May 22, 2026

at

10:30 am

EST

MIN READ

Polymarket vs. Kalshi: How The World's Two Biggest Prediction Markets Compare

Prediction markets have quietly crossed over from niche crypto markets to mainstream financial reference points. When major news networks began citing Polymarket odds alongside polling averages during the 2024 U.S. presidential race, it was clear that prediction markets had crossed the chasm to the general public.

Today, Polymarket and Kalshi are the two largest platforms in this space, but their approach and architecture could not be more different. One is a decentralized, crypto-native protocol with a global user base and permissionless architecture, while the other is a federally regulated U.S. exchange that functions closer to a futures clearinghouse than a blockchain application. As they converge on the same market categories and compete for the same traders, the differences lie in how they handle custody, fees, regulation, and market resolution.

Custodial Strategy and Platform Architecture Compared

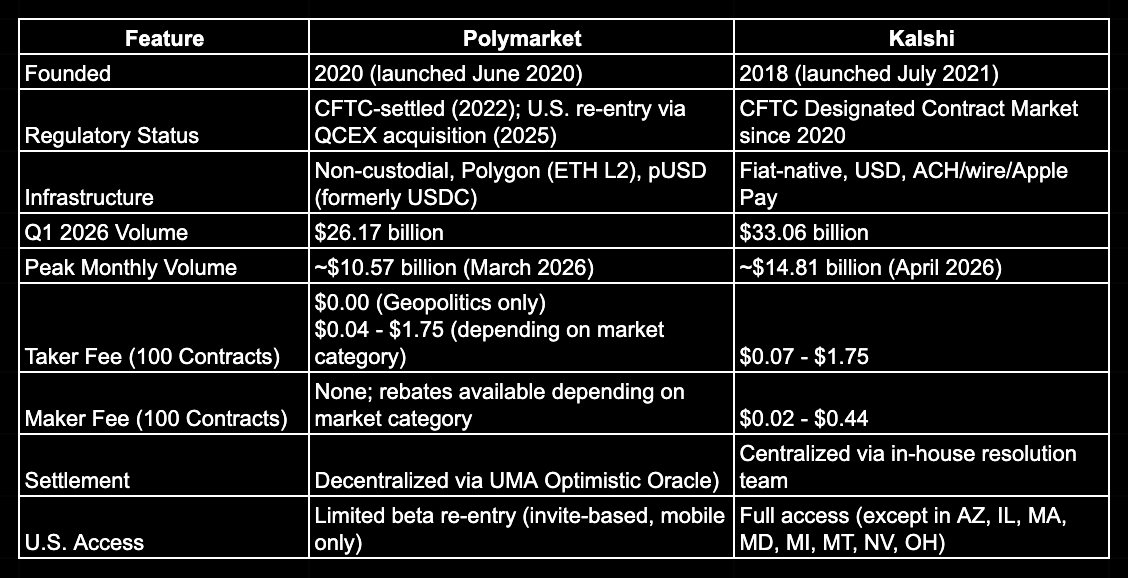

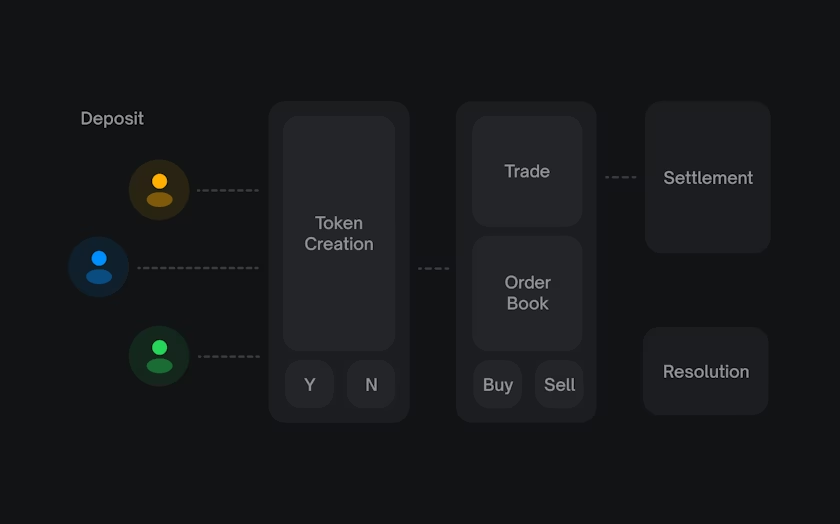

Due to the difference in their approach, their architectures also differ greatly. Polymarket operates as a non-custodial protocol built on Polygon, an Ethereum Layer 2 (L2) network. Users hold their own funds in self-managed wallets, trading against one another using Polymarket’s own stablecoin, pUSD. Polymarket is designed as a non-custodial system where users retain control of their wallets and assets. Positions exist as conditional tokens on a blockchain, with settlement delegated to UMA’s Optimistic Oracle system. This structure allows the platform to serve users globally without routing capital through traditional banking rails.

Kalshi runs on an entirely different set of rails. User deposits arrive via ACH transfer, wire, or Apple Pay in U.S. dollars. Kalshi holds user funds as a regulated clearinghouse, Kalshi Klear LLC, which received CFTC registration as a Derivatives Clearing Organization in 2024. This architecture is much closer to that of a futures exchange than a crypto protocol, which comes with both the regulatory credibility and the access constraints that model implies.

For the end users, Polymarket's on-chain architecture means instant, global access but requires familiarity with wallets and stablecoins, whereas Kalshi works exactly like a brokerage account and accepts standard payment methods, but its footprint is currently limited to jurisdictions where event contract trading is legally permissible.

Trading Volume Compared

The 2024 U.S. presidential election was the catalyst for prediction markets, catapulting them from niche markets to sources quoted by mainstream media.

