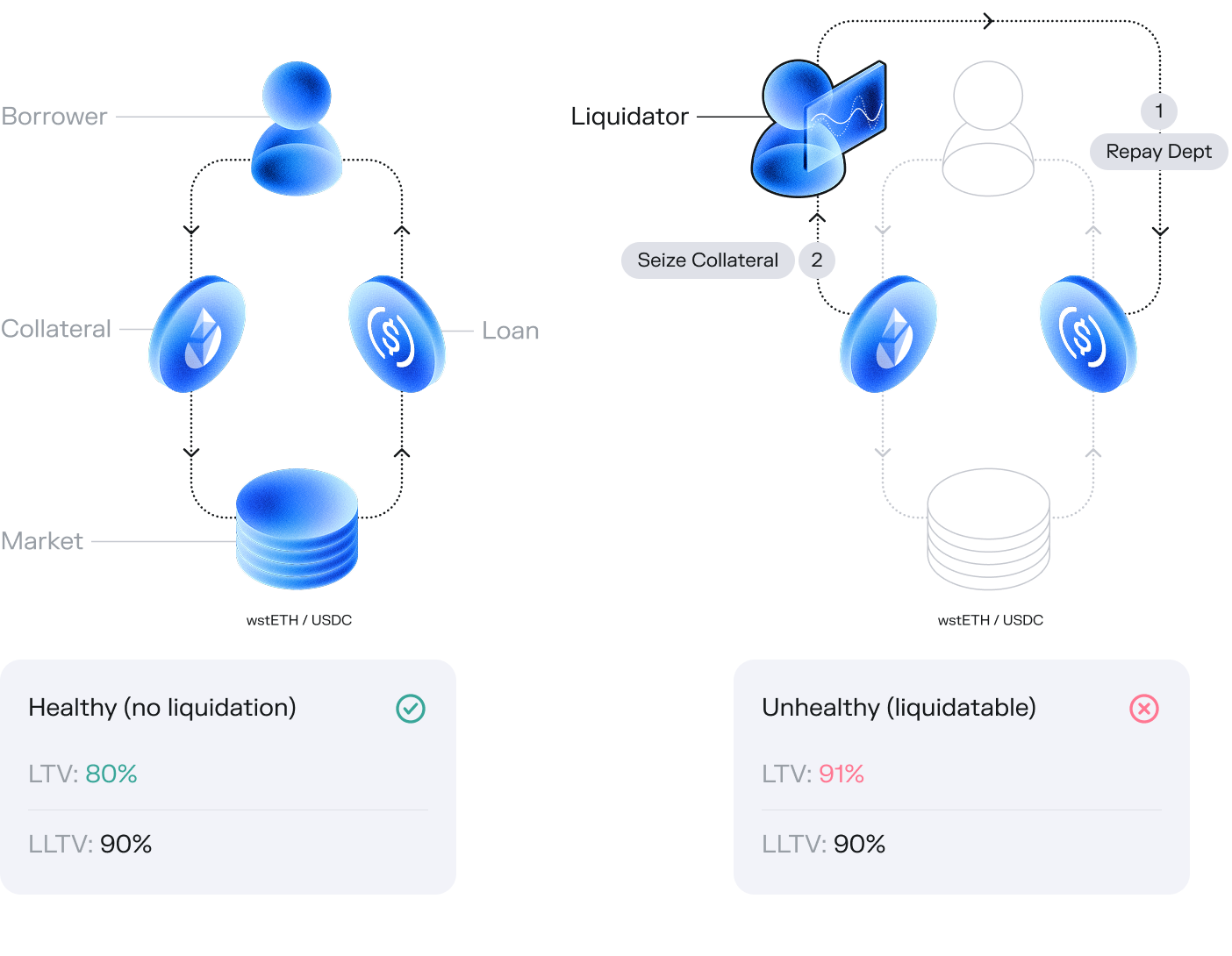

The lender holds the collateral for the duration of the loan and if the borrower repays the principal with interest, they get their crypto back. However, if the collateral value drops below a certain threshold, the position gets liquidated, which gives the lender the right to sell off the collateral to recover the loan value.

The key metric governing these loans is the loan-to-value ratio (LTV). For example, a 50% LTV means that a borrower can access $50,000 in liquidity by depositing $100,000 worth of Bitcoin. In general, crypto-backed loans require overcollateralisation, meaning borrowers must post more collateral than the loan value, to buffer against price volatility. Collateral requirements vary by platform and by asset, with Bitcoin and Ethereum traditionally attracting the most favourable LTV ratios given their liquidity and relative market depth.

