July 3, 2026

at

5:40 am

EST

MIN READ

Tokenized Deposits: What Are They And How Are They Different to Stablecoins?

Institutional adoption of blockchain technology has accelerated steadily over the past few years, moving from cautious experimentation to production infrastructure. Banks and asset managers that once treated digital assets as a peripheral concern are now building on-chain products for core treasury, settlement, and payment functions.

One of the more significant developments to emerge from this shift is tokenized deposits, a way for regulated banks to put existing deposit infrastructure onto distributed ledgers, gaining the speed and programmability of crypto rails without needing to step outside the conventional banking system. As institutions look for ways to modernize legacy banking systems, tokenized deposits have become one of the prime experiments in how blockchain technology might complement, rather than replace, the systems already in place.

Summary

- Tokenized deposits are digital tokens issued by regulated banks representing real deposits, subject to the same insurance, capital rules, and regulatory oversight as traditional accounts.

- Unlike stablecoins, tokenized deposits operate on permissioned networks restricted to identity-verified institutional clients, keeping liabilities on the bank's balance sheet.

- Key use cases include cross-border payments, atomic trade settlement, programmable collateral management, and conditional payment automation for corporate treasuries.

- Major financial institutions like JPMorgan, HSBC, and BNY are already running live programs, but interoperability across banks remains the primary barrier to broader adoption.

What Are Tokenized Deposits?