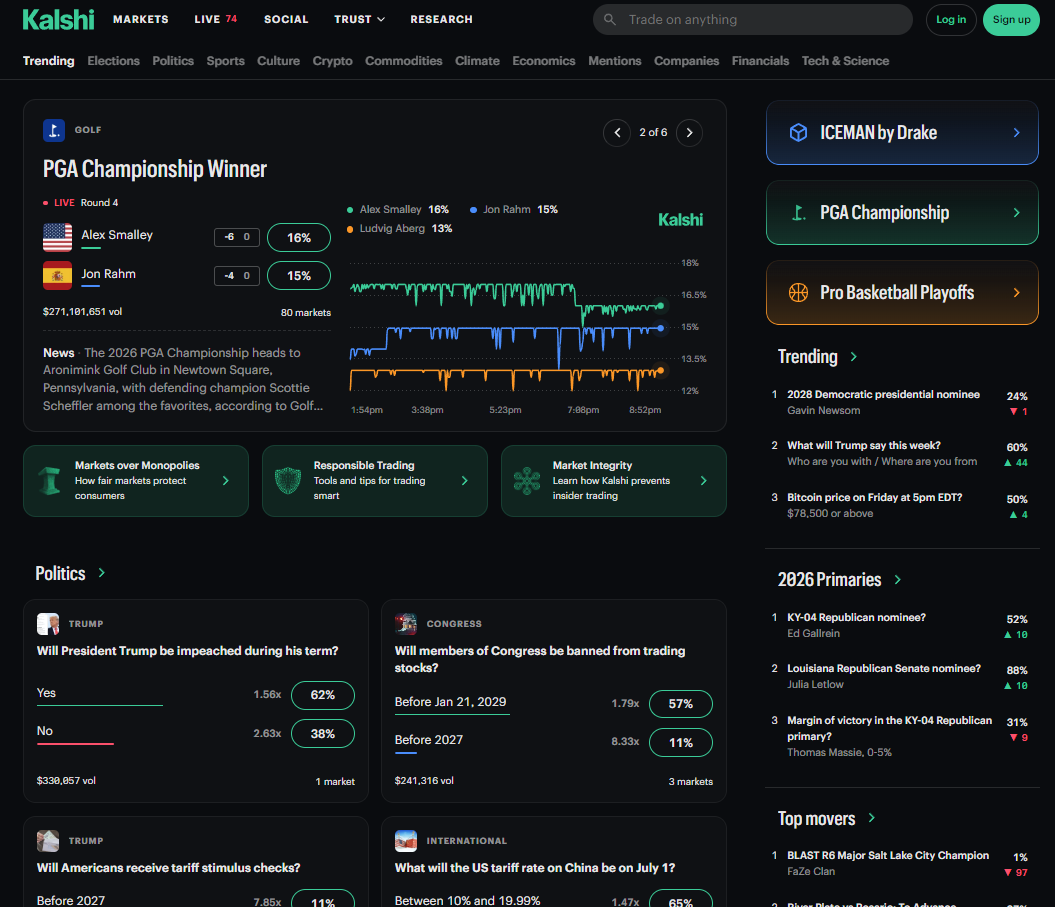

Polymarket handled over $3.7 billion on the presidential race, pushing its volume for the quarter to almost $11 billion, or 4x the prior quarter. Monthly active traders peaked at 314,500 in December, and open interest hit $510 million during election week in November. In Q1 2026, Polymarket hit an all-time high volume for the quarter of $26.17 billion.

Kalshi's volume was substantially lower during the 2024 election cycle due to its ongoing legal battle in October 2024. However, despite only having just over 30 days to roll out their contracts after their legal victory, they still achieved a record high volume of $245 million traded on Election Day itself. Since then, Kalshi’s volume has only continued to surge, with Q1 2026 hitting a record $33 billion in volume traded, notably higher than Polymarket’s in the same period.