The History of Crypto-Backed Loans

The foundations of crypto lending were laid in DeFi. Maker first launched in December 2017 and allowed users to lock Ethereum as collateral to mint DAI, a decentralised stablecoin. This was, functionally, the first widely used crypto-backed loan product. Compound followed in 2018, introducing algorithmic money markets where users could supply and borrow assets with interest rates set automatically by supply and demand. Although ETHLend (now Aave) launched earlier in November 2017, their initial model used a peer-to-peer lending market, which was eventually phased out in 2018 due to its fragmented liquidity and inefficiency.

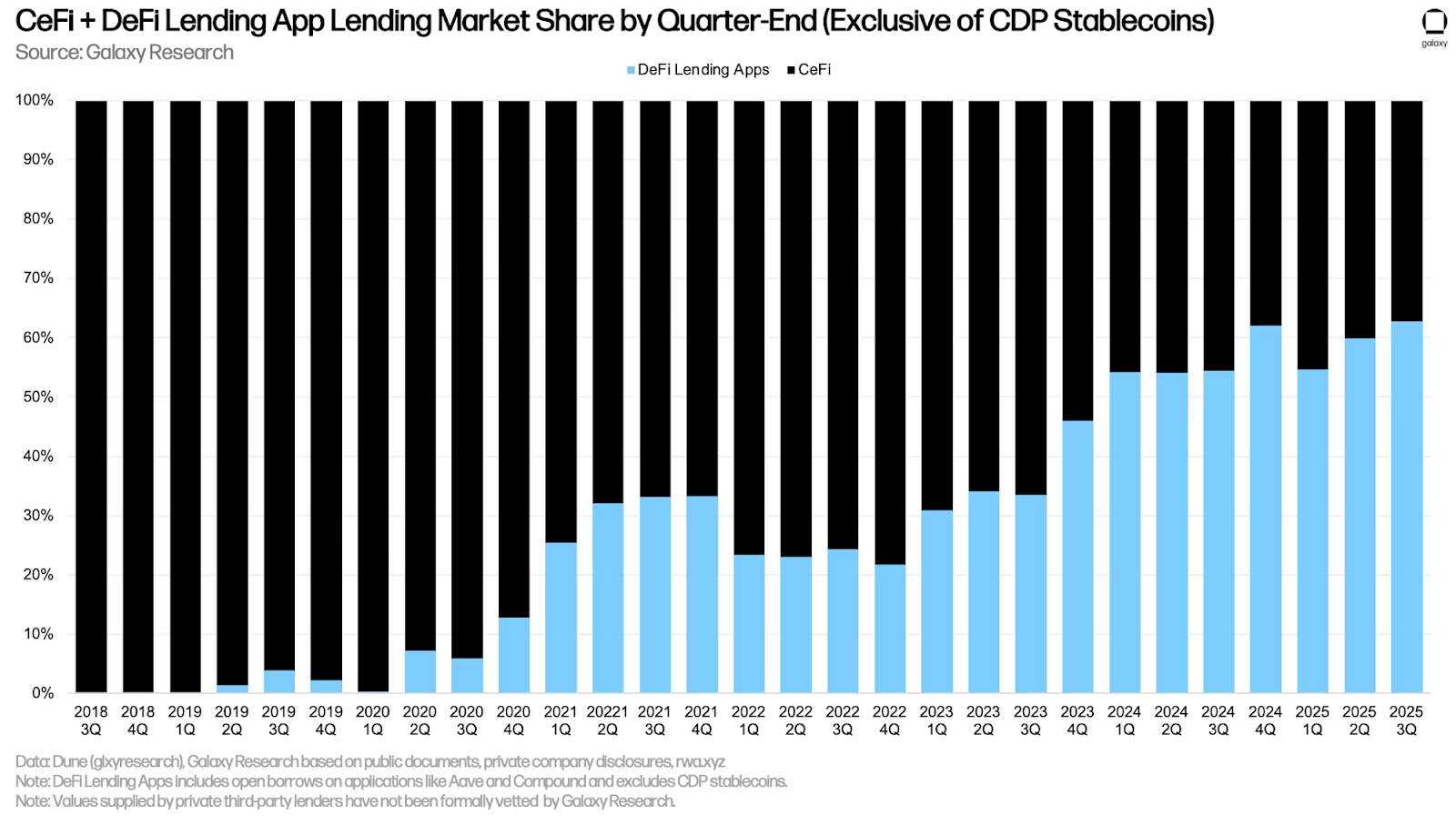

Centralised crypto lenders then emerged to bring this model to a broader audience. BlockFi, Celsius, Genesis, and Nexo all launched retail crypto lending products between 2018 and 2020, making it easier for users to borrow against their holdings without interacting with smart contracts. These platforms grew rapidly during the 2020-2021 bull market as yields on crypto deposits and demand for dollar liquidity both surged.