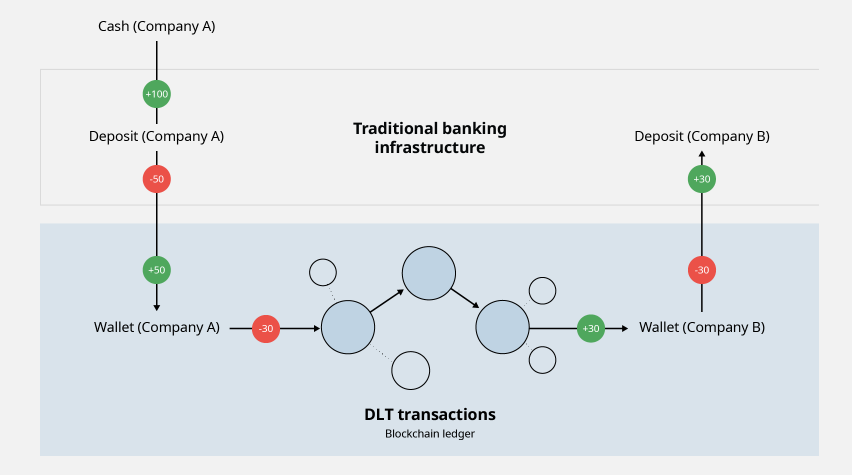

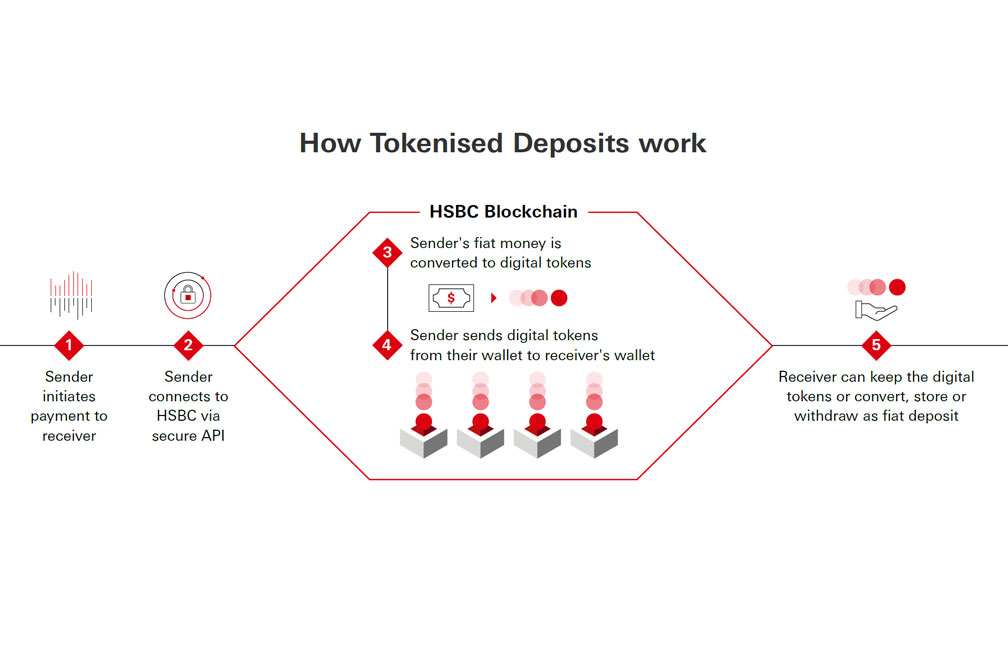

A tokenized deposit, as the name implies, is a tokenized representation of deposits held at a bank or financial institution. This is created when a bank takes one of its existing deposit liabilities and issues a digital token to represent it on a blockchain or distributed ledger. Think of it as the bank printing a receipt for your deposit, except that receipt can move on a shared ledger, settle instantly, and carry programmable instructions.

The deposit itself does not go anywhere. It stays on the bank's balance sheet, earns the same regulatory treatment, and falls under the same deposit insurance framework as any other account. What changes is the delivery mechanism: instead of moving money through conventional payment rails with their cut-off times and correspondent bank delays, the token representing that money can transfer between parties in real time, at any hour, with settlement recorded automatically.

As such, tokenized deposits can be viewed as a wrapper around money that already exists inside the banking system. The bank remains the issuer, the liability remains with the bank, and the holder's claim is on that bank rather than on a pool of reserve assets sitting in a third-party account.

Tokenized Deposit Use Cases

The most immediate use case for tokenized deposits is simply moving money faster. Tokenized deposits can settle between counterparties in real time, cutting through settlement windows for domestic and cross-border transfers. This speed also extends to trade settlement, removing counterparty exposure in the window between the two.

Tokenized deposits can also be pledged as collateral for trades, loans, or margin requirements without transferring funds out of the depositor's account. As the token lives on a shared ledger, collateral can be mobilized and released programmatically, reducing the operational overhead of collateral management desks and freeing up liquidity that would otherwise sit idle.

Above all is the capacity to embed conditional logic into the token itself. A tokenized deposit can be set to transfer only when certain conditions are met. This removes manual steps from processes that currently require human intervention to execute and reconcile.

Consider a multinational corporation running treasury operations across Hong Kong, Singapore, and London. At the end of each business day, the treasury team is trying to sweep excess liquidity from one entity into another, fund upcoming payments in different currencies, and make sure no subsidiary is sitting on idle cash overnight. Under the current system, each of those sweeps goes through correspondent banking rails that close at specific times, take hours or days to settle, and require manual reconciliation on the back end.

With tokenized deposits, the same company can hold its bank balances as digital tokens inside a permissioned system and move them between its own accounts, or to approved counterparties, at any moment. The transfers settle in real time without waiting for banks to open, and conditional rules can be embedded directly into the payment itself, so that a transfer only executes when a predefined threshold is met or a specific invoice is matched.

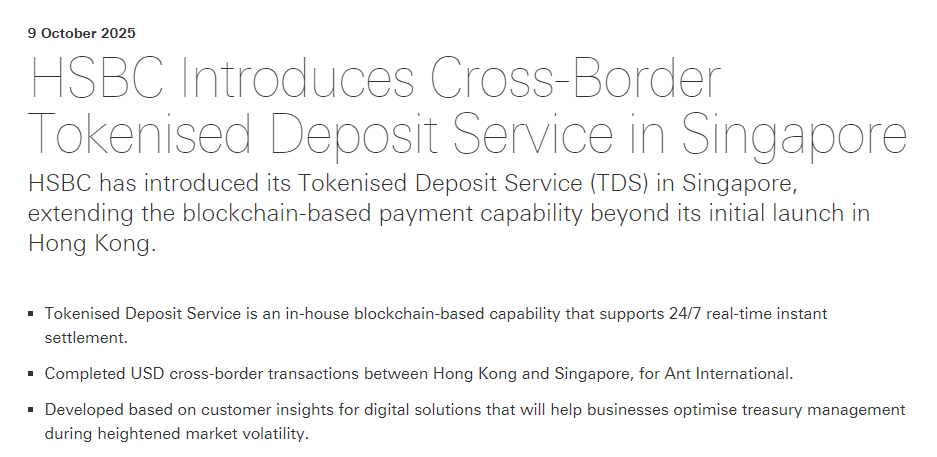

HSBC demonstrated this in September 2025 when it completed its first cross-border tokenized deposit transaction, moving U.S. dollars between Hong Kong and Singapore for Ant International in real time. That transaction removed time-zone friction from an otherwise routine treasury function and allowed the company to manage its liquidity position continuously rather than in batch windows.