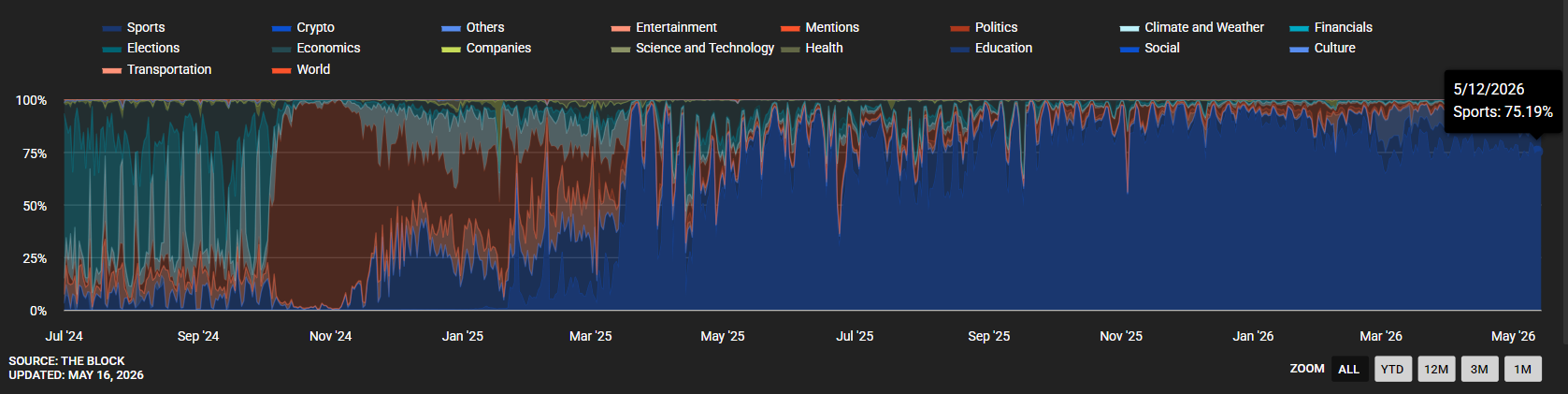

The composition of that volume tells a different story for each platform. Polymarket's strength historically centers on global politics, crypto-adjacent events, and internet culture markets, categories where its international, crypto-native user base has more interest in. Kalshi's edges lie in more U.S-centric markets, including U.S. macroeconomic data like the Federal Reserve rate decisions, CPI prints, unemployment figures,and U.S. sports, particularly NFL, NBA, and MLB. Interestingly, sports betting forms a significant portion of trading volumes for both prediction markets, making up 45% of Polymarket’s daily volume and 75% of Kalshi’s.