However, the 2022 bear market was catastrophic for the CeFi lending sector. The collapse of the Terra-LUNA ecosystem triggered a cascade of liquidations and bad debt across the ecosystem. Three Arrows Capital defaulted on loans from Genesis and Voyager. Celsius froze withdrawals in June 2022 and filed for bankruptcy shortly after. BlockFi followed suit later that year. The bankruptcies revealed a common trend across CeFi lenders: rehypothecation of customer collateral, poor risk management, and opaque balance sheets.

DeFi protocols, by contrast, largely functioned as designed. Aave and Compound's liquidation mechanisms fired automatically when collateral fell below required thresholds, keeping the protocols solvent. This distinction became important in the post-2022 reassessment of crypto lending risk.

Who Offers Crypto-Backed Loans?

DeFi

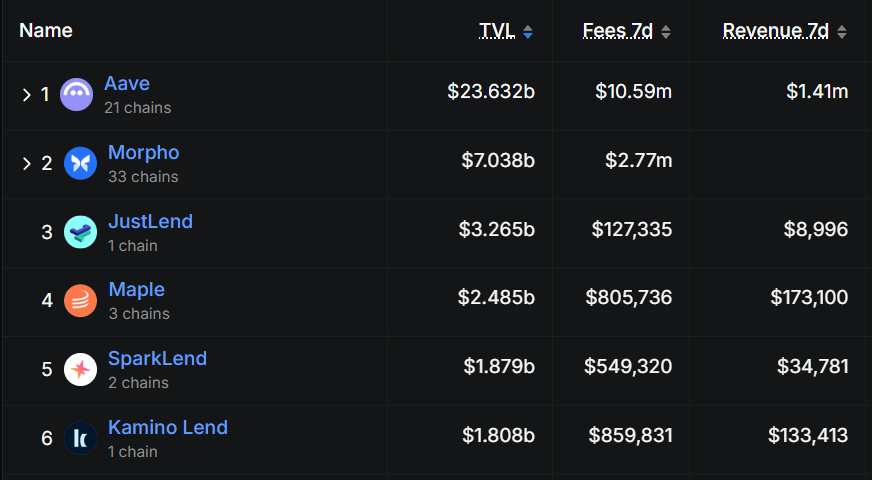

Decentralised protocols remain the most transparent and accessible option for crypto backed borrowing. Aave, Maker (now known as Sky), and Morpho remain some of the largest, collectively holding over $35 billion in total value locked across multiple chains. Users deposit collateral directly into smart contracts, borrow against it permissionlessly, and liquidation parameters are publicly auditable. There is no counterparty risk from a centralised intermediary, though smart contract risk and oracle manipulation remain relevant considerations. Interest rates on DeFi loans are typically variable and determined algorithmically based on current utilisation of the lending pools, although several DeFi protocols have recently begun exploring fixed rate loans as well.

CeFi

Centralised lenders offer a more familiar user experience, often with fixed rate options, customer support, and the ability to use a wider range of collateral types. After the wave of bankruptcies in 2022, the surviving and newly launched CeFi lenders operate with significantly more conservative risk frameworks. Today, companies like Nexo, Ledn, and Unchained, among leading centralized exchanges, are among the most active players in this space. The trade-off for convenience is that users must give up custody of their assets to these lenders, thereby creating counterparty risk.

TradFi

Traditional financial institutions are now the newest entrants to this industry. Several banks, fintechs, and broker-dealers have launched or are developing their own Bitcoin-backed loan products. The regulatory clarity provided by frameworks like the EU's MiCA regulation and evolving US guidance in recent years has also made it easier for regulated entities to engage with digital asset collateral.

The Benefits of Borrowing Against Your Crypto

The most obvious benefit of crypto-backed loans is liquidity without selling. Long-term holders who believe in Bitcoin's long-term trajectory can access cash without exiting their position. Depending on jurisdiction, the loan proceeds are generally not considered a taxable event in the way a sale would be. This makes crypto-backed loans a potentially tax-efficient way to generate liquidity from an appreciating asset. For large holders, selling even a portion of a position can move markets and attract attention. A loan allows them to access liquidity quietly, without broadcasting their activity on-chain as a sale.

From the standpoint of speed and accessibility, DeFi loans can be drawn instantly and globally, without credit checks or income verification. Anyone with sufficient collateral can take out a crypto-backed loan. For users in markets with limited access to traditional credit, this can be a viable alternative to the traditional finance system.

Finally, crypto backed loans can serve as a tool within broader treasury or portfolio management strategies. Borrowing against crypto to buy other assets, fund business operations, or meet tax obligations without selling is a common use case among more sophisticated holders.

