June 8, 2026

at

9:35 am

EST

MIN READ

Non-USD Stablecoins Reach $2B Circulating Supply

Non-USD stablecoins have climbed to an all-time high circulating supply of $2 billion, propelled by a $600 million influx since the start of the year. According to recent on-chain data, this growth is heavily dominated by three distinct regional tokens:

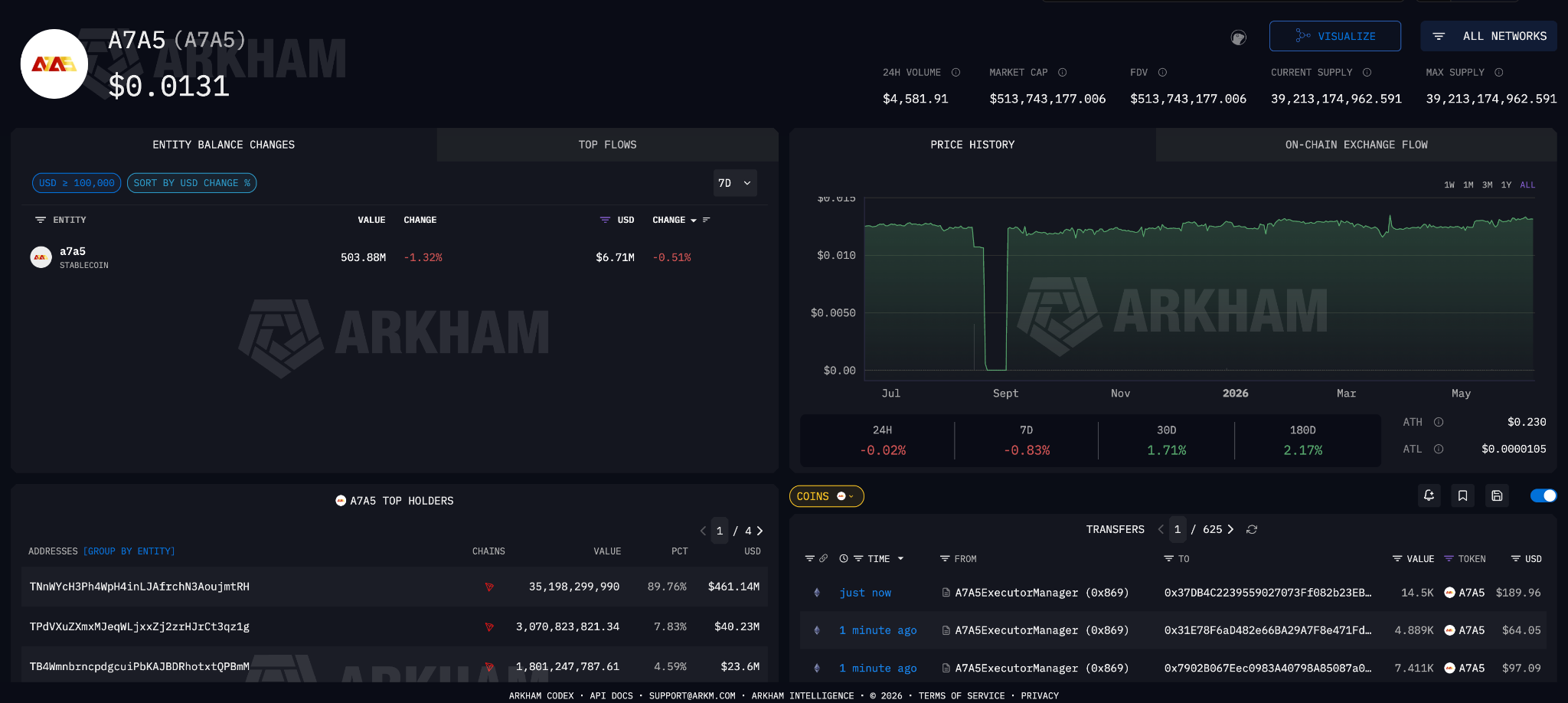

- A7A5 - $586M: Russian-Ruble backed stablecoin

- BRZ - $479M: Brazilian Real backed stablecoin

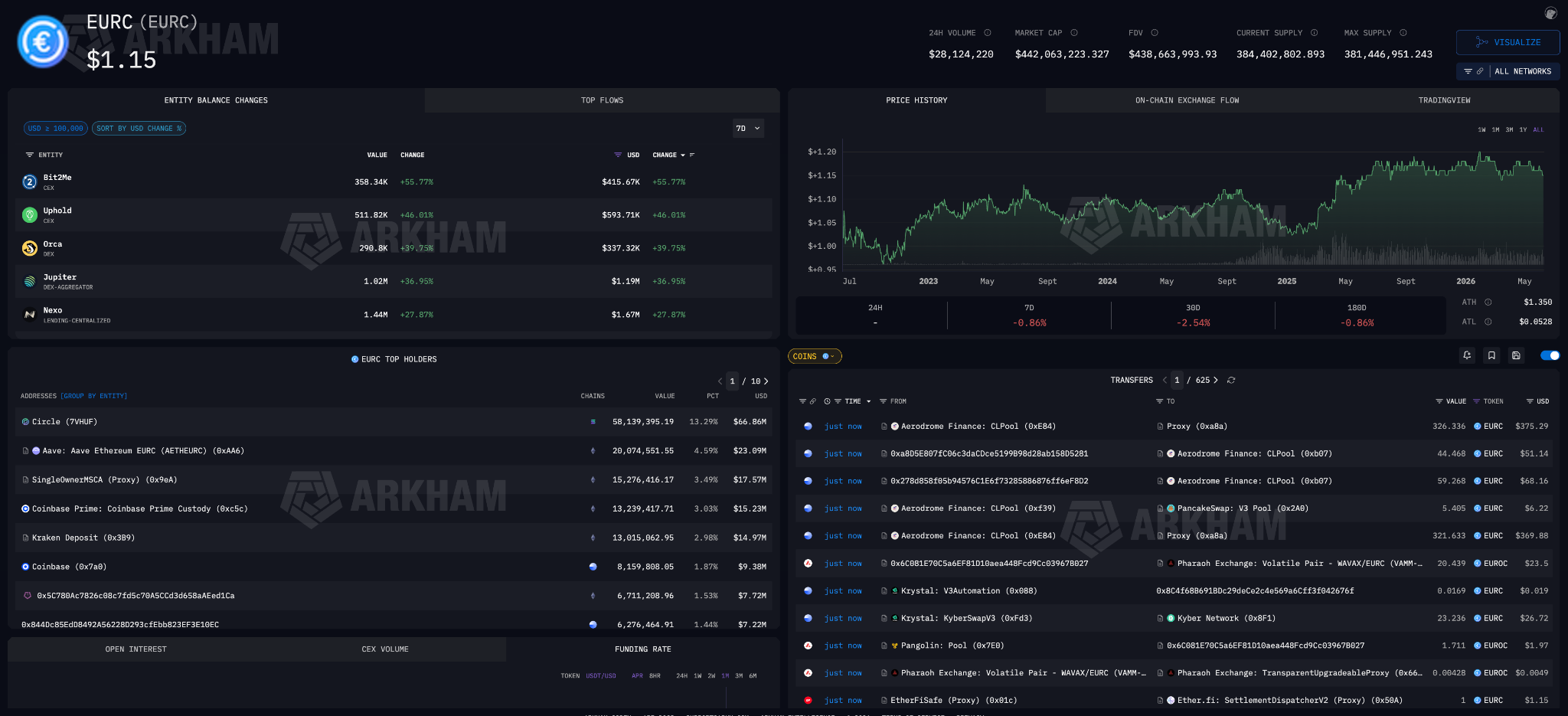

- EURC - $440M: Euro-backed stablecoin

Over the last few years, the USD stablecoin supply has become a bellwether metric people watch to assess the state of crypto. There are good reasons for this - USD stablecoin supply provides an indication of liquidity conditions, DeFi adoption and risk appetite.

But the rest of the world has currencies too.

Currently, non-dollar stablecoins are almost statistically irrelevant. $2 billion set against the roughly $316 billion in USD stablecoins and you have a market that is, for now, almost entirely dollar-denominated.

But the stablecoin market is currently inconsistent with the actual reality of the supply of global currencies. When looking at foreign exchange reserves, the dollar accounts for about 57% of global foreign exchange reserves - dominant, but not the 99% implied by stablecoins.

The Euro holds around 20%, the Yen about 6% and Sterling about 4%, out of a global reserve pool of roughly $13 trillion. This means that more than 40% of the world's reserve fiat sits in currencies with very little stablecoin presence. There is clearly significant room for growth, and the rate of increase of non-USD stablecoins in 2026 suggests that growth may be about to begin.

This growth will have a considerably different look to dollar stablecoin growth. USDC and USDT, the two dominant stablecoins, were private-sector projects that operated in a landscape of minimal regulation. That may be changing.

Governments increasingly see tokenised money as an extension of monetary policy, meaning it requires heavy regulation, if not outright absorption through CBDCs. The European Central Bank frames its digital euro CBDC as a "global euro moment," explicitly aimed at strengthening the euro's international role and protecting European payment sovereignty. China is pursuing the same logic, treating the digital Yuan as part of a deliberately multipolar currency strategy.