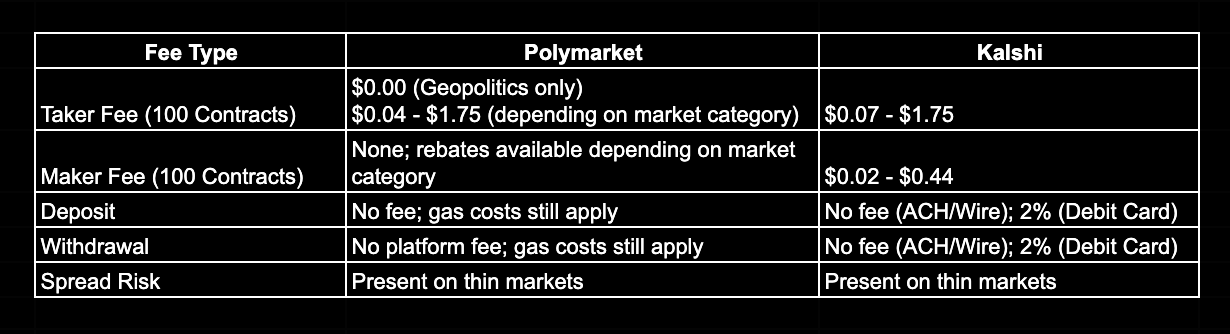

Fees Compared

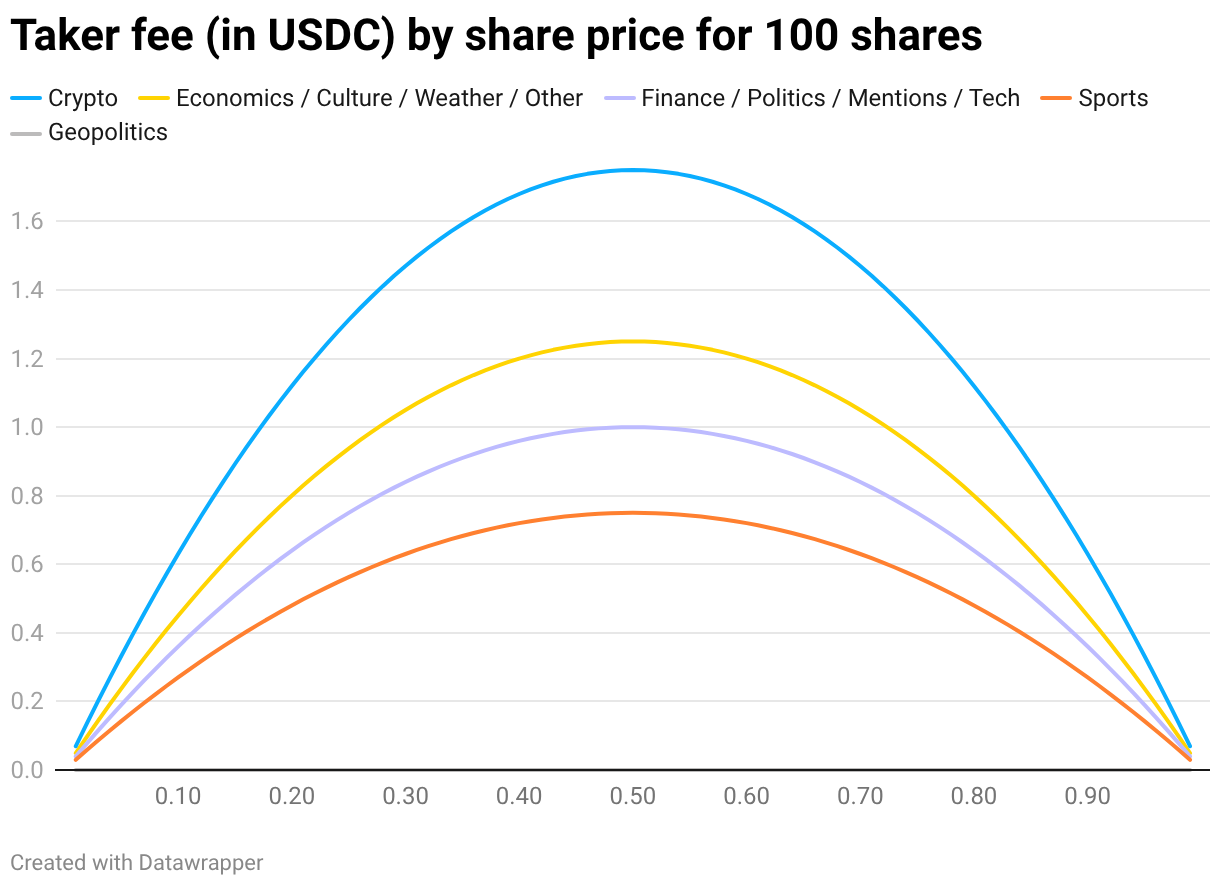

For most of its existence, Polymarket charged nothing to trade and covered users’ gas fees as part of their growth strategy. However, this has changed over the years as the platform grew to become a leader in the space. Since early 2026, Polymarket has implemented trading fees based on the Maker-Taker model, with trading fees computed based on the formula: Fee = Number of Shares Traded × Fee Rate × Price of Shares × (1 - Price of Shares), The fee rate ranges from 0 for geopolitical markets to 0.07 for crypto markets. Using this formula, trading fees are probability-weighted, making trading fees highest at maximum uncertainty, when shares trade closest to $0.50, reflecting a 50% probability on either side of the market.