Tokenized Deposits vs Stablecoins

The two instruments get conflated regularly, but the structural differences are significant.

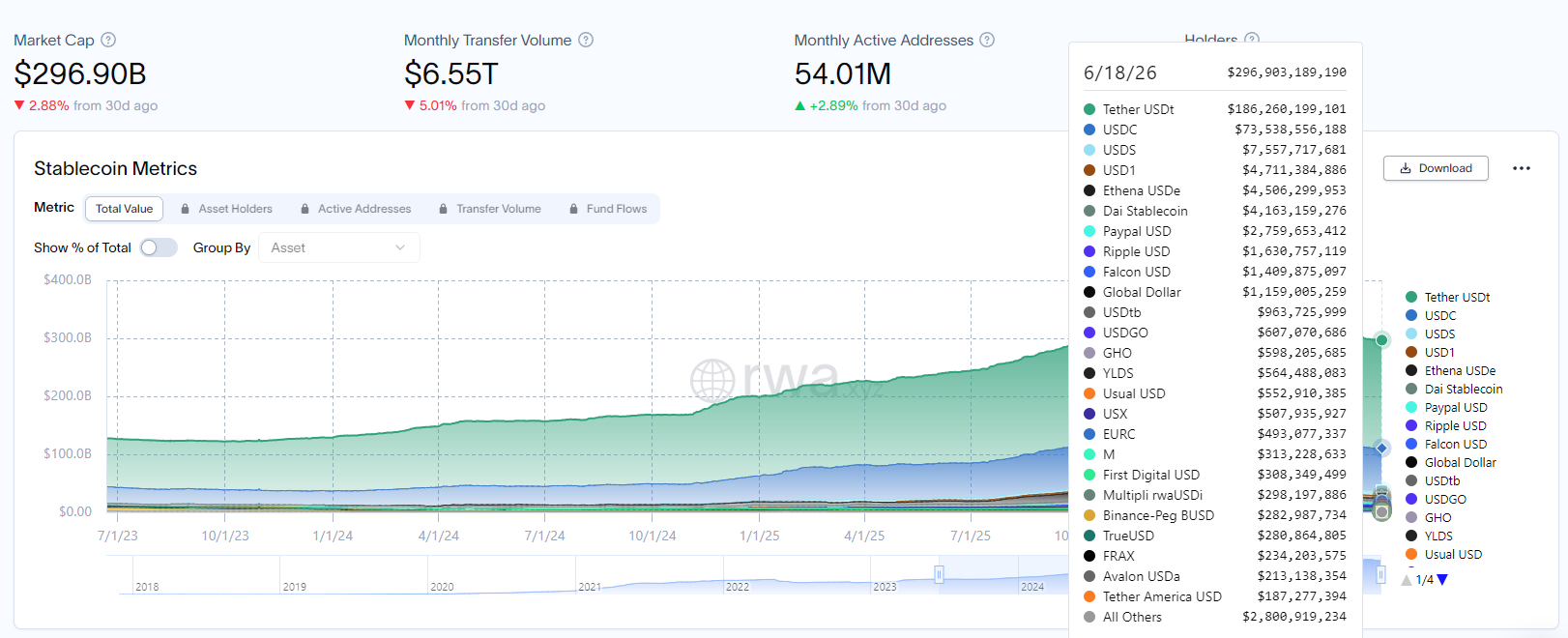

Stablecoins like USDT or USDC are issued by non-bank entities. The issuer holds a pool of reserve assets, typically short-dated U.S. Treasury bills or cash equivalents, and the token circulates as a bearer instrument on public blockchains, with ownership belonging to whoever holds the token at any point in time. There is no bank balance sheet involved, no deposit insurance, and no requirement to go through standard identity verification to receive or send the token. The total outstanding supply of USD-backed stablecoins has climbed to almost $300 billion by mid 2026, and they have become deeply embedded in crypto markets and cross-border payment flows.

Tokenized deposits work differently at almost every level. The liability sits with the issuing bank, not a reserve pool. They operate on permissioned networks where all participants are identity-verified clients of that bank. Transfers are recorded as updates to the issuing bank's ledger rather than transfers of a bearer asset. Since the bank is the issuer, the underlying deposit remains eligible for the same deposit insurance protections (where applicable) and regulatory protections as any other account held at that institution.

A February 2026 New York Fed staff report captured the structural distinction clearly: stablecoins function as a form of "safe money" for payments, while tokenized deposits stay inside the conventional bank money framework and continue to fund lending. One instrument is a parallel system, the other is the existing system running on better infrastructure.