As of May 2026, 146 countries representing 98% of global GDP were exploring a CBDC. The US under Donald Trump has explicitly banned CBDCs for the dollar. So, although non-USDC stablecoins are a tiny fraction of the stablecoin supply today, the landscape has already started to shift. This $2 billion milestone could be the start of a rebalancing of the stablecoin supply away from USD.

The three largest non-USD stablecoins listed above offer an interesting cross-section of the growing use-cases of non-USD stablecoins.

A7A5 is a stablecoin that was launched by crypto company A7 in 2024. A7 is largely owned by Russian state-owned bank Promsvyazbank. We wrote a quick guide to A7A5 here. A7A5 is allegedly being used by Russia (and sometimes Iran) to bypass western sanctions.

BRZ is the leading Brazilian Real stablecoin. Each BRZ has a 1:1 peg to the Brazilian Real and is backed by a reserve of fiat Brazilian Reals, government bonds, or other highly liquid collateral managed by its issuing entity, Transfero Group. Brazil has a high crypto adoption rate and BRZ enables users to minimise FX risk during trades. Most of the BRZ supply is on Gnosis, an EVM-compatible chain.

EURC is the leading Euro stablecoin, issued by Circle. EURC is 100% backed by euros held in euro-denominated banking accounts so that it's always redeemable 1:1 for euros. EURC is a growing alternative to USDC, allowing European crypto users to minimise foreign exchange risk (the potential for financial loss due to fluctuations between the value of different currencies), engage in DeFi, conduct cross-border payments and be compliant with MiCA.

Non-USD stablecoin adoption is lagging way behind USD counterparts. However, the rate of increase is significant. Non-USD circulating supply is up 43% this year, whilst USD supply is up just 2%.

There are several reasons why non-USD stablecoins are so far behind USD. These range from stricter regulations (in the EU, MiCA regulations demand a high proportion of stablecoin backing is held in cash), the network effects of the dollar, a lack of liquidity, and poor off-ramping infrastructure. Read our beginner’s guide to stablecoins here to understand the landscape mechanics, and use cases of these pegged cryptocurrencies.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)