It should be noted that Makers are not charged fees when trading to encourage provision of liquidity on Polymarket. In fact, Makers are rewarded with direct rebates as high as up to 25%.

Kalshi uses a similar formula to compute their trading fees. Taker fees are calculated using the formula: Fee = 0.07 x Number of Shares Traded x Price of Shares x (1 - Price of Shares), while Maker fees use a lower variable component, using the formula: Fee = 0.0175 x Number of Shares Traded x Price of Shares x (1 - Price of Shares). Since Kalshi accepts deposits via traditional fiat rails, it also levies a 2% processing fee on debit card deposits and withdrawals, though ACH transfers are free.

Thin markets on both exchanges carry hidden costs in the form of bid-ask spreads, which widen significantly on lower-liquidity events. A trader entering and exiting a position on a niche market may pay more in spread than in stated fees.

Compliance and Regulatory Situation

Kalshi's current regulatory standing is the result of years of deliberate groundwork. After receiving the CFTC Designated Contract Market status in 2020, Kalshi was required to implement full KYC/AML procedures, ongoing reporting requirements, and market surveillance systems before beginning its operations in 2021. Despite their license and compliant approach, the legal troubles did not stop there, but each legal victory continued to expand their market and product offerings, with their biggest being the 2024 case against political prediction markets. Since May 2025, the CFTC has dropped its appeal, and Kalshi now operates sports, election, economic, and crypto event contracts under federal oversight. Its reach currently covers most U.S. states, with exceptions in Arizona, Illinois, Massachusetts, Maryland, Michigan, Montana, Nevada, and Ohio, primarily due to ongoing state-level disputes with gaming regulators.

Polymarket's path has been more turbulent. After the 2022 CFTC settlement and mandatory geo-blocking of U.S. users, the platform grew its user base overseas instead, targeting an international crowd. It broke back into the U.S. market via its 2025 acquisition of QCEX, a CFTC-licensed exchange and clearing entity. As of mid-2025, Polymarket received CFTC Designated Contract Market designation for its U.S. entity. The U.S. rollout has been gradual, starting with an invite-only access phase, before rolling out to the general public.