Naturally, the distinction creates a trade-off in accessibility. Stablecoins are available to anyone with a wallet, while tokenized deposits are available only to vetted institutional clients of the issuing bank, which is both the source of their regulatory strength and the primary constraint on their adoption.

Banks Offering Tokenized Deposits

JPMorgan

JPMorgan operates its tokenized deposit program through Kinexys, the firm's blockchain division previously known as Onyx. The platform already processes more than $7 billion in daily transaction volume, with over $3 trillion processed since inception. In November 2025, JPMorgan officially launched its USD-denominated deposit token, branded JPMD, to institutional clients on Coinbase's Base Layer-2 network. The token allows approved clients to move dollars between accounts using public blockchain infrastructure while remaining within JPMorgan's permissioned client ecosystem. The bank and Singapore's DBS have also announced an interoperability framework to connect their respective on-chain systems.

HSBC

HSBC launched its Tokenized Deposit Service in Hong Kong and Singapore in May 2025, initially for domestic payments. By September, it had completed its first cross-border transaction, and by late 2025 it had expanded the service to the UK and Luxembourg, supporting GBP, EUR, USD, HKD, and SGD. In April 2026, HSBC extended the program to U.S. corporate and institutional clients. The service uses HSBC's proprietary distributed ledger technology to convert deposits into digital tokens on a 1:1 basis and currently supports programmable conditional payments and tokenized asset settlement.

BNY Mellon

BNY launched its tokenized deposit service for institutional clients in January 2026. The program provides a blockchain-based record of client deposits held at the bank and is designed to enable faster payments and settlement for institutional counterparties. BNY has also collaborated with Goldman Sachs' Digital Asset Platform on tokenized money market funds, signaling a broader move toward on-chain institutional infrastructure across the bank's product line.

Advantages of Tokenized Deposits

The most immediate advantage is settlement timing. Conventional bank transfers, even fast ones, carry cut-off windows, batch processing delays, and correspondent banking layers that add friction to large-value flows. Tokenized deposits settle on-chain in real time, around the clock, regardless of time zones or banking hours.

Additionally, tokenized deposits offer the benefit of programmability. Banks can embed conditional logic directly into tokenized deposit transfers: payments that execute only when a document is verified, sweeps that trigger automatically at a liquidity threshold, or settlement that occurs atomically when two parties exchange assets simultaneously. These capabilities either do not exist or require significant manual intervention on legacy rails.

Finally, tokenized deposits also benefit from their regulatory standing, particularly for institutions that need their counterparties to hold regulated instruments. Since tokenized deposits stay inside the banking system, they carry FDIC eligibility where applicable, access to central bank liquidity facilities, and a supervisory framework that institutional risk teams already understand.

Risks of Tokenized Deposits

The biggest practical risk at this stage for tokenized deposits is interoperability. Most tokenized deposit programs currently operate within a single bank's ecosystem. Moving value between a tokenized deposit at JPMorgan and one at HSBC is not straightforward, and the multi-bank clearing network that would make this seamless is still in development. The Clearing House announced plans in mid-2026 for a shared tokenized deposit network involving more than a dozen U.S. banks, but that infrastructure does not yet exist at scale.

Technology risk is also a factor. Smart contracts can carry bugs, and distributed ledger infrastructure lacks the decades of testing built into core banking systems. When these new systems fail, they don't break the way traditional payment rails do. Banks running these programs are taking on operational risk that has limited historical precedent.

Finally, access constraints limit network effects. A tokenized deposit is only useful if both the sender and receiver are clients of the issuing bank, or if interoperability infrastructure connects them to counterparties at other institutions. Until multi-bank networks mature, tokenized deposits remain powerful inside a single bank's ecosystem but less useful for payments that cross institutional boundaries.

Conclusion

As institutional adoption of blockchain technology accelerates, tokenized deposits represent a meaningful shift in how institutions use money held in banks. By putting existing deposit infrastructure on distributed ledgers, banks gain the speed and programmability that have made stablecoins attractive, while keeping their regulatory standing and balance sheet treatment intact. For institutions that cannot or will not work with stablecoin issuers, tokenized deposits offer a compliant path to real-time settlement and programmable payments.

The limitations are real: restricted access, nascent interoperability, and unproven technology at scale. But the pace of institutional adoption, from JPMorgan's live JPMD program to HSBC's multi-market rollout to BNY's January 2026 launch, suggests that tokenized deposits are moving from pilot phase to operational reality faster than most of the earlier blockchain-in-banking efforts managed to do.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)

.png)

.png)