The Risks of Borrowing Against Your Crypto

The central risk in crypto-backed loans tends to be liquidation risk. If the collateral value drops sharply, the platform will liquidate the position to recover the loan. Given how volatile crypto assets can be, this can happen faster than most users are able to react. During the March 2020 crash, both Bitcoin and Ethereum dropped by over 40% in a single day, triggering mass liquidations across DeFi. Borrowers who were not monitoring their positions closely had collateral sold out from under them before they could top up..

Interest rates on crypto-backed loans can also be substantial. DeFi interest rates in particular can spike dramatically during periods of high demand. Borrowers who enter loans during periods of low rates may find costs rising significantly over time when demand picks back up.

For CeFi platforms, counterparty risk remains the main concern despite the more conservative risk frameworks following 2022’s fallout. Platform insolvency or fraud can result in loss of collateral, as seen with BlockFi and Celsius customers who are still working through bankruptcy claims even years later.

On the DeFi side, smart contract exploits present a different category of risk. Even well-audited and long-standing protocols have been the victims of costly exploits. Oracle manipulation, where the price feed used to calculate collateral value is compromised, has also been a common attack vector on lending protocols.

Finally, regulatory risk is always a consideration in the background, particularly for CeFi lenders operating in uncertain jurisdictions. Regulatory action resulting in a platform halting operations could complicate access to collateral for active borrowers.

TradFi: Crypto-Backed Loans

The entry of traditional financial institutions into crypto backed lending represents a notable shift in the crypto lending landscape. The approval of spot Bitcoin ETFs in the U.S. in January 2024 legitimized Bitcoin as a financial asset in the eyes of many institutional actors. At the same time, regulatory frameworks in Europe have started to provide clearer guidance on how digital assets can be used as loan collateral within regulated banking structures.

In the U.S., large institutions have been cautious but increasingly active. Goldman Sachs made history with the first Bitcoin-backed loan in 2022. Since then, several other financial institutions have stepped into the arena, with JPMorgan expanding their offerings to allow Bitcoin and Ethereum-backed loans last year, after accepting spot Bitcoin ETFs as collateral earlier in the year. In the mortgage finance space, Fannie Mae also recently enabled Bitcoin and USDC as collateral for down-payment loans, in a landmark move for U.S. housing.

Banks face a particular challenge here, due to their regulations under the Basel III framework. Under this framework selected cryptocurrencies are allocated a 1,250% risk weight, or the highest possible risk weight for any asset class. This means that for every $100 of Bitcoin held by the bank on their balance sheet, they must hold another $100 in equity as a reserve. This can make it highly capital inefficient for banks to hold cryptocurrencies on their balance sheet.

The Future of Crypto Backed Loans

Several converging trends point to continued growth in crypto-backed lending. Clearer regulation across major jurisdictions will lower the compliance barriers for traditional institutions. As more banks and asset managers hold or facilitate crypto exposure for clients, the demand for liquidity products against those holdings will naturally follow.

Tokenization of assets further advances this demand. If real-world assets like U.S. Treasuries and equities are increasingly brought on-chain, the collateral universe for DeFi lending protocols expands significantly. Aave and similar protocols are already exploring the integration of tokenised RWAs as collateral, which could bring a much larger pool of capital into on-chain lending.

On the risk management front, more sophisticated oracle systems, cross-chain liquidity solutions, and improved liquidation mechanisms in DeFi are gradually addressing the protocol-level risks that have historically deterred risk-averse borrowers. AI-driven monitoring tools that alert borrowers to approaching liquidation thresholds are also becoming more common.

The longer-term trajectory for this market looks like one of convergence. DeFi protocols will become more compliant and composable, while CeFi lenders will rebuild trust through transparency and conservative leverage. At the same time, traditional financial institutions will gradually develop or acquire the infrastructure needed to serve clients who want to borrow against digital assets within familiar regulatory frameworks.

Conclusion

Crypto backed loans have come a long way from the early days of Maker and a few centralized lenders operating with minimal oversight. The 2022 collapse wiped out a significant chunk of the CeFi lending sector, but it also forced a reset toward more sustainable, transparent models. With DeFi protocols having proved their resilience and CeFi players having emerged with better risk frameworks, traditional financial institutions are now beginning to take the space seriously.

For holders with significant crypto positions, the ability to borrow against those assets without selling can be a genuinely useful financial tool. But, the risks are real and the liquidation mechanics are unforgiving. As infrastructure improves and the regulatory environment becomes clearer, crypto-backed loans could very well be on course to become a mainstream feature of both digital asset finance and traditional lending.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)

.png)

.png)