Security: Oracles, Disputes, and Resolution Risks

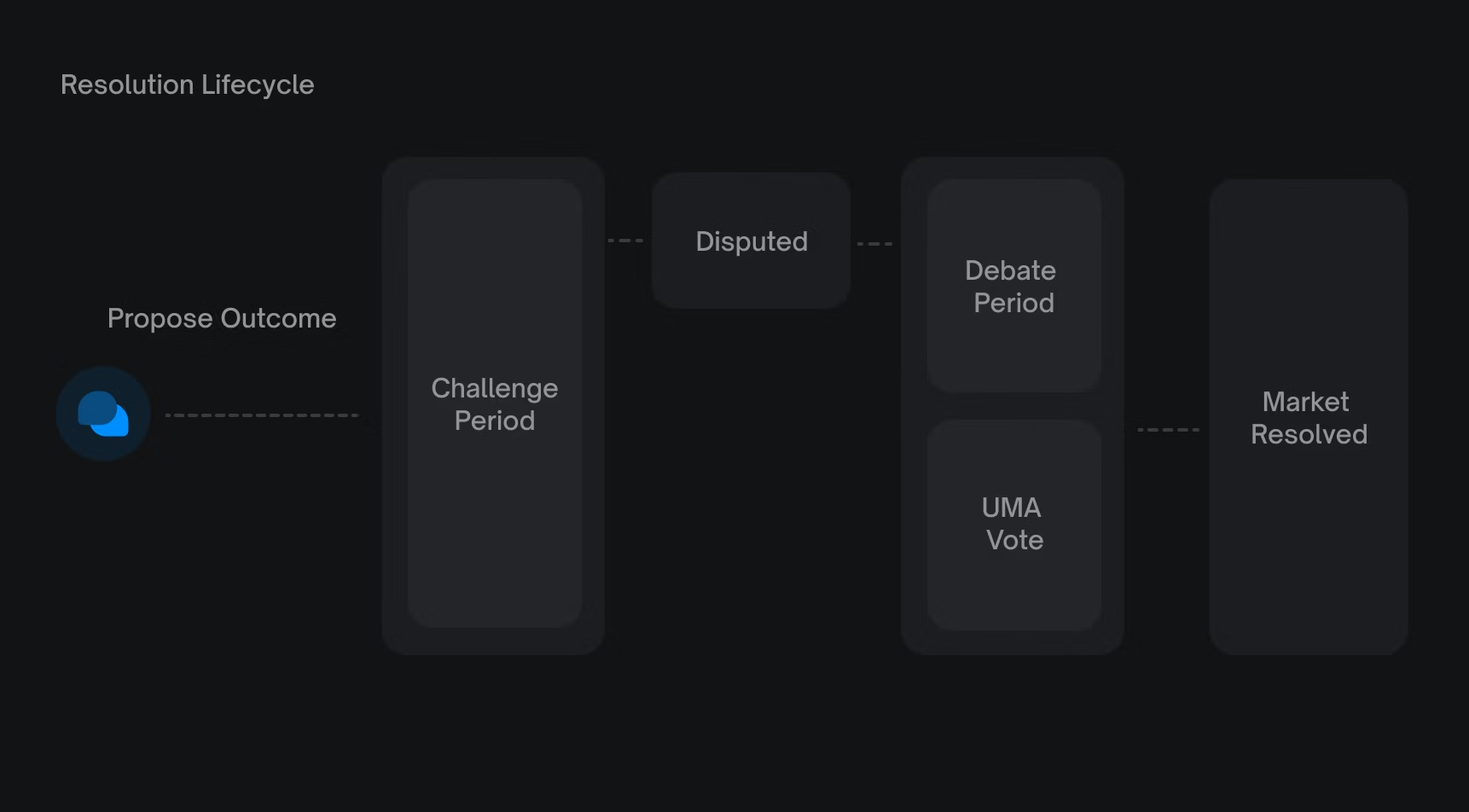

Despite their differences in design, the core of any prediction market lies in resolution: how does a smart contract or application know what actually happened in the physical world? The design of each platform's resolution mechanism defines its security profile.

Polymarket delegates the entire resolution process to UMA's Optimistic Oracle, an independent decentralized protocol where anyone can propose an outcome, anyone can dispute it, and contested cases escalate to a vote among UMA token holders. According to data from UMA, roughly 98% of Polymarket markets resolve without any dispute, settling within two hours of a proposal. The remaining 2% involve a challenge process that can take four to seven days before resolution. During that period, affected funds are locked.

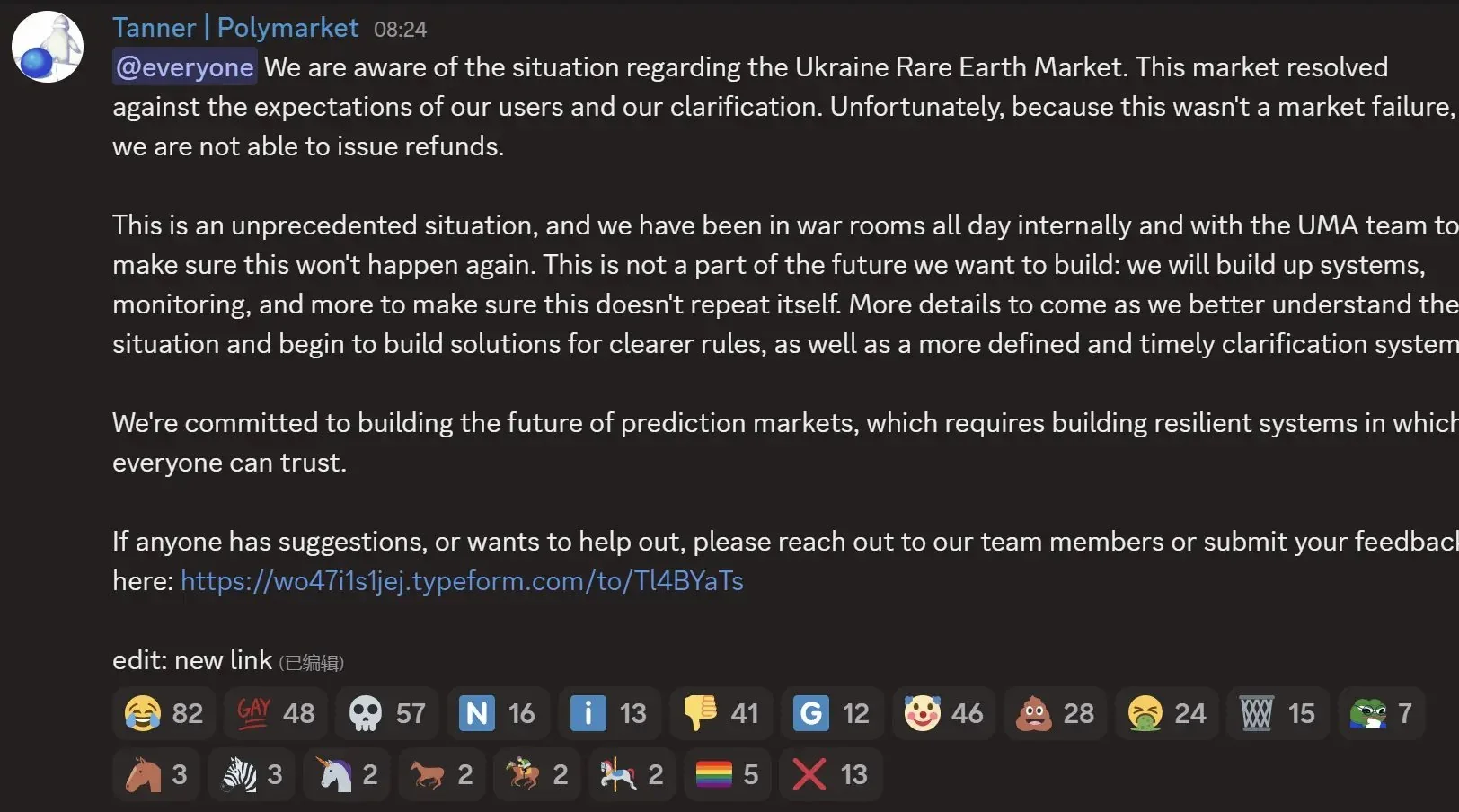

The vulnerability in this resolution mechanism is language, specifically ambiguity in language. Markets whose resolution criteria are ambiguous enough to admit competing interpretations have historically generated the most contentious disputes. In a high-profile case involving a market regarding a rare earth minerals deal between Ukraine and the USA, Polymarket incorrectly resolved the market to “Yes”, despite there being no such deal. This was a result of a single UMA token whale forcing an incorrect resolution. In such a case, personal interests outweighed factual accuracy, casting doubt on the reliability of Polymarket’s resolution process.

Kalshi's resolution mechanism is much more centralized, with a team within the exchange reviewing outcomes against pre-defined market rules and declaring results. This approach is faster and eliminates the governance dynamics that occasionally complicate UMA votes, but it also concentrates decision-making authority in a single organization. In the case of the recent death of Iran’s Supreme Leader, Ali Khamenei, Kalshi froze the market relating to his ousting, claiming that they did not allow transactions “directly tied to death”. $77 million in winnings tied to the market were not paid out as a result, drawing controversy from users.

Market Ecosystem and Offerings

Polymarket's catalog skews toward global and crypto-adjacent topics. Political events, Fed rate decisions, crypto price milestones, entertainment awards, and internet culture events all find audiences here. The platform's architecture - permissionless market creation backed by on-chain settlement - means new markets can appear just hours after a breaking news event, which has made it a go-to reference for fast-moving geopolitical stories. During the 2024 election cycle, mainstream media outlets began citing Polymarket odds as a benchmark alongside polling averages.

Kalshi's catalog reflects its regulated U.S.-centric origins. Congressional control, Federal Reserve decisions, inflation and unemployment prints, weather events, and U.S. sports dominate the Kalshi selection. The focus on U.S. macroeconomic events has attracted notable interest from traders as well as institutions, with partners including Robinhood and Coinbase using Kalshi's infrastructure to offer event contracts to their users.

On speed, Polymarket's permissionless structure gives it an advantage for emerging events. While Kalshi's regulated environment requires internal review before any new market can go live, it can reduce the risk of malformed or unresolvable markets reaching traders.

A Brief History of Polymarket

Polymarket was built on a straightforward premise: financial incentives produce better forecasts than opinion polls. The platform was launched by Shayne Coplan, who had dropped out of NYU's computer science program, in June 2020 to counter misinformation during the COVID-19 pandemic. The early product attracted a small but engaged crypto-native audience, and the 2020 U.S. election served as an early stress test that demonstrated real liquidity could form around political outcomes.

The platform's first significant setback came in January 2022, when the CFTC issued a cease-and-desist order, citing Polymarket's operation as an unregistered swap execution facility. Polymarket settled for $1.4 million, blocked U.S. IP addresses, and shifted its growth strategy offshore, leaning into its decentralized architecture and kept building.

The platform’s breakout moment came in 2024 with the U.S. presidential elections. Trading volume grew from $73 million in 2023 to $14.1 billion across the full year, driven largely by the U.S. presidential election cycle with almost $3.7 billion wagered on the Trump-Harris race alone.

In late 2025, the Intercontinental Exchange, the parent company of the New York Stock Exchange, had made a $2 billion strategic investment, valuing Polymarket at approximately $8 billion. The platform simultaneously acquired QCEX, a CFTC-licensed exchange, to facilitate a regulated re-entry into the U.S. market.

As of 2026, Polymarket has relaunched in the U.S. under a more compliant structure and is reportedly in talks for a Series E funding round at a valuation of $15 billion.

A Brief History of Kalshi

Kalshi took the opposite approach to Polymarket from a regulatory standpoint. Founded in 2018 by MIT graduates Tarek Mansour and Luana Lopes Lara, the company spent more than two years working through the CFTC approval process before launching a single contract. Kalshi received designation as a CFTC Designated Contract Market in 2020, becoming the first U.S. exchange specifically authorized to offer event contracts. The platform opened to traders in July 2021.

Much like Polymarket, Kalshi’s biggest moment arose due to the 2024 U.S. presidential elections, albeit in a different form. After the CFTC moved to block the offering of political event contracts as contrary to the public interest, Kalshi sued. In October 2024, a federal district court in Washington, D.C., sided with Kalshi, ruling that political event trading did not constitute "gaming" under the Commodity Exchange Act. The CFTC initially appealed, then dropped its appeal entirely in May 2025 following a change in administration.

This landmark legal victory for the platform opened the doors for many of its later products. Sports contracts followed in January 2025, and although state gaming regulators and tribal gaming interests have since filed legal challenges, Kalshi continued operating under federal oversight. In its latest raise in May 2026, Kalshi raised $1 billion at a valuation of $22 billion in a Series F round led by Coatue.

Which Is Better for You?

Best for U.S. users: Kalshi. It is fully operational, accepts standard payment methods such as traditional fiat rails, and is federally regulated. For anyone who prefers not to deal with crypto wallets or stablecoins, Kalshi is the straightforward choice.

Best for crypto-native and international users: Polymarket. Its global footprint, non-custodial architecture, and zero-fee-or-low-fee structure across most markets make it the natural home for traders outside the U.S. or those who are already familiar with crypto.

Best for long-term hedgers and macro traders: Kalshi. Its macroeconomic and economic data markets: Fed decisions, CPI, labor data, offer structured exposure to real-world financial outcomes with institutional-grade clearing, make it an attractive choice to professional traders and funds looking to express specific views regarding these events..

Conclusion

Polymarket and Kalshi have both scaled rapidly, but they remain genuinely different products serving different users. Kalshi's compliance-first approach gives it structural advantages in the U.S.: broader payment options, institutional partnerships, and a regulatory track record that took years to build. Polymarket's decentralized architecture makes it faster, more globally accessible, and cheaper to trade on for most market categories.

Neither platform is without risk: Polymarket's oracle-based resolution has produced controversial resolutions of high-profile markets before, while Kalshi's centralized model means a single internal decision can freeze $77 million in user funds. As both platforms push deeper into overlapping territory, the choice between them comes down less to which is objectively better, and more to each user and their needs.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)

{kind